Carnegie Endowment for International Peace has published an article titled: “Egypt’s Shaky Investment Climate” by Brendan Meighan, a macroeconomic analyst focusing on the Middle East. The article addresses the situation of direct foreign investments in Egypt, especially after the Egyptian pound flotation, the IMF package of loans to Egypt, and the government’s lifting of the subsidy on fuel.

The Egyptian government’s reluctance to loosen its grip on private sector industries has impeded the flow of foreign direct investment into the country

In 2017, the Egyptian economy saw an influx of foreign currency following the implementation of a foreign exchange liberalization in conjunction with a series of structural reforms and an IMF loan package. The hard currency shortage, which had slowly ground the economy to a halt, was finally over. However, after eighteen months of turbulent economic changes, foreign investors have shown remarkably little appetite for long-term investment in the Egyptian economy. Over the course of 2017, the government touted the central bank’s rapidly increasing foreign exchange reserve levels and broadcasted new debt sales to much fanfare. Despite the big talk from the government, investment in rapidly maturing government securities is no indication of long term financial stability and security, as this money can exit the economy almost as quickly as it entered.

A much more robust indicator of economic improvement is foreign direct investment (FDI), which usually takes the form of longer-term business investment. It can both improve Egypt’s current account balance by increasing the economy’s ability to export and reduce the stubbornly high unemployment rate. Foreign direct investment did rise to $7.92 billion during the 2016/2017 fiscal year, up from $6.93 billion during the previous fiscal year, but it did not reach the government’s $10 billion target. Private multinationals are likely biding their time to ensure that the promised reforms can bring about substantive changes to the economy. As many major international firms already have some sort of presence in Egypt, there is little advantage to be gained from increasing investment too quickly. While Minister of Investment Sahar Nasr has talked up the prospects of higher FDI flows for the current fiscal year, there is little evidence of an improvement. The latest FDI data from the government (traditionally about nine months out of date) actually shows a decline in net FDI compared to the same period the year before.

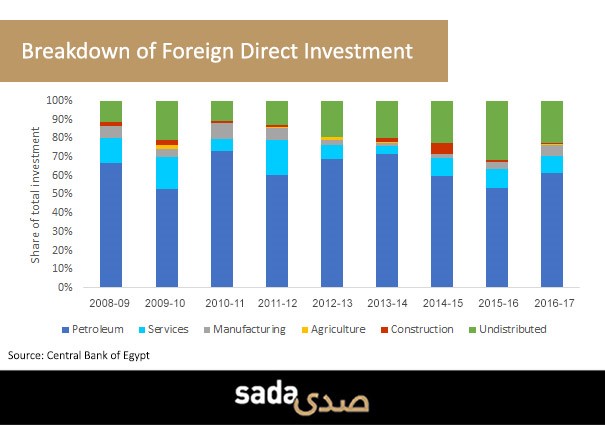

Investment outside of oil and gas extraction has been weak. According to calculations based on data from the Central Bank of Egypt, FDI in the non-petroleum sector of the economy actually fell from $3.24 billion in the 2015/2016 fiscal year to $3.07 billion in fiscal year 2016/2017. Part of the decrease may be due to the uncertainty following the currency float by the Central Bank of Egypt, but the data indicate that this did not impact petroleum investment. Due to the large capital investments required for the exploration and production of oil and gas, especially for offshore projects in the Mediterranean, the petroleum sector has always accounted for a disproportionate percentage of FDI in Egypt—even prior to the discovery of the massive Zohr gas field in 2015. While the sector may be doing quite well overall and contributes greatly to Egypt’s topline macroeconomic indicators, the petroleum sector employs relatively few Egyptians. Growth in the petroleum sector has not and will not directly translate into gains for most of Egypt’s population of more than 90 million. This is particularly troubling when factoring in Egypt’s unemployment rate of 11.8 percent and an official labor force of only 29.5 million Egyptians.

The Egyptian government’s reluctance to loosen its grip on private sector industries has impeded the flow of foreign direct investment into the country. Figure 1: Breakdown of Foreign Direct Investment

Figure 1: Breakdown of Foreign Direct Investment

Increasing investment in the manufacturing and services sectors can benefit a broader swath of the population, as these sectors can more easily integrate local Egyptian labor into their production processes. However, the manufacturing and services sectors only saw $495 million and $752 million of FDI, 5.8 percent and 9.5 percent, respectively. By attracting more foreign investment in the manufacturing and services sectors, Egypt can still reap the same macroeconomic benefits it gains from the petroleum sector by increasing exports and decreasing imports, resulting in a reduction in the trade deficit. But manufacturing and services provide additional upsides as well. Foreign investors can take advantage of the young and relatively cheap labor force in Egypt, which directly addresses the unemployment situation, a purported goal of the government. And by moving more Egyptians into formal employment, the government’s tax base will be broadened, thereby reducing the budget deficit.

The Egyptian government itself is an obstacle to greater FDI. A recent Reuters exposé on the murky role of the military in the Egyptian economy indicated that the military owns dozens of businesses, although it remains unclear how much of the overall economy they control. Other government entities also compete alongside private participants in sectors such as banking, tobacco, and fertilizers. Government participation in the private sector puts private firms at a major disadvantage. State-owned enterprises in Egypt are often exempt from charging customers a value added tax on their purchases and can operate at a loss indefinitely, undercutting private participants. Private companies, especially those which report back to shareholders, are obligated to maximize profits and are rarely afforded the kinds of privilege and government access state owned firms receive.

The government has announced plans to sell off pieces of these entities over the next several years, particularly those in banking and energy, through initial public offerings on the stock market. This would be a step in the right direction, but the size and scale of the government’s involvement in the private sector will remain substantial, even if all the prospective IPOs actually take place. There is still substantial uncertainty regarding the IPO plans as the stakeholders in these businesses have no incentive to sell and the government may just be seeking to alleviate the concerns of foreign lenders. Outside of cases of market failure and industries absolutely vital to national security, there is little macroeconomic justification for the government and military to be running companies when the private sector can provide the same services in a more efficient manner. This is a major hindrance of private investment, especially from foreign firms less familiar with the Egyptian market place. As the government moves further away from free markets and representative democracy and towards a bald-faced enrichment mechanism for the military elites, the incentives for foreign investment will dwindle.

Egypt is no longer in the grips of catastrophic economic crises, nor is it still enduring the aftermath of much needed structural and macroeconomic reforms. Inflation has begun to die down and the central bank has started to lower interest rates, improving domestic investment conditions. The focus of the Egyptian government now needs to be set on extricating itself from the manufacturing and services sectors through sales of state owned enterprises and enticing foreign investment to fill the gaps. By doing this, they can improve the unemployment rate while maintaining growth and develop a more inclusive and sustainable economy. This is an absolute necessity, as Egypt’s population is poised to surpass 100 million in the coming years. Unfortunately, instead of exploiting its position to fully integrate into the global market place, Egypt appears ready to consign itself to growth through rent seeking and resource extraction.