Egyptian Military & Destruction of Economy – 5

(In Part 4 of this documentary file, the writer addressed: External Funding and Egypt’s Losing Bets for Achieving Development, External Funding and Egypt’s Losing Bets for Achieving Development, Crises of Living Besiege Egyptians in the Coup Era, Food Gap in Egypt Intensifying, and Uncovering the Truth of Egyptian Balance of Payments Deficit.)

XXI- Petroleum Imbalance and Economy of the Rentier State in Egypt

Although Egypt has been included among the Petroleum Exporting Companies, since the second half of the seventies of the twentieth century, yet it did not enjoy membership of the Organization of Petroleum Exporting Companies (OPEC), due to its small export share and that it does not possess large amounts in terms of production or export.

Since declaration of Egypt as of the Petroleum Exporting Countries, Egypt has experienced crises in petroleum supplies. The fuel prices were raised more than once, which caused political and social unrest. However, the situation now is a real crisis roiling the Egyptian regime because of the dependence on the vagaries of the international oil markets.

Oil exports returns remained one of the most important sources of foreign exchange until 2008, when the government of Ahmed Nazif made decisions pertaining lifting the state subsidy of the intensive-energy industry within four years. However, the occurrence of the global financial crisis prevented the coming of these decisions into effect.

Unfortunately, the oil export revenues have been used to cover the state budget needs. It is worth mentioning that these needs of the budget have been consumer needs since the implementation of Egypt’s economic reform program in 1991/1992.

The petroleum export revenues as well as other resources such as the dollar remittances of the Egyptians working abroad, the fees of transit through the Suez Canal and tourism, were not used well in productive projects. Even the map of the petroleum contracts for research, exploration or extraction was not changed to engage in an advanced stage of oil products refining, especially that Egypt possesses the technical components necessary to do so. Instead, Egypt remained as it was exporting crude oil and importing oil derivatives. However, the Egyptian oil refineries remained as they were without any development and Egypt continued to import oil derivatives instead of benefitting from them in refining imported crude oil which would certainly be cheaper than to import oil derivatives.

Egypt also did not have the infrastructure necessary for natural gas use requirements. The Egyptian government depends on a wrong strategy related to insistence on gas export, although it was advised through all evidences as well as energy experts’ recommendations that it should not export the natural gas, but to keep it for meeting future needs.

Petroleum balance deficit

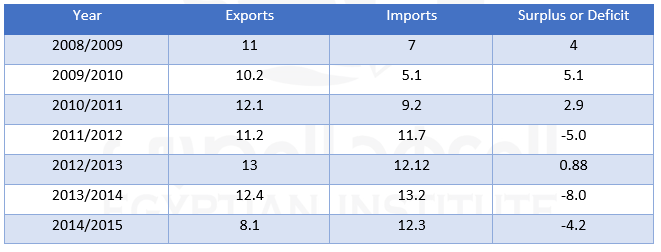

The data of the monthly financial report for November 2015, published on the Ministry of Finance site describes the evolution of the petroleum trade balance (the petroleum exports and imports), during the period from 2008/2009 to 2014/2015. Below is a review of the components of this period and conclusion of what is shown of analyses to explain the critical situation of the petroleum resources in Egypt:

Petroleum Exports and Imports in Egypt during

The period from 2008/2009-2014/2015

(The value is in $ billion)

Source: The Ministry of Finance, the monthly financial report. The data was collected by the researcher from Table: 38, on page 65 of the report.

It is to be noted according to the above table that the best of the years in the petroleum balance in Egypt, during the years of comparison, was 2009/2010, when the surplus reached $ 5.1 billion. This is attributed to the start of the recovery of the oil prices in the international market, after the global financial crisis that took place at the end of the year 2008, which accordingly led to the improvement of the Egyptian oil exports returns.

After that year, the problem began to appear in the Egyptian economy, where the development requirements and the needs to energy for the production and service projects increased, resulting in the decline in the petroleum balance surplus to $ 2.6 billion in 2010/2011.

