The economic projects implemented by the state have not produced significant revenues for anyone but their contractors, as the frantic focus was on infrastructure projects, especially roads and bridges, and establishment of two new capitals: a winter capital and a summer capital. Then, some repercussions of the Russian war on Ukraine started to appear, in addition to the already deteriorating conditions of the Egyptian economy as a result of the policies adopted by the regime over the past years. The paper attempts to answer the question is: How does the Egyptian regime react toward the worsening economic crisis in the country?

Monetary policies

A massive inflation wave hit the Egyptian market following the devaluation of the Egyptian pound in late 2016, which later prompted the Egyptian authorities to maintain stability of the exchange rate, to demonstrate the success of its economic policies, and to control prices at home, in addition to maintaining an appropriate price for investors in local debt instruments, when they leave.

Then, the Coronavirus Pandemic came to further complicate matters, as it caused a severe inflation crisis that affected the whole world as a result of economic recovery attempts and compensation for the losses caused by the crisis. Of course, the global inflation wave reflected on the Egyptian citizen, that had not yet recovered from the first inflation wave following the government’s agreement with the International Monetary Fund (IMF) and the flotation of the local currency.

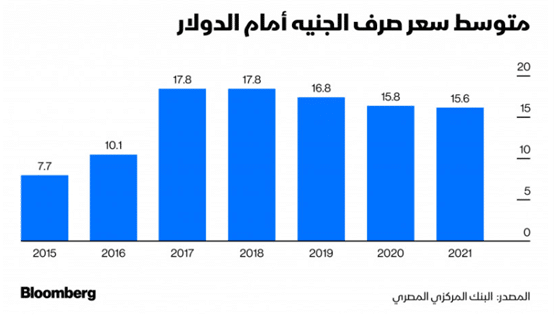

It was logical for the global inflation wave to move to an economy that relies on importing most of its needs from abroad. To counter the effects of external and domestic inflation, the government sought to stabilize the exchange rate (as shown in the following figure), which widened the gap between the real value and market value of the local currency over time.

For example, Goldman Sachs Group indicated – more than two months before the outbreak of the Russian-Ukrainian war – that the Egyptian pound was overvalued by about 15%, which means that the fair value of the dollar price against the Egyptian pound then exceeded EGP 18[1].

Thus, the Egyptian monetary authorities found themselves in front of the dilemma of devaluation of the pound again, which necessarily leads to fueling the already enflamed inflation, in addition to the significant negative impact of this percentage (15%) on the net real interest that hot money investors are likely to obtain.

Therefore, the decision of the Central Bank of Egypt (CBE) to devaluate the Egyptian pound came along with raising the interest rate by 1%, to serve the interest of foreign investors in local debt instruments over the crushed majority of the Egyptian people, in anticipation of a dollarization wave and the black market that had already begun.

In general, the wave of the initial devaluation of the pound and the initial raising of the interest rate have already occurred, with likeliness of not being the last. Senior Analyst for the Macroeconomics and Financial Services Sector at HC Monette Doss expected a gradual decline in the value of the Egyptian pound during 2022. in view of the pressures on the balance of payments in Egypt, due to the repayment schedule of Egypt’s external debts. It should be noted here that this prediction was before the outbreak of the Ukrainian war.

The vice president of Research at Zilla Capital also noted that the medium and long-term fundamentals of the Egyptian pound remain unfavorable, in addition to the increasing reliance on capital inflows; and the balance of payments continues to suffer from a low level of foreign direct investment, and modest growth in non-oil exports.

The logical question here is: Is it possible for these factors affecting the value of the pound to change in the short or medium terms? The clear answer is that there will be no significant change in the level of foreign investment flows, the current balance deficit, or any significant changes to factors affecting foreign exchange flows (except for debt and Gulf deposits). The only thing that may reappear with successive rate hikes is hot money, but it is unlikely to return to its high value quickly, especially in light of competition by emerging economies, and also in light of the successive hikes in the US interest rate.

