The recently issued Standard & Poor’s global rating report has updated some significant about the Egyptian economy, especially in the area of public debt and its annual growth rates and total values, with important expectations for the current year[1].

This paper will attempt to review the figures related to Egypt in the Standard & Poor’s report, most notably:

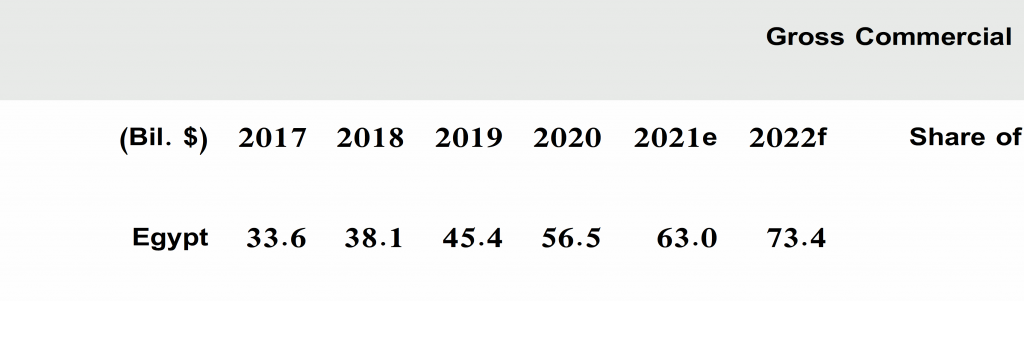

1- Egypt borrows $73.4 billion during current year:

The report notes that its debt figures focus on central government debts, excluding local government and social security debts, as well as debt of other public bodies and government-guaranteed obligations.

The estimates of the commercial debt figures include borrowing via bonds issued either in listed markets or sold as private deposits, in addition to commercial bank loans. Also, the report does not include government debts that may be issued by some central banks for monetary policy purposes.

The figures in the Standard & Poor’s report refer to the annual Egyptian sovereign loan figures from 2017 to 2022, including expectations during 2022. The figures included in the report’s Table 2 are for long-term loans, which means that by adding short-term debts due during the year, they will exceed the mentioned figures. It should also be noted that these figures of borrowed funds include foreign debt bonds in foreign currencies and the domestic debt in local currency, but do not include foreign loans from international institutions or bilateral loans.

Reviewing the table figures, the following can be deduced:

– The report monitors the annual leaps of Egypt’s sovereign debt. While Egypt borrowed $33.6 billion dollars in 2017, the loans increased to $38.1 billion in the following year, and then to $45.4 billion in 2019, which means that the annual increases are limited to less than $5 billion annually, but the boom started in the year 2020, where Egypt borrowed $56.5 billion, a ten-billion increase than the previous year, which illustrates the great crisis of the repercussions of the Coronavirus on the Egyptian economy, a crisis that became more violent in 2021, when Egypt borrowed 63 billion dollars, an increase of about $20 billion than the year before the outbreak of Coronavirus. It also indicates the increasing reliance of the Egyptian state on borrowing from abroad.

– Talking about Egypt’s intention to borrow $73.4 billion this year as long-term debt, an increase of 10 billion dollars than the previous year, seems consistent with the above escalation of figures, as well as in light of the continuing repercussions of the Coronavirus and the crisis of the war on Ukraine. However, this remains an estimated figure that could further escalate in light of the continuation of the war in Ukraine or any other international emergency factors. The figure is also likely to escalate in light of the most recent great exit of foreign investments in debt trade or hot money (some estimate the volume of these investments at about $15 billion), due to the interest rate hike, with the rise in the inflation rate in Egypt, which renders these investments useless, taking into mind that the interest rate in Egypt is likely to increase with the expected rise in the US interest rate as well as the inflation rate in Egypt.

– The current budget deficit (the difference between revenues estimated at EGP 1 trillion and 365 billion, and expenditures of EGP 1 trillion and 837 billion) is approximately EGP 500 billion , equivalent to approximately $33 billion at the exchange rate of 15.5 pounds per dollar, according to the dollar price at the beginning of the fiscal year, which will be borrowed through domestic debt instruments, and therefore, according to the estimated figure in the report, about $40 billion remain, which will be borrowed from abroad as long-term loans, mostly through foreign currency bonds, in addition to the short-term loans required to meet urgent needs, as well as loans from international institutions and bilateral agreements.

– In light of the huge surge in the annual Egyptian sovereign borrowing, which amounted to $33.6 billion in 2017, compared to about $73 billion expected for the current year, an increase of nearly $40 billion, and with the continuing repercussions of the growing global crises and the local economy’s inability and mismanagement, the occurrence of another $40 billion increase over the next two years is largely expected, which means that Egypt may need at least $110 billion in sovereign debt in 2024 and possibly 2025.

– These booms are not due to the above reasons only, but also as a natural result of the due payment dates of installments and interests. It is also irrefutable evidence of the inability of the regime to develop economic activities through which it can repay a percentage of those dues abroad, as well as its inability to manage dollar resources. To cover the worsening deficit in the trade balance and the general budget, commercial loans are supposed to provide financing for productive activities that generate a return that allows for the repayment of loans and their interests, and accordingly raises the gross domestic product, not to be used merely to repay previous loans or to cover the deficit in the general budget and the trade balance.

– The S&P report indicates that Egypt’s total sovereign debts will amount to $391.8 billion by the end of this fiscal year, compared to $348.4 billion at the end of last fiscal year, which means that the sovereign debt will rise by $43.4 billion, despite the fact that Egypt will borrow $73.4 billion, which means that about at least $30 billion of new debts will merely go to pay off previous debts, nothing more.