With the increasing energy consumption in Egypt during the period 2010/2011-2014/2015, the petroleum balance showed a deficit, with the exception of the fiscal year 2012/2013, despite the political anxiety that accompanied the presence of the first elected civilian President in Egypt’s history Dr. Mohamed Morsi. Though the consumption rates in homes and the commercial sector witnessed a crisis in fuel provision during that year (2012/2013), yet the fuel for industry was provided, which led positively to an increase in exports. Moreover, the country headed during that year towards thinking and searching for petroleum substitutes of other sources, in addition to searching ways to save energy consumption and the employment of natural gas as a cheaper and environmentally-better alternative, even though it was manageable through import.

However, it is to be noted that in spite of Egypt’s obtaining of a petroleum support estimated at about $ 8 billion from the pro-military coup Gulf States in 2013/2014, yet the results of the petroleum balance for that year shows a deficit of $ 800 million, which means that the petroleum balance deficit was expected to increase by an amount equivalent to the value of the Gulf support.

According to the 2014/2015 figures, which the Ministry of Finance data said they were preliminary figures, they show that Egypt’s petroleum deficit reached around $ 4.2 billion, despite the decline in oil prices in the international market by 60%. Meanwhile, the Egyptian government carried out a program to reduce subsidies in the public budget, starting from July, 2014, particularly with regard to fuel and petroleum. The decline in fuel subsidies during that year reached about LE 50 billion.

Exploring the oil crisis in Egypt

The data on the petroleum deficit in Egypt show that the policies with respect to oil and natural gas in Egypt, which have been followed s far, are wrong policies. The government did not realize as from the beginning of the third millennium what is facing Egypt of challenges, related to development and the increase in Egypt’s consumption of petroleum products by 3%. Egypt also had long overdue in the adoption of real programs for the use of the alternative energy. The governments of the military coup in Egypt are not different from the previous ones of Mubarak’s era. The dimensions of treating the crisis revolve in the orbit of the financial crisis, resulting from Egypt’s needs of petroleum, not all requirements of development. However, a natural gas field in the north of Egypt was compromised in favor of a British company. An agreement was also signed with Cyprus and Israel, excluding Egypt from participation in a large natural gas field in the Mediterranean region.

Egypt is now moving towards the import of natural gas from Israel. At the time when Egypt is signing contracts through loans and by direct contracting on the establishment of power stations, the fact that these stations could be operated only by fuel was ignored by the Egyptian government. The government even did not consider how to provide this fuel in a transparent manner.

Unfortunately, it is clear that Egypt is lacking the infrastructure for the importation of natural gas, which forced it to hire boats for the conversion of the imported natural gas. The government did not even think about the rehabilitation of the Egyptian ports infrastructure, necessary to import the natural gas in the long term.

Egypt remains captive to debts related to the oil crisis. It has recently been published that the debts owed to the foreign companies operating in Egypt in the oil field increased to about $ 3 billion against $ 2.7 billion before, in spite of the coup government’s employment of local and regional banks to pay about $ 4 billion for foreign oil companies.

This indebtedness will remain a sword of Damocles against Egypt, because of the nature of the production contracts that grant foreign companies a share ranging between 40% and 60%. Moreover, the entire Egyptian share of natural gas production was waived in favor of the British Company, in the field located north of Egypt, in return for Egypt’s purchase of the entire production of the field at a price 2 dollars less than the world price per million BTUs.

The problem in Egypt remains that things are run away from a strategy, within the framework of the “day by day” policy, no matter the cost of the financial and developmental burdens were, in spite of being not consistent with Egypt’s current or future potentials. Moreover, Egypt continues to rely on the support of Gulf States, in the field of petroleum supplies. Saudi Arabia has recently announced that it will offer about $ 8 billion to Egypt over the coming years in the field of investment and imports of petroleum.

XXII- Dimensions of the Increasing Gap between Energy Production and Consumption in Egypt

The issue of energy is considered a central issue because of its relation to the future of development as well as meeting the community needs of fuel to conduct the requirements of their living. The life of Egyptians with its various aspects is connected to the constant flow of energy on a regular basis.