1- (Financial) austerity policies

The expected increase in the public budget deficit resulting from the global rise in prices of goods imported by Egypt is likely to be met by the government with a large wave of austerity, which may be manifested in postponenent of some investment expenditures in allocations of some bodies, but it is certain that it will not touch thousands of soldiers deployed in the state’s bureaucratic apparatus, neither will it affect the wages of senior state employees.

Most of the revised fiscal policy is likely to focus on the revenue side, through raising fuel prices and gradually removing the remaining subsidies, raising the prices of food commodities, and raising the price of subsidized bread, in addition to increasing government service fees. It is also certain that we will witness a new wave of increasing indirect taxes on value or others, as well as raising customs duties, with the likely slowdown of the state’s tendency to support the price of gas and electricity for factories, to a large extent.

Reducing public expenditures will always remain the government’s last resort as it seeks to reduce the budget deficit. Whatever the government’s measures towards revenues, it will not lead to the desired results, given that the informal economy controls 55 percent of the Egyptian economy.

2- External borrowing

The departure of $15 billion from domestic debt instruments means erosion of a significant proportion of foreign exchange reserves. Also, the repayment of dues on Egypt, including installments and foreign loan interests in the current year, amounting to $ 14.9 billion, means that the foreign exchange reserves will evaporate in one year, with only about $ 10 billion remaining to finance exports, enough for only four months at most. This means that the Egyptian government is on its way to a new and big wave of external borrowing.

The Egyptian regime has lately maintained its foreign exchange reserves in the range of $40 billion, to ensure its control over the exchange rate. In light of the erosion of a significant proportion of these reserves, it is logical to talk about an unusual increase in external borrowing, which may depend to a large extent on finding sources willing to lend.

The Egyptian government has recently announced that it is negotiating with the International Monetary Fund on obtaining a new loan, where Egypt has resorted to the IMF 3 times in the past few years, as follows:

– Egypt borrowed $ 12 billion under the extended fund facility (3 years) agreement in November 2016.

– Egypt borrowed $2.8 billion under the rapid financing instrument (RFI) agreement in May 2020.

– Egypt borrowed $ 5.2 billion under a Stand-by Arrangement (SBA) in June 2020.

That is, the total amount of Egypt’s loans obtained from the IMF amounted to $ 20 billion during the past few years, which puts Egypt in second position after Argentina in the volume of borrowing from the International Monetary Fund.

It seems that the delay in negotiations with the IMF so far is not due to the new austerity terms that the Egyptian administration clearly does not care much about, but because the IMF expressed its frustration with the decline in private investment, and the failure of the Egyptian government to respond to the fund’s demands to amend the competition law, in addition to the most significant condition for the IMF, that is stopping any support for the Egyptian pound in the market[2]. This supports the views about the gradual devaluation of the local currency (more than once) during the coming period, especially after obtaining the IMF loan; and that the speedy raising of the interest rate and the sudden devaluation of the Egyptian pound came to allow for more successful discussions with the IMF.

It is noteworthy that the flexibility of the exchange rate demanded by the IMF will expose the falseness of the Egyptian regime allegations about progress of the Egyptian economy, and that competition will gradually remove the army’s dominance over Egyptian economy and accordingly its support to Sisi, where the regime is likely to accept the former to some extent, but to circumvent the second by the significant expansion of sovereign agencies’ ownership of projects, then sale of a percentage not equal to the previous expansion, which means an increase in ownership and dominance.

Of course, borrowing will not stop at the IMF, but will extend to every possible or potential market for external borrowing in euro bonds, dollar bonds, samurai bonds, or any possible foreign currency. Rather, the importance of the IMF loan lies mainly in the fact that it is a kind of certificate that allows others to have some confidence in continuing the lending process. This also extends to new Gulf deposits, similar to what has recently been announced about a new deposit of $ 5 billionin the Central Bank of Egypt from Saudi Arabia, with talk about a new Kuwaiti deposit, as well as extending the term of some of the already existing deposits.

A report by the Hermes[3] investment bank indicates that Egypt is also preparing to benefit from 2 to 4 billion dollars from net inflows with its inclusion in the JP Morgan Global Emerging Market index, a step that is likely to be accelerated sharply in the coming short period.

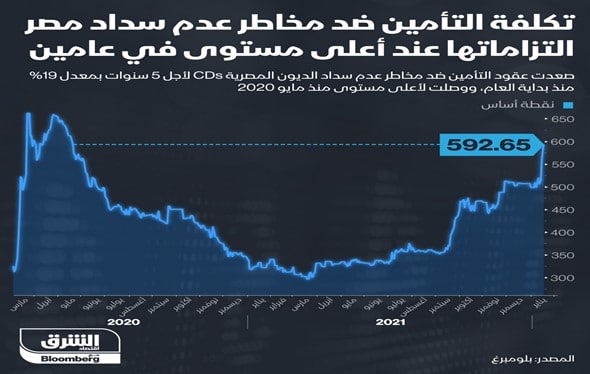

In the context of resorting to external borrowing, it is noteworthy that not only the authority was forced to pay the highest interest rates in the world to be able to borrow due to many negative conditions surrounding the Egyptian economy, but it is also held responsible for the high cost of insuring Egypt’s sovereign debt, which according to the figure below amounted to 19% since early this year, and reached its highest level since May 2020, amid a decline in net foreign assets in Egyptian banks, and high returns on sovereign bonds due in 2029 and 2032.

Of course, the significance of insurance payments on external loans is increasing in light of the sharp growth of such loans since 2013. It suffices to know that in 2013 the external debt was $ 47 billion, against about $ 137.4 billion in late September 2021, where the increase is three times its value in just 8 years.

It is also noteworthy that bilateral loans will play a major role in the coming period, and China will most likely emerge as a lever for the Egyptian economy and regime. However, everyone knows the size of China’s requirements and mortgages for borrowing, taking into mind that the Egyptian mortgaged assets may be subject to confiscation from China in the event of a halt in repayment, as happened in many African countries.

3- Sale of state-owned assets

The Egyptian government has repeatedly announced its program for government offerings and the companies to be privatized, which has been postponed more than once since 2018 under the pretext of the declining stock prices, and waiting for them to rise again, but under the current circumstances, the matter has become urgent to face challenges.

Bloomberg has recently announced that the Abu Dhabi Sovereign Fund, represented by the Abu Dhabi Holding Company ADQ, held talks with Egypt to buy Egyptian state-owned stakes in some of the most successful public companies, most notably 18% stake in the Commercial International Bank, and the “Fawry” banking services company and stakes owned by the Egyptian government in Abu Qir Fertilizers and Chemical Industries, Mist Fertilizer Production Company and Alexandria Container and Cargo Handling Company, with a total of $2 billion.

Announcement of these government sales to the UAE reveals several things, including, as usual, selling the most profitable companies such as the Commercial International Bank, and also highly profitable strategic companies such as fertilizer companies, in light of lack of transparency in evaluation of such companies.

However, what is new in this regard, is likely emergence of an option titled “Choose What To Buy”, where the stakes in companies announced to be sold to the UAE were in no way offered for sale in the government’s offering program, which shows the extent of the predicament in which the Egyptian authority has been involved.

It has also been announced recently, within the framework of the Egyptian-Qatari rapprochement, that Qatar would invest $5 billion in Egypt, likely to be in the purchase of assets similar to the agreement with the UAE.

This was followed by announcing that the Sovereign Fund of Egypt signed an agreement with the Saudi Public Investment Fund, regarding the Saudi Sovereign Fund’s investment of up to $10 billion in Egypt in cooperation between the two funds in various sectors, including: education, health care, agriculture and financial sectors.

The acceleration of wasting the state’s strategic assets at the lowest prices is the title of the coming stage of privatization in Egypt, with continuing implementation of the existing projects, and maintaining the economic and political benefits of stakeholders.

However, these funds will unfortunately evaporate in the same way as the hills of previous external loans[4].

[1] The Egyptian pound in 2022.. A global institution is strongly optimistic, link

[2] Egypt is negotiating with the IMF for obtaining a new loan, link

[3] Expectations of the US dollar price against the Egyptian pound during 2022, link

[4] The views expressed in this article are entirely those of the author’s and do not necessarily reflect the views of the Egyptian Institute for Studies

To Read Text in PDF Format Click here.