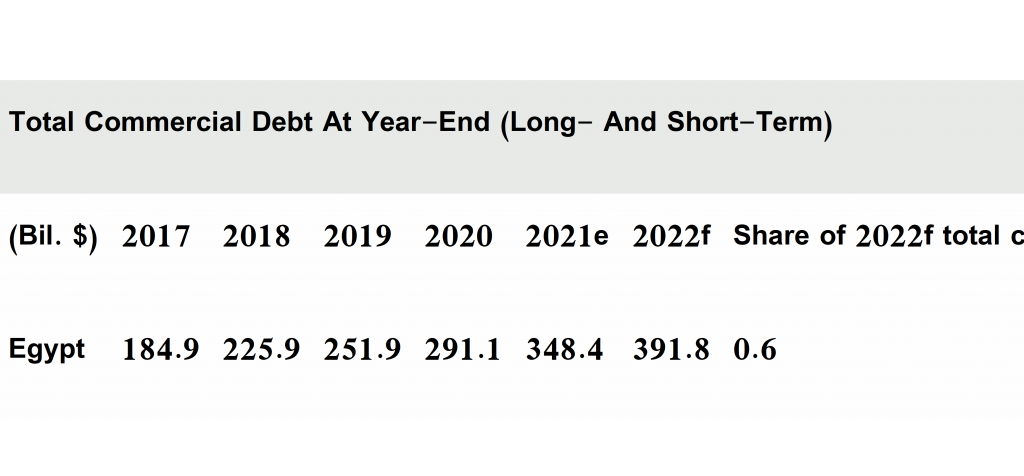

2- Egypt’s total commercial debts:

The figures mentioned in the report’s Table 3 indicate the evolution of the total Egyptian public debt, both external and internal, of commercial loans during the period from 2017 to the current year.

Accordingly, it has become clear that:

– The Egyptian public debt has increased from $184.9 billion in 2017 to likely $391.8 billion by the end of this year, which means an increase of more than 100% in just five years. Even at the calculation of the real figures of 2021, the increase is close to 100% (i.e. the figure has doubled) in just 4 years.

– The figures also indicate huge and escalating leaps, but this sharp escalation is evident in 2020, an increase of $40 billion compared to the previous year, and nearly $53 billion as an expected boom for the current yearcompared to the previous year.

-Following up the figures of the rise in the total public debt, as well as the rise in the sovereign debt, reviewed above, compared to the increases announced by the Central Bank of Egypt (CBE) in the volume of foreign debts, an increase by about 5 to 10 billion dollars on an annual basis on average only, indicating frantic increases in the domestic debt (in local currency) as a result of the booms in the sovereign debt relying on debt instruments, and as a result of the persistence in external borrowing through bilateral loans or from international institutions.

– The existence of huge spikes in the Egyptian domestic debt increases during the last five years, confirms the government underestimation of the repercussions of both domestic and external loans on the country’s economic future, in addition to the apparent general trend of excessive reliance on loans as a primary and sustainable source of financing, which makes the economy permanently exposed to global crises.

– It is expected that Egypt’s total commercial debts by the end of 2022 will amount to $391.8 billion. Based on the analysis in the above item that concluded that the economy requires borrowing $110 billion as sovereign debt at the end of 2024 or 2025, Egypt most likely needs approximately $150 billion (an additional increase of about $40 billion) to meet the required financing needs, whether from through bilateral loans or from international institutions, or even through privatization processes or through deposits of sister countries in the CBE.

– It can be emphasized here that the total public debt due on Egypt will rise in no more than two years to reach half a trillion dollars, which means that it will certainly exceed the gross domestic product, amounting to EGP7.9 trillion, about $503 billion, at an exchange rate of 17.7 pounds per dollar, as the general budget indicates. However, there is a lot of exaggeration in the estimates of the GDP itself, given that the GDP for the previous year did not exceed EGP5 trillion, that is, no more than $290 billion, so how may such miraculous boom happen?!).

– The above data means that the value of public debt has already exceeded the GDP, especially with the decline in growth estimates for the current year due to the successive domestic and international crises.

– Every Egyptian citizen will be indebted more than $3,900 by the end of 2022, i.e. more than EGP71,000, according to the current exchange rate. With the strong potential decline in the value of the Egyptian pound under the weight of the urgent needs for foreign exchange, and with the large increase in internal and external borrowing booms referred to above, the citizen’s share of the total sovereign debt will most likely exceed $7,000 within two years, that is more than EGP135,000 in debt to each citizen at the current exchange rate.

3- The general budget burdens of repayment of interests and installments of both external and internal debts:

Egypt’s total debt installments and interests in the current fiscal year amount to about EGP 1.172 trillion. When this sum is deducted from the public budget’s total revenues, which amounts to EGP 1 trillion and 365 billion, only EGP 213 billion remains, to be spent on public expenditure items in various sections of the Egyptian budget, which means that the total debt service from installments and interests exceeds 85% of the state’s total revenues this fiscal year, and that only less than 15% of revenues remain for public spending, which requires management of the rest of the public spending needs from other sources.

The report indicates that the interests of Egyptian debts devour about 44% of Egypt’s general budget revenues, according to Figure 5a in the Standard & Poor’s report. This indicates that the bulk of the country’s budget goes as interest for the debts that Egypt borrowed from foreign institutions and banks, which highlights the great predicament that the country’s general budget is currently experiencing. According to the report’s figures, this situation will certainly continue, perhaps for several decades to come, in light of the transformation of a significant proportion from Egyptian loans to long-term loans.

It is certain that the total premiums and interests will be expected to increase over public revenues in the coming fiscal year, which means that Egypt needs to manage its public expenditures completely from outside the budget, in addition to the repercussions of conclusions of surges in domestic and external debt, which may indicate that the burden of debt service (premiums + interests) will