However, in light of the data of the Central Agency for Public Mobilization and Statistics, it is noted that the energy crisis is on its way to take more negative dimensions, which will affect the Gross Domestic Product and change the living style of the Egyptians who are suffering under the current conditions of the high rates of inflation, unemployment and poverty.

The statistical bulletin of the Central Agency for Public Mobilization and Statistics for December, 2015, shows that there is a gap that is viable for widening between Egypt’s production and consumption of energy over the period between May and October, 2015. Egypt’s total production of oil and natural gas reached 34.6 million tons during the period from May to October, 2015, while Egypt’s consumption of oil and natural gas amounted to 37.1 million tons during the same period. Thus, the gap between production and consumption was 2.5 million tons by 7.2%.

Reading these figures may not reflect the energy crisis correctly. The ratio of the difference between production and consumption does not exceed 7.2% during the period in question. The fact is that Egypt does not control the production entirely in terms of ownership. The producing companies get no less than 40% of this production, so if we wanted to reach the real numbers and see the deficit between production and consumption of oil and the natural oil in Egypt, we have to reduce the value of the production share of the foreign partner to reach then approximate results concerning the gap between the production and consumption up to 47% – 50%.

The reality of the foreign partner share appeared when the Egyptian government resorted to buying the foreign partner’s share to cover its needs of energy, which put Egypt in the trap of accumulated indebtedness to these companies. Whatever was repaid of debt shares by the military coup government to the foreign companies operating in the field of oil production, they were immediately replaced by new debts, so that these companies would continue doing its job in the production process. These companies threatened previously to pull out of Egypt or stop work in the oil and natural gas production, unless they got their financial dues.

According to the data of the Central Bank of Egypt for 2014/2015, Egypt’s petroleum exports represented 40% of the total exports of goods, which amounted to $ 22 billion. The petroleum imports to Egypt during the same year reached 20% of the total imports, which amounted to $ 60.8 billion. Concerning the performance of the exports and imports during the first quarter of 2015/2016, the Central Bank of Egypt data showed that the petroleum exports represented 32% of the total commodity exports which amounted to $ 4.6 billion whereas the Egyptian petroleum imports reached 20% of the total imports which amounted to $ 14.6 billion.

Perhaps, the accurate follow-up of the period of the data, available in the bulletin of the Central Agency for Public Mobilization and Statistics, can put us on the evolution of the crisis. Therefore, we will review them through the following table:

Egypt’s Consumption of Petroleum and Natural Gas

(In thousand tons) during the period (May-October), 2015

Source: The data of the table was compiled by the researcher through the CAPMS bulletin for December, 2015, Table 19, page 5.

– It is noteworthy that the month of July was the highest among the months of the period in terms of the amount of production, with a share of 5626 thousand tons. However, the average monthly production during the period in general was about 5773 tons.

– In terms of consumption, the month of July also represented the highest month of consumption among the months of comparison by about 6359 thousand tons. The lowest month in consumption among the months of the period was May, with a share of 6101 thousand tons. The average monthly consumption during the period amounted to 6197 thousand tons.

– The gap between the production and consumption during this period in terms of percentage was in September as the highest percentage among the months of comparison by 10%.

The dimensions of the growing energy gap in Egypt:

1) The financial dimension is one of the most important dimensions for Egypt at this time, when Egypt suffers from a gap in resources and a large financing gap. As for the resources gap, Egypt suffers from the value of the commodity and the service imports, estimated at $ 32 billion.

Perhaps the decline in the oil prices in the global market is considered one of the most important opportunities for the Egyptian government to reduce the payment bill of the energy gap. However, we should evoke Egypt’s crisis of its non-capability of immediate payment, which prompts Egypt’s purchase of its energy needs at higher prices, in return for what it gets of credit facilities; or borrowing to be capable of immediate payment.

2) The Egyptian economy components during the coming period will be subject to the performance level of prices in the global market. In the case of the price increase, it will be reflected on the levels of goods and services prices, as well as on the goods prepared for export. In both cases there would be lack of competitiveness of goods and services produced in Egypt.

3) The gap also describes the size of culpability of the military coup against the Egyptian people because of signing two contracts concerning the production of natural gas; one in the north of Egypt, where Egypt’s share of production was waived in favor of the British Company, and the other one was in the waters of the Mediterranean Sea, where the coup government signed an agreement excluding Egypt from participation in this largest natural gas field, under geographical range claims, in favor of Israel and Cyprus.

4) It is feared that the performance of the Egyptian parliament, which holds its first session on January 10th, towards the Egyptian government policy concerning energy, adopting or approving them, which means increasing the gap between the production and the consumption of energy dramatically. In fact it is a gold opportunity for the parliament to decline the agreement signed by Adly Mansour when he was occupying the position of the interim President of Egypt in the transition period after the military coup.

5) The governments of Egypt under the military coup are still heavily dependent on the Gulf’s role in the supply of Egyptian oil needs whether in the form of grants and aid, or through medium-term credit contracts. It must be taken into account that the Gulf States adopt this policy for political considerations the region is going through. On the other hand, the low oil prices make the Gulf States willing for the existence of a buyer for their oil, under the state of the increasing oil supply in the global market and its low prices. However, when there is an opportunity of oil prices improvement, the Gulf States will then re-consider their stances, which will put Egypt at that time in a big crisis.

We can say that Egypt will suffer during the coming period from the problems of water and energy shortage, which will put it in a critical economic situation.

XXIII- Tax Imbalance Continuing under the Military Rule

Tax returns represent an important aspect of the general revenues of the state. In addition, they do several other tasks, including the achievement of social justice, contribution in the achievement of the goal of equitable distribution of wealth. Taxes are also used in other economic areas, including the protection of domestic industry through the reduction of tax rates on certain industries in order to encourage and protect them in the face of foreign products.

Unfortunately, the situation in Egypt reflects an upside down state in the tax performance of all the previous missions. This was evident in the crisis of the state budget of decline in revenues and in not keeping pace with what was included in the budget of public expenditure, resulting in a worsening of the budget deficit crisis.

There is a general note on the tax structure in Egypt that all estimates of tax returns in the state budget are overpriced. The real figures show a sharp decline in the earned taxes against the budget estimates, which means creation of a state of confusion for the maker of the fiscal policy. This also indicates poor technical estimation by the Ministry of Supply despite the existence of cadres who are capable of doing this at a high degree of precision. However, it seems that this comes within the political employment framework, so that the budget deficit should not appear as a great figure and lead citizens to despair, though this despair is achieved at the end of the year with the final account data.

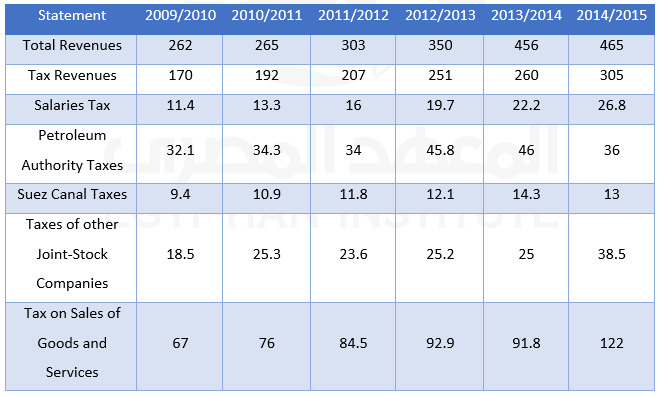

We will give evidence to the previous result through the data of the Egyptian Ministry of Finance’s monthly financial report for November, 2015, where the data published in Table (12A), page 28 explain that clearly. The estimates of the total budget for the public revenues in the fiscal year 2014/2015, were LE 622 billion whereas only an amount of LE 465 billion was actually realized, according to the final account statements, a decline of LE 157 billion, by 25.2 of what was estimated.

As for the estimates of the total tax revenues in the budget, they were LE 422 billion, while only an amount of LE 305 billion was actually earned, a drop of LE 117 billion, by 27.7% of the previously estimated number.

The same thing is applied to all tax revenue data: the tax estimates on income profits and capital gains were LE 158 billion in the budget of the same year, while only an amount of LE 129 billion was virtually achieved, a drop of LE 29 billion, by as much as 18% of the estimated number in the budget.

The general sales tax on goods and services were estimated in the same year at LE 184 billion, while the actual collected revenues were only LE 122 billion, a decline of LE 62 billion, by 33.6% of the estimated number.

Manifestations of Tax Imbalance

Data of Some Tax Sources in Egypt during the Period

Between 2009/2010-2014/2015 (The value is in LE billion)

Sources: The data of the table was compiled by the researcher through Table No. 21/A, page 28 0f the monthly financial report of the Egyptian Ministry of Finance for February, 2015.

It is to be noted from the data contained in the table that there is a great disparity in tax burdens load on various segments of the society, reflecting the bias in favor of the rich at the expense of the poor. We will discuss this in the following points:

– The proportion of the tax revenues contribution to the total public revenues reached between 64% and 65% during this period, which shows how important the tax revenues are to Egypt and that any imbalance occurs in these revenues could lead to a confusion of the state general budget.

– The tax revenues derived from the salaries of the employees amounted to LE 26.8 billion in 2014/2015 while the taxes earned from the Suez Canal revenues reached only LE 13 billion, which means that the taxes earned from employees were twice the number of those earned from the Suez Canal revenues. Moreover, the taxes on salaries of the employees amounted to 70% of the total taxes earned from the taxes on the joint stock companies in the same year, including the public and private sectors companies.

– The increase in the taxes on the salaries of employees between 2009/2010 and 2014/2015 amounted to about LE 15.4 billion, an increase rate of 135% while the tax increase earned on the joint-stock companies (public + private) during the period of comparison amounted to about LE 20 billion, an increase rate of 108%. This means that the difference of the value earned from the two groups reached LE 4.6 billion in favor of the joint-stock companies. In terms of percentage, the tax increase on salaries was 27% higher than the increase rate earned from the joint-stock companies.

– It is due to the bad omen of the military coup in Egypt and its poor economic management that the taxes earned on the Suez Canal revenues declined to only LE 13 billion in 2014/2015 against LE 14.3 billion in the previous year, which means that the decline amounted to LE 1.3, a rate of 9%.The data of the period from 2009/2010 to 2013/2014 showed an increase in the tax returns from the Suez Canal. Undoubtedly, it is expected that there will be a drop in the tax returns on the fees of passing through the Suez Canal during the coming years, because of the decline in the canal’s revenues in general, as well as the increase of its commitments in light of the burden of the debts of financing the project of the new Suez Canal Shunt, which reached LE 64 billion as well as an annual interest of LE 7.5.

– One of the manifestations of the tax imbalance is that taxes on the joint-stock companies (private + public) amounted to LE 38.5 billion in 2014/2015, while the tax on the sales of goods and services amounted to LE 122 billion, equivalent to more than three times the tax revenues earned from the private and public joint-stock companies. This is an evidence of the lack of efficiency in the Egyptian tax organ, due to its reliance on the collection of indirect taxes such as the sales tax, as well as the emergence of default in the collection of direct taxes from the big joint-stock companies.

Among evidences of the unfairness of the tax system to the poor in Egypt is that the sales tax gets such great value equally from the rich and the poor while the taxes of the rich achieve less amounts, due to their ability to evade them or settle their accounts in crooked ways.

The issue of tax reform remains neglected on the agenda of the military coup. After talking about the progressive tax, it was “undone” despite the few slides this tax was supposed to earn from. The collection of the taxes on the stock market transactions was postponed while the real estate tax was activated, with the exception of the civil institutions owned by the army including clubs, restaurants and tourist institutions.

It is not expected under the new parliament, which was “elected” under the military coup, that the legislative agenda will include any tax reforms. The administrative reform inside the tax organ will also be away from the interests of the new members of parliament, who will keep on the path of the vice-Mubarak, seeking jobs for their relatives and acquaintances in the Tax Authority.

XXIV- Poor Direct Gulf Investments in Egypt

The direct foreign investments in Egypt at this stage are of great importance in light of the funding crisis, experienced by Egypt. The alternative to these investments is the expansion of public debt either internally or externally, which is another problem Egypt fears of its economic and social consequences. The ceiling of expectations and dreams was at its peak, following the military coup in Egypt in July, 2013 towards the direct Gulf investments flows; that some Gulf media men declared that the Gulf States would pump investments of $ 100 billion into Egypt if Sisi, the commander of the military coup, came to power as president of Egypt.

However, the reality was different and those dreams have vanished; the Egyptian economy found traditional performance of the Gulf investments. Even the increase of Gulf investments in Egypt witnessed by the year 2014/2015 was very humble, about $ 2.4 billion.

Describing this amount as humble was due to several reasons; first, that Egypt needs at least $ 20 billion of direct foreign investments, according to estimates of some officials. The second thing is that this amount which the Gulf States pumped was of little value, compared to the foreign investment wallets of these countries. The third thing is that the United States alone pumped equivalent of 87.5% of what the Gulf States pumped of investments in Egypt in the same year.

The nature of the foreign investments in Egypt

In general, the foreign investments in Egypt need to be reconsidered, as its component does not lead to achieving a breakthrough or significant change in in the performance of the Egyptian economy. A rate of 60% of these investments goes to the extractive industries (of oil and gas) , a rate of 36% is directed to service sectors, such as construction and tourism projects, and 4% at most is the share of the industrial sector.

The direct foreign investments did not achieve a boom in Egypt in terms of increasing the exports, the elimination of unemployment or in bringing technology. The dominant feature of direct foreign investments in Egypt, especially those that came out of the extractive industries, was the contention of local industries, and many of them sought for the establishment of a monopoly position in the Egyptian market, as happened in the detergent industry and some of the food industry. Some of the Gulf investments have recently taken the same path when they started to go towards the food industries in Egypt.

The dominant feature of the Gulf investments in Egypt is that they are in the framework of the tourist and real estate projects, and some of them in the light of the privatization projects, which suffered many problems during the last period, because of suspicions of corruption, where the Egyptian Judiciary issued rulings of the invalidity of the majority of contracts of the Gulf deals and projects of selling the factories that were privatized.

The implications were clear after the military coup in Egypt, with respect to the orientation of the Gulf States’ direct investments in Egypt, when Saudi Arabia and the United Arab Emirates were the first to call for the Conference of Donors in Egypt, after the elections that brought the leader of the commander of the military coup as president of Egypt. The Gulf States performance in Sharm El-Sheikh Conference in March, 2015, receded to a Gulf program of deposits to support the foreign exchange reserves with about $ 6.8 billion, as well as some petroleum grants and cash.

The Gulf States presence in the conference’s investment contributions was missing. It is to be noted that some of the projects that were associated with UAE companies did not enter into force and announced their failure, as was the case with the one million housing-unit project as well as the new capital project.

The reality of Gulf investment flows in Egypt

In light of the available data, we find that it is appropriate to look at the reality of direct Gulf investments in Egypt during the period from 2010/2011 to 2014/2015, due to the stance of the Gulf States’ support of the military coup in Egypt since July, 2013.

We also believe that it is appropriate to make a comparison between the performance of the five Gulf States and the United States in the field of direct investment flows to Egypt, in order to show that there is a role, drawn carefully to the nature of the aid or investments offered to Egypt from abroad. These investments and aid were meant to serve as relievers of the situation in Egypt. They should not enable the country to come out of its economic crisis, so that its role as a regional power would remain under control.

This result was taken for granted with regard to the United States and other countries towards Egypt over past decades. However, the new thing this time was that the Gulf States practised the same role, in a clear political employment framework, especially in light of the political and economic developments, witnessed by the Middle East region recently.

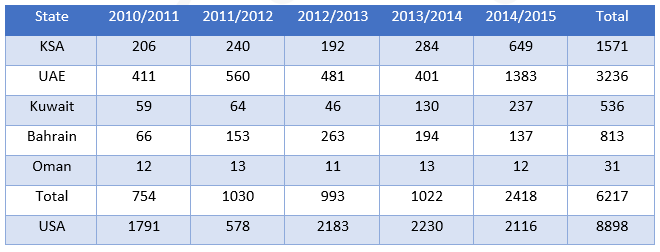

The Direct Gulf Investments Flows to Egypt

During the Period (2010/2011-2014/2015)

(The value is in $ million)

The source: The table was collected and prepared through the data of Table No. 37, page 61 of the monthly financial report of the Ministry of Finance for November, 2015.

Through the data of the above table, we find out a number of facts on the situation of Gulf States’ direct investments to Egypt, in comparison with similar investments pumped by the United States during the same period. Following are the most important items of the comparison:

– The year 2014/2015 was the highest among the rest of the years in terms of the flow of direct Gulf investments to Egypt, an investment value of $ 2.4 billion, while the year 2010/2011 was the lowest, an investment value of $ 0.75.

– The UAE tops the Gulf States in terms of the value of direct investments in Egypt, about $ 3.2 billion over the period from 2010/2011 to 2014/2015, followed by the Kingdom of Saudi Arabia, about $ 1.5 billion. The investments of the UAE and KSA represented a ratio of 77.3%

– The year 2014/2015 is considered the highest among the years of the period in terms of the value of the Gulf investments in Egypt, reaching $ 2.4 billion. It is also the only year that the Gulf investments exceeded the American investments in Egypt, amounting to $ 2.1 billion.

– Over the five-year period of comparison, it turned out that the five Gulf states, supporting the military coup in Egypt, pumped direct investments to Egypt of $ 6.2 billion, while the USA alone pumped $ 8.8 billion, thus surpassing the Gulf States in direct investment flows by $ 2.6, an increase of 43.1%.

– The average annual flows of direct investments from the Gulf States to Egypt during the period was about $ 1.24 billion, while according to this indicator, the US direct investments flows reached about $ 1.77 billion, which means that the direct investments of USA in Egypt was more important than those of the Gulf States in terms of the value.

– It can be said that Egypt’s bet on the Gulf States’ direct investments flows during the coming period is a failed bet, in light of what the Gulf States are going to face of difficult economic situations, due to decline of the oil prices, the recent raging crisis between Iran and the Gulf States, in addition to the emphasis on the strategic rooted view towards Egypt, ‘to remain captive of want and need’, and that the investments offered should not meet its requirements for achievement of development or renaissance.

XXV- Decline of Exports and Its Impact on the Increase of Unemployment in Egypt during the Period (2011-2015)

The Egyptian exports witnessed a consecutive decline in exports during the period (2011-2015). In 2011, the exports amounted to about $ 31.574 billion, which fell to $ 29.339 billion in 2012, then to $ 28.735 billion in 2013 and to 26.771 billion in 2014. The total exports fell in the first half of 2015 to reach $ 11.225 billion, compared to $ 14.148 billion in the first half of 2014, a decline rate of 23%. This is reflected directly on the size of employment in Egypt, especially in sectors which have seen a marked decrease in the volume of exports.

To find out the impact of the decline in exports on the rate of unemployment in Egypt, it is required to identify the structure of the Egyptian exports, and know: which goods are exported?, what are the sectors that can absorb employment?, how big is the decline in the exports of these sectors?, and how far did this decline affect employment in each sector?

The petroleum exports decreased from $ 9.237 billion in 2011 to $ 7.548 billion in 2013 and then to $ 6.261 billion in 2014. The oil exports also declined to $ 2.112 billion during the first half of 2015 against $ 3.471 billion in the first half of 2014, a decline rate of 39%.

The data show that the commodity exports in 2013/2014 represented about 9.1% of the Gross Domestic Product. The oil exports accounted for 47.7% of the total commodity exports, reflecting the weak contribution of the oil sector in the GDP on the one hand, and the inability of this sector to absorb a large number of employment and reduction of its relative importance in employment, on the other.

The non-oil commodity exports also witnessed a consecutive decline. In 2011, they amounted to about $ 23.326 billion and fell to $ 22.856 billion in 2012, a decline rate of 2%. They then decreased to $ 22.090 billion in 2013, a decline rate of 3%. In 2014, the non-oil exports in goods achieved a 1% increase, reaching 22.261 billion. In 2015, there was a collapse in the total exports, reaching $ 15.361 billion, a decline rate of 31% against the previous year. The total exports also fell in the fourth quarter of 2015, reaching $ 1.429 billion against $ 5.060 billion in the fourth quarter of 2014, a decline rate of 72%.

The impact of the decline in the non-oil exports on employment appears through recognition of their contribution to the GDP, the employment and the degree of employment flexibility for the size of exports. The rate of the non-oil exports to the total exports reached about 53.3%, which reflected directly on the size of employment in Egypt, especially in the sectors that witnessed a prominent decline in the volume of their exports.

As for the relative importance of the structure of the non-oil commodity exports, the data of 2014 indicates that the industry of the chemical products and fertilizers ranks first with a rate of 22%, followed by the construction materials with a rate of 21%, the food industry with 16%, the engineering commodity goods and electronics with 12%, while the contribution of the leather, footwear and leather products industry comes in the last place with only 1% of Egypt’s total non-oil exports.

The main commodity exports which plunged in value were in the sector of chemical industries and fertilizers, which declined from $ 3.74 billion in 2011 to $ 3.552 billion in 2013 and then $ 3.124 billion in 2014. They also decreased from $ 1.793 billion in the first half of 2014 to about $ 1.005billion in the first half of 2015, a decline rate of 44%. The exports of this sector constitute 22% of the total non-oil commodity exports. About 16.3% of the total employment rate in Egypt, a number of 2570500 workers, worked in the manufacturing industries sector in 2015.

It is a very low percentage compared to the employment in agriculture and fishing, which are estimated at 6.7025 workers, by about 28% of the total employees. The manufacturing sector also witnessed a decline in the growth rates because of continuation of the partial or total halting of a great number of the industrial establishments.

The construction materials sector occupies the second position in the structure of the non-oil commodity exports at a rate of 21%. Data of 2015 indicated that the rate of the workers at the construction and building sector reached 14.4% of the manpower. This sector has a medium importance as a contributor to GDP, and its operational flexibility, relative to the size of the exports, is high. It must be pointed out that it is extremely important to note that the production in the construction sector is mostly for local consumption, and thus it is not affected by the shocks that occur in the foreign trade.

The food industry sector occupies the third position in the exports structure by 12.5% of the non-oil exports, which increased to 16% in 2014. It achieved exports of $ 13330 million in 2011, which decreased to $ 1220 million in 2012. The exports increased to $ 1412 million in 2013 and to $ 1443 million in 2014. Then, they decreased to $ 679 million during the first half of 2015, compared to $ 764 million during the same period in 2014, at a decline rate of 11%.

The labor force working in agriculture and food-related industries constitutes 30.2% of the country’s workforce. In spite of its importance, this sector suffers from big problems, the most important of which are: the poor infrastructure available to the industry, intensity of foreign competition and its weak competitiveness in overseas markets, as well as the low wages in the manufacturing industries in general.

The textile and garments sector also contributed with about $ 3.437 billion in the non-oil exports in 2011, at a rate of 15.39%. This contribution decreased to $ 3.1 billion, at a rate of 14% of the non-oil exports. The exports of the sector declined in the first half of 2015, reaching $ 1431 million, compared to $ 1530 million during the same period in 2015, at a decline rate of 6%.

This decrease in the volume of exports is due to a number of problems, the most important of which are: the low infrastructure quality, the negative impact of the political and security turmoil that followed the January 25 Revolution, particularly after the military coup on July 3, 2013, and the consequent rise in transactions costs, related to the exports of the sector, due to higher cost of freight and its delay, as well as the deterioration of the cultivation of cotton locally, which adversely affected the production of the sector, especially in the face of the rising prices of the domestic cotton, compared to what can be imported from other countries such as India and Pakistan.

(N.B. Part 6 of this documentary file will start with: Funding For Youth Projects Implicates the Egyptian Banks.)