Egyptian Military & Destruction of Economy – 4

(In Part 3 of this documentary file, the writer addressed: the suffering of agriculture in Egypt, the public debt, the future of Egyptian economy, the economic legislative structure of the military and legalization of corruption, and the situation of tourism in the aftermath of the 2013 coup d’etat)

XVI- Foreign Funding and Egypt’s Losing Bets for Achieving Development

There are many evidences on the decline in the Egyptian development situation during the past four years. According to a statement of Egyptian Planning Minister Ashraf El-Arabi, the average growth rate in the Egyptian Gross Domestic Product (GDP) during the past four years amounted to 2% while the average population growth rate reached 2.5%.

In a sound development situation, it is supposed to have a growth rate three times the rate of the population increase. But when the rate of the population increase exceeds the growth rate, this is what we call “an inverted equation”, which reflects the dilemma of development in Egypt.

This does not mean that the development in Egypt before the January 25th Revolution was so good. In the light of the aforementioned relation between the GDP growth rate and the population increase rate, we find out that the GDP growth rate was then three times the population growth rate. But, to complete the picture, there was lack of justice in the GDP distribution, resulting in poor distribution of wealth on the one hand. On the other hand, this dedicated the marginalization of large segments of the Egyptian society, in addition to the accumulation of the numbers of the unemployed as well as the poor people.

This led to the deformation of the development results before the January 25th Revolution. In spite of achieving high rates of economic growth, this growth concentrated on rentier and non-productive sectors, which cost it the ability to create jobs suitable for those who want to get a job, especially the new entrants to the labour market of young people.

It is noted that the development policy in Egypt for decades sees that the funding crisis in Egypt can be solved through relying on the outside through foreign investment or debt.

This policy has remained in Egypt up till now; something that was clearly visible during the recreation of the “Future of Egypt” conference, which was held in March,2015. “The Economist” published, a few months ago, that Egypt needs an amount of $ 60 billion until 2018 to achieve a growth rate of 5%. This means that Egypt needs funding flows from abroad at an average of about $ 20 billion per year which is undoubtedly a big challenge for Egypt under the current circumstances.

The ambition of the Egyptian government does not stop at providing the funding, necessary for development through direct foreign investment, but it also tends to borrow money from abroad, under the pretext that the Egyptian external debt is still at acceptable rates and that the interest rate of borrowing from abroad is less than that of borrowing from the inside. The government of Sherif Ismail has been exerting great efforts for borrowing from abroad; it has recently signed loan agreements amounting to $ 4.5 billion with the World Bank and the African Development Bank.

According to the Egyptian government tendencies towards development funding that we mentioned before, there is a group of risks associated with this trend. We can refer to some of them as follows:

The wide-range options of foreign investors:

Egypt does not guarantee that the foreign investor will have one single option in front of him, which is to invest in Egypt. However, Egypt occupies a leading competitive position among the countries of the region and the world, with regard to investments. The current circumstances in the countries of the region, including Egypt, make them repulsive to investments due to absence of political and security stability.

Therefore, the foreign investor will be having the option to choose other countries that enjoy better privileges regarding investment. However, the African countries have significantly become a destination for foreign investments, especially from the emerging countries such as China and Turkey, over the past few years. This was behind Egypt’s loss of the advantage of being member in regional agreements from which the investor benefits in getting tax and customs exemptions, as these African countries have become an open market for investment, as well as goods.

Different Trends:

Unfortunately, with regard to the issue of the government’s reliance on the outside world in the financing of development, yet the goals of the foreign investor differ from those of the host country. The foreign investor’s eye is usually focused on the profit in the first place, which makes him not interested in investing in projects, which are either needed by the development in Egypt or representing quality and time priorities. The foreign investor may be heading for rentier or quick-profit projects, as happened with the Gulf investments in Egypt over the past few years, which concentrated on the areas of real estate and tourism projects, as well as telecommunications and banking services.

While there is strong need in Egypt nowadays for intensive-labour projects to absorb the unemployment surplus, as well as the pumping of foreign funds in the field of investment in the industry and agriculture sectors, especially those that depend on the achievement of high added value and targeting a policy of import substitution of goods and services, so as to bridge the gap of resources in this regard, estimated at about $ 20 billion annually.

Looking at the experiences of Egypt’s participation in various international and regional conferences, we find that Egypt usually offers a long list of project ideas without organizing its priority needs.

Thinking about recruitment of external funding for development through direct foreign investment causes the aforementioned risks. Furthermore, the development experiences in several successful models such as the Southeast Asian countries indicate that their success was achieved through the domestic savings, which is unfortunately neglected by the Egyptian planner.

With regard to the experiences of the Southeast Asian countries, the foreign investments came to help after the domestic savings succeeded in financing the development investments. Afterwards, the foreign investments came to reap the fruits of success stories and get sustainable and high-profit investment returns, compared to those of their original countries.

Involvement in external debt:

If the Egyptian external debt is still in the safe limits as some officials say, yet the supplementing part of the equation is that the domestic debt exceeded all the red lines and became one of the challenges that plague the economic and development policy maker in Egypt.

However, it is clear that the tendency for external funding in the Egyptian case was to bridge the financing gap in the budget deficit funding, or to maintain safe levels of foreign exchange reserves.

The credit situation of Egypt necessitates imposition of high interest rates according to the rules of the international credit market. What raises a lot of concerns is that the funding available in the market is usually in favour of short-term and medium-term loans at best, while the financing of development requires long-term funding, which is not available except through the international financial institutions or bilateral agreements between the countries.

Whatever direction the funding came from, whether external or domestic, this money is not grants or donations, but it has its cost which will finally affect the performance of the general budget and the national economy.

The abandoned alternative:

Egypt is still considering a development funding framework that is far from benefitting from the domestic financing. Before thinking about funding, we have to reconsider the priorities for development and then encourage the domestic funding, particularly the “non-formal” one, which is estimated at about LE one trillion. This means that this domestic financing reaches a proportion close to 85% of the volume of deposits available at the Egyptian banking system.

These funds will not be stirred unless they are given the same generous advantages of the foreign investment offers presented by the Egypt government. Moreover, Egypt failed during the past period in marketing its development projects, particularly in the infrastructure areas, through the BOT or the Islamic bonds mechanisms. It is worth noting that the Asian countries and Turkey benefitted so much from these two mechanisms.

XVII- Causes of the Egyptian Pound Collapse after the Coup

There is no need to say that there is no scientific approach to analyse any economic problem we suffer from in Egypt. Though there are many ailments and problems, specialists can diagnose these ailments and develop appropriate treatment for them in order to get out of the crisis of the Egyptian Economy. However, it is obvious that these problems are deliberately left to exacerbate, even go sour and become more difficult to solve, the spread of the disease across the entire economic body and doctors become unable to prescribe any medication due to its side effects on the economy.

An evidence for this is the deterioration of the value of the Egyptian pound over 70 years. The Egyptian pound exchange rate was LE 0.25 against the US dollar before the 1952 Revolution and the beginning of the military rule of Egypt. Now, it has become nearly LE 8.00 in the official exchange market. Since the military coup against the first democratic experience in Egypt and over two and a half years, the value of the Egyptian pound continued to deteriorate due to aggravation of crisis after crisis.

The year “2015” witnessed a decline in the value of the Egyptian pound by more than 30% during the period of the coup, which negatively affected the purchasing power of the Egyptians and led to increasing inflationary pressures, including raising the prices of foodstuff and all costs of living as well as causing the escape of investors.

The pound has fallen in the official exchange market by 11% since the beginning of 2015. The dollar exchange rate has recently reached about LE 8.60 in the black market versus LE 7.10 early last year. Among the causes of this decline in the pound exchange rate are internal causes related to the government’s inability to fulfil any of its promises. Some of them are linked to the monetary policy of the Central Bank and the continuation of the state budget deficit to unprecedented levels, mainly due to the rising expenses and the falling revenues.

The second cause which led to further deterioration of the pound was the result of the inability of government oil companies to repay their debts to the foreign oil exploration companies. The Egyptian General Petroleum Corporation (EGPC) has sought to meet the debt due for the foreign companies operating in Egypt through borrowing from the Egyptian banks and pay arrears to these foreign companies. A group of banks have lent the EGPC $ 3 billion in December, 2014, and recently in April, last year.

The third factor has been associated with more consumer imports of luxury and entertainment items, which can be least described as “provocative”. Figures of the merchandise imports of 2014 revealed that Egypt imported raw sugar for $ 2.6 billion, apples for $ 400 million, corn for $ 1.7 billion, food to cats and dogs for $ 153 million, toys for $ 55 million, jumbo shrimps and caviar for $ 78 million,“Yamish Ramadan” for $ 104 million (Yamish Ramadan: is usually a collection of dates, ‘Qamardeen’ or cooked apricot, reserved figs, apricot, raisin and nuts which Egyptians are used to buying and consuming large quantities of them at ‘sunset’ breakfast in Ramadan, the fasting month for Muslims), meat of peacock, deer and ostrich equivalent of about $ 95 million, chocolate for $ 57 million, race cars, golf cars and ‘Beach Buggy’ for $ 600 million, in addition to import of fireworks and the like for about $ 600 million.

The fourth cause is associated with more payment of the Egyptian debt instalments. It is worth mentioning that this item is expected to increase due to the growing volume of the foreign debt, reaching $ 46.2 billion.

The fifth factor is represented in the manipulation of both importers and exporters of import documents in order to smuggle dollars out of the country, and open offshore dollar accounts due to fear from the coup authorities’ tendency to confiscate their dollar funds as they did with the money, societies, and schools of the Muslim Brotherhood, and charging Businessman Hassan Malek of causing the dollar rate rise. They also smuggle dollars abroad to finance their imports from their dollar accounts abroad in case of the Egyptian banks inability to provide dollar (for import), as well as achieving capital gains through acquisition of dollar and speculating them on the black market.

The sixth cause is related to the flourishing currency trade outside the banking system. There is a big difference between the official price and the price of the black market, which tempts everyone for demand on dollars, so that they could achieve extremely fast gains, reaching at least LE 0.70 per dollar. This makes citizens prefer resorting to the black market, to exchange their revenues in dollars, to resorting to banks. There was a more dangerous element, associated with this factor, i.e. the collusion of both the importers and the money exchange companies to obtain the remittances of the Egyptians working abroad, particularly those who work in the Gulf countries, as a result of the price difference between banks and money exchange companies or what is called the parallel market. So, the military coup played an important role in provoking fear among all economic entities, which led to panic from a control over foreign exchange, prompting them to hedge, caution and keep their wealth out of the country.

The seventh factor is linked to the drug trade. Statistics indicate that the increased spending on drugs is calling for shock. In 1991/1992, Egypt spent about LE 2 billion on drugs. This number jumped to reach LE 40 billion in 1996, due to seizure of a large amount of drugs in that year. According to a series of data on the expenditure on purchase of drugs in the drug trafficking market, the volume of spending on drug purchase could be estimated at LE 60 billion, according to balanced estimates of specialists.

The demand on drugs is mostly made in the US dollar; hence the demand for the dollar to cover the demand for drugs is no less than $ 8 billion annually, which inevitably leads to an increase in the dollar price and a decline in the price of the pound. Are the Egyptian security forces not able to eliminate the trafficking of drugs? or Is it left on purpose to drown the Egyptian people in endless problems? However, the Egyptian security after the coup only concentrated on the political security at the expense of other aspects, especially with regard to the criminal offenses. Furthermore, the police might resort to criminals to eliminate the opponents of the coup.

As a result of all these factors, the coup government failed to control the dollar crisis and rein the big traders, speculating in the dollar, and put an end to the black market. Instead, it headed to foreign parties, whether in agreement with Saudi Arabia to provide oil or in arranging for a loan request from the International Monetary Fund to find solutions for controlling the exchange market.

It seems that there is no solutions for the crisis due to the current policies, which leads to fear from the future and the policies of the brutal military coup, which aims at imposing a control over all the economic resources without studying or planning. Perhaps, the collapse of the pound will be a useful lesson in order to rescue the remnants of the Egyptian economy.

XVIII- Crises of Living Besiege Egyptians after the Coup

With this famous statement, “Tomorrow, you’ll see Egypt”, Sisi, the commander of the military coup, launched his promises of stability and achievement of economic welfare to the Egyptian people. The Egyptians thought their homeland would witness the end of the era of living crises, especially after the Army ousted the elected President Mohamed Morsi on July 3rd. , 2013.

However, what happened was completely the opposite, when many living crises exacerbated, varying between lack of services, low wages, increased unemployment and price rises in most goods and services, after the government tended to reduce the fuel and commodity subsidies in order to reduce the aggravating budget deficit, as well as many other problems. Here, we will review the most prominent living crises suffered by the Egyptians under the rule of the military coup:

1) Fuel prices go on fire:

We overlook fuel crises from time to time, as the current coup regime raised the fuel prices more than once and most recently an increase up to 78%. Domestic gas prices were raised more than once, after the government reduced the fuel subsidies over the last few years from LE 134 billion (LE 7.83 per one dollar) in the budget two years ago to LE 100.3 billion in the last fiscal year budget, and then to LE 60 billion in this fiscal year. It is expected that there will be another increase in the fuel prices within the coming few weeks according to government statements.

It is noteworthy that the fuel crisis was one of the main reasons that led to the June 30 demonstrations against President Morsi. However, after the military coup, the crisis was repeated at frequent intervals, which led successive governments in the era of the coup to resort to the Gulf Cooperation Council (GCC) for oil materials support. In spite of this, the crises exacerbated and its effects extended to the factories, particularly the steel and cement plants where the production capacity was interrupted by 75% due to lack of fuel, according to statistics of the Federation of Industrial Chambers.

2) The electricity crisis:

The Egyptians also faced the crisis of frequent power outages after the coup in spite of the generous petroleum aid from the Gulf States to Sisi’s regime. The power supply outages were repeated in winter as well as in summer, especially during the first period of the coup, before electricity services improved slightly during the last period. However, the electricity bills jumped extremely high after successive increases of electricity prices. Ministry of Electricity reports revealed that there are several reasons behind this problem, including the shortage of gas and the worn out power plants, which prompted the government to resort to diesel to operate them, affecting negatively the capacity of the stations. Moreover, the Egyptian Electricity Ministry suffers from high indebtedness owed by the Ministry of Petroleum, amounting to about LE 60 billion, according to official statistics.

3) The low wages:

One of the prominent problems that faced the Egyptians was the low wages, as the first government after the coup fell on the implementation of its promises of minimum wage application. Kamal Abu-Eita, the Manpower Minister, who came from the heart of the June 30 protests, promised to lift wages and apply the minimum wage within a month, according to media statements he made in August, 2013. A month passed after the other when the workers discovered that these promises were mirage. The Beblawi government confirmed the application of the minimum wage in January, but these assurances were declined in light of the economic downturn, which stood in the way of raising the wages. The first government after the coup failed, and then came the first and the second governments of Ibrahim Mehleb without application of the minimum wage.

Though the budget included an increase in the item “wages” during the last financial year and this year, yet the wages remained as they were. Moreover, the government threatened to cut the salaries of some categories after the announcement of the Civil Service Law, which was exposed to large labour protests during the last period. The strikes of Labour and professional unions continued, demanding better living conditions and higher wages to cope with the growing burdens of life and the increases in prices during the past two years in light of the deterioration of the living conditions despite the increased security crackdown.

4) Aggravation of unemployment:

The problem of unemployment aggravated in Egypt with the continuation of security unrest and instability of situations, which led to deterioration of many sectors, including the tourism sector which used to absorb a number of 4 million workers before the dramatic deterioration of situations after downing of the Russian aircraft over Sinai by a terrorist act, in addition to closure of thousands of factories.

The unemployment rate amounts to about 13% of the total labor force, around 26 million people, according to official statistics. (i.e. equivalent of 3 million citizens) However, some study centers estimate the unemployment rate at more than 25%.

5) Specter of price rises:

The Egyptians were stung over the past two years by the prices of goods and services. The inflation rate in consumer prices ranged between 11% and 13% according to the data of the Central Agency for Public Mobilization and Statistics.

The higher prices of various goods and service extended to the real estate sector, the fees of means of transportation and others. Expectations indicate that the price rise will continue, in light of the austerity measures taken by the current government due to exacerbation of the financial crisis.

6) The bread queues:

The suffering trip of the Egyptians continued with the subsidized loaf of bread, despite the new system, announced by the government, which pledged to put an end to the bread queues completely. However, the crisis did not stop, but became more complex with the new system, which allocated 5 loaves of bread per person daily through a smart card, reducing the loaf weight by 35% from 130 grams to 90 grams. It is worth noting that Dr. Bassem Oudah, the Minister of Supply, who is currently facing a death sentence, was the first one who applied the bread system of separating production from distribution in 2013, in the era of President Morsi, without reducing the weight of the loaf or determining maximum individual limit. During Oudah’s rein, the crisis saw a breakthrough initially in some provinces.

7- Erosion of the Egyptian pound:

The local currency was exposed to great pressures as a result of decline in Egypt’s foreign exchange resources, chiefly of tourism, Suez Canal, remittances of Egyptians working abroad and foreign investments, lower than their levels before the January 25 Revolution, in addition to the accumulated rise of imports against exports.

According to international reports, some projects adopted by the government, such as the Suez Canal shunt, contributed in the increased demand on the hard currency. The dollar rate increased during last year from LE 7.15 to LE 7.83 officially and more than LE 8.60 in the black market, which had its negative impact on the Egyptian citizen. Prices have risen in light of Egypt’s reliance on import of most of the goods, estimated at $ 70 billion annually, according to data of the Central Agency for Public Mobilization and Statistics. Egypt’s reserves of hard currency decreased from $ 36 billion before the January 25 Revolution to about $ 16.4 billion currently, despite Egypt’s obtaining of aid and grants from the Gulf countries, estimated at more than $ 40 billion during the period that followed the coup in 2013.

XIX- Food Gap in Egypt Intensifying

Egypt is considered a net importer of food. It suffers from a food gap in most food commodities, particularly the strategic ones, which led to a high rate of economic dependency on abroad.

The Size of the Food Gap in Egypt:

1) Size of the gap in wheat:

Egypt suffers from a food gap in wheat, where consumption rates are growing larger than production rates. The food production amounted to 8370 thousand tons in 2011, 8795 thousand tons in 2012, 9460 thousand tons in 2013, whereas consumption amounted to about 18015 thousand tons in 2011, 15184 thousand tons in 2012 and 12737 thousand tons in 2013. This resulted in a gap in wheat by 53.5% in 2011, 42.1% in 2012 and 25.7% in 2013. It is noted here that there is an increase in wheat production in 2013 than what was in 2012 by 665 thousand tons, as well as a decline in the gap by about 16.4% in 2013, when Dr. Bassem Oudah, the Minister of Supply during the era of the first elected civilian President Mohamed Morsi, managed the file of wheat in Egypt.

2) Size of the gap in maize:

Egypt also suffers from a food gap in maize, where maize production was about 6830 thousand tons in 2011, 6804 thousand tons in 2012 and 6370 thousand tons in 2013. The consumption of maize amounted to 12696 thousand tons in 2011, 12009 thousand tons in 2012 and 9454 thousand tons in 2013. This resulted in a gap in maize by 54% in 2011, 43% in 2012 and 32.6 in 2013.

3) Size of the gap in sugar:

Sugar production in Egypt reached about 2057 thousand tons in 2011, 2057 thousand tons in 2012 and 1892 thousand tons in 2013, whereas consumption of sugar amounted to 2938 thousand tons in 2011, 3010 thousand tons in 2012 and 2167 thousand tons in 2013. This resulted in a gap in sugar by 30% in 2011, 31.7% in 2012 and 12.7% in 2013. It is clear that the gap declined in 2013 by about 19% against the previous year and fell significantly compared to previous years in an unprecedented way, despite lower production and lower consumption, too. This may be attributed to good management of “the available”, for consumption.

4) Size of the gap in vegetable oils:

The gap in the vegetable oils is considered significantly high, where it reached 75.8% in 2011, 81.2% in 2012 and 67% in 2013. It is also noted that the gap declined in 2013 against 2012, as well as the previous years.

5) Size of the gap in overall meat:

Egypt suffers from a gap in the overall meat (red and white), where consumption is growing larger than the production rates. The overall meat production amounted to about 1582 thousand tons in 2011, 1672 thousand in 2012 and 1655 thousand in 2013 whereas the consumption reached 1826 thousand tons in 2011, 2012 thousand tons in 2012 and 2016 thousand tons in 2013. This resulted in a gap by 14.4% in 2011, 16.9% in 2012 and 18.9% in 2013.

The increasing agricultural and food deficit:

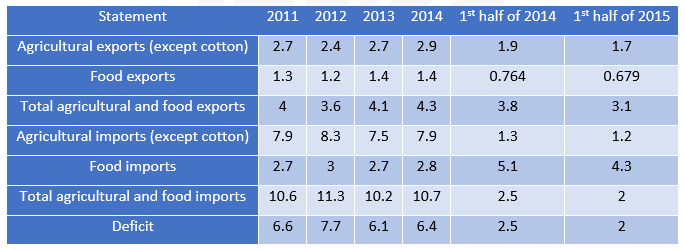

The data of the Ministry of Trade and Industry’s International Trade Point show that the agricultural and food deficit between exports and imports during the period between 2011 1nd 2014 ranged between $ 6.1 billion and $ 7.7 billion. Below is a review of detailed data during this period, monitoring the food gap sources in Egypt:

Egypt’s Agricultural and Food Exports and Imports during the period 2011-2014 (Values are in $ billion)

Sources: The table has been derived and prepared by the researcher from the published data on the site of Ministry of Trade and ommerce’s International Trade Point: link

We notice a drop in the Egyptian agricultural exports for the agricultural imports over the years of the comparison period, due to Egypt’s dependence on the import of a set of strategic goods, including wheat and grain. The agricultural imports ranged between $ 7.5 billion and $ 8.3 billion, whereas the agricultural exports were very low, between $ 2.4 billion and $ 2.9 billion.

In the context of the Renaissance Dam crisis and the possibilities of its great influence on Egypt’s share of the Nile waters during the coming period, it is likely that it could affect negatively the Egyptian agricultural sector performance. Therefore, there are expectations of an increase of Egypt’s agricultural and food imports, in light of another indicator that is not less important than the expected shortage of water, i.e. the high rates of the over-population which will significantly contribute to the increasing consumption rates.

When we compare the data of the first half of 2015, concerning the performance of the Egyptian agricultural exports and imports, with the corresponding period of 2014, we find that there is a deficit amounting to about $ 2 billion. But here it has to be borne in mind that the final data may lead to a deficit rate approaching the performance of the last four years.

There is no doubt that the dollar crisis experienced by Egypt due to lack of resources of foreign exchange may cast its shadows on reducing the volume of imports of agricultural and food commodities with the end of 2015.

In this regard, there is an important note with respect to the year 2013, during the era of President Morsi, whose declared strategy was that Egypt should produce its food, medicine and weapons.The data in the above table, which was derived from a governmental entity, show that the Egyptian agricultural and food exports rose from $ 3.6 billion in 2012 to $ 4.1 billion in 2013, whereas the agricultural and food imports decreased from $ 11.3 billion in 2012 to $ 10.2 billion in 2013.

The positive data in 2013 was reflected in reducing the deficit in Egypt’s foreign transactions in the field of agricultural and food products. The total deficit in this sector decreased from $ 7.7 billion in 2012 to $ 6.1 billion in 2013. The deficit rose again in 2014, under the military coup, to $ 6.4 billion.

Risks of the continuing food gap:

There is a number of risks that raid the Egyptian citizen, in the absence of a program to bridge the food gap, plaguing Egypt for years, due to dependence on abroad, which leads to more dependency, and exposure to the vagaries of international markets. Following is a review of some of those risks:

1) The rising food prices:

Despite the low prices in the international markets during the last period, yet the situation is inversed in Egypt because of the dollar crisis. The citizen bears the cost of the importers’ purchase of dollars from the black market rather than to enjoy lower prices on the world markets.

2) The increasing dependence on abroad:

This made Egypt fall under the weight of the risks of the food-exporting countries of vagaries of the climate or due to political conditions, which leads to negative decisions towards continuation of food export. Egypt suffered more than once from those risks with Russia and other countries. In fact, Egypt itself resorted to preventing the export of rice due to the water crisis.

3) Internal social and political instability:

Scarcity of goods or providing them at high prices has a direct impact on the low-income people and the poor, whose numbers are increasing with the passage of time in Egypt, especially in light of the deterioration of economic performance under the military coup.

XX- Uncovering the Truth of Egyptian Balance of Payments Deficit

According to the Central Bank of Egypt (CBE) data for the fiscal year 2014/2015, the foreign exchange resources amounted to $ 84.6 billion, whereas the total payments of foreign exchange reached $ 80.9 billion, achieving a surplus of $ 3.7 billion.

What is wrong here is that the foreign exchange resources include what Egypt obtained of grants and loans during that fiscal year. The weakness of this fault appeared in the data of the first quarter of 2015/2016, when the value of the Gulf support significantly dropped and the balance of payments surplus turned to a shortfall of about $ 3.7 billion, which means that the deficit is expected to exceed $ 15 billion by the end of 2015/2016.

In Economics, the surplus or the deficit cannot absolutely be made this way, as this is considered a deliberate misleading to the public opinion. The truth is that each transaction was registered twice in the balance. Therefore, it is considered amplification of the accounts to reflect improvement of the economy performance, contrary to the truth. In fact, the current account which includes the transaction items of goods and services is the one which should be the measurement criteria.

According to the US Reserve Bank, the balance of payments deficit was calculated, considering the deficit of the exports and imports as being in goods only until 1993, after which the deficit of exports and imports in services was added, which is known as the current balance.

Odder still, the US Federal Bank determined that this is the official statement, the news agencies were required to publish, to prevent any misunderstanding or wrong estimates concerning the situation of the US economy. This shows the actual volume of the exports and imports. In fact, uncovering the disease is the first step towards its treatment.

With an in-depth look at the balance of payments data, published by the Central Bank for the year 2014/2015, we find that it showed a rise in the trade deficit to $ 38.8 billion, an increase of $ 4.3 billion, earned from the deficit in the trade balance for the year 2013/2014. The question is: Why is there a deficit increase? Is this deficit temporary and can be cured throughout this year or the coming years? Or: Is it a chronic deficit?

To give answers to these questions, we need to look at the exports and imports figures. The data showed that there is a decline in exports to $ 22.1 in 2014/2015 against $ 26.1 billion in the previous fiscal year, due to the decline in the oil prices, as the oil exports represented about 27.9% of the total exports.

The total exports are extremely low. The exports outcome reached $ 29 billion eight years ago in the fiscal year 2007/2008. This means that Egypt is on the verge of a difficult stage due the global tendency to lower the oil prices in the world market. The question now is: Could a country have one third of its exports of a raw material such as crude oil? What is harder is that Egypt’s imports of oil have become bigger than its oil exports. Not only this, but the oil sector has become a burden on the foreign currency resources after it was one of four important sources of the hard currency income.

Not to mention that the deficit in oil will affect the electricity generation in Egypt, as 90% of stations are operated by using one of oil derivatives. Everybody knows the negative effects of the accident of the Russian aircraft downing on the Egyptian territories, concerning tourism in Egypt this year, in addition to a decline in the Suez Canal revenues and the big decrease of the Gulf support to $ 2.7 billion against $ 11.9 billion in the previous fiscal year. The Gulf support will continue to decrease due to the decline in the oil prices and the wars supported by the Gulf States in the area in 2016.

On the other hand, the imports payments increased to about $ 61 billion, nearly at three times of the exports, due partly to the increase in imports of non-oil goods by about $ 2 billion.

We cannot, under any circumstances, modify the Egyptian pound rate against the US dollar. It is natural that we can reduce the luxury commodities, either by raising the customs tariffs or even using the quota style to reduce these imports entirely. However, the coup government does not want to stop the luxury of the ruling class but actually bestows them with innumerable things to the extent that Egypt imports dogs and cats in a society that 40% of them live under the poverty line. However, the big deficit in the balance of payments will make the Central Bank indifferent to restrict imports and accordingly it will not be able to control the dollar rate.

It is expected that there will be a rise in the US dollar rate as a result of this chronic deficit in the balance of payments. In fact, this chronic deficit is just a symptom of a disease as long as the coup continues with its policies of ousting the producers by causing problems to them, in order to reinforce the Army’s control over all the aspects the economy, monopolizing the market and stifling all the doors of free competition in the economy, which ultimately leads to the fall of the Egyptian economy in the abyss.

The continued crisis of the balance of payments deficit in Egypt led to the following negative results:

1) The continuation of the dollar crisis: The black market in Egypt will witness a state of sale-ability during 2016 and the Central Bank may find itself compelled to raise the deposit ceiling for individuals and companies to afford their import cost needs after the bank’s failure in management of the dollar provision under the exacerbation of the balance of payments deficit and the decline in dollar resources: of tourism, exports, the Suez Canal revenues and the remittances of the Egyptians working abroad.

2) The natural consequences of the dollar crisis and the black market recovery are price inflammation and significant rising of inflation rates. In light of the budget deficit and the government attempt to adjust its position to sign an agreement with the International Monetary Fund, there will be no action concerning a rise of the wages of the government employees so that they will be capable of facing the inflation rates.

3) Due to the austerity measures, announced by the Gulf States, and the high cost of living there, the dollar transfers of the Egyptians working in the Gulf are expected to decline because of the negative impact on their savings. This will have its impact on Egypt, where these conversions manage the needs of about 5 million Egyptian families. The Egyptians working in the Gulf States will have no choice but to pressure their expenses to cope with the negative developments in the Gulf, and there will be significant possibilities of increasing the recession rates in Egypt.

4) This atmosphere of inflation and recession imposes a deflationary policy on the economic management in Egypt, in order to take some steps including the Central Bank’s decision to restrict the imports and demand the importers to provide bank credit for their imports by 100%, concerning the commercial goods other than the medicine and the baby milk supplies. If the case of the deflationary policy imposed itself on the Egyptian government, the head of the Central Agency for Mobilization and Statistics (CAMS) statements complete the darkest picture of the future of the Egyptian economy, at least in the short term. The head of the CAMS indicated the increase of unemployment and inflation rates during the past period, reaching 12.9% and 12% successively.

(N.B. Part 5 of this documentary file will start with: Petroleum Imbalance and Economy of the Rentier State in Egypt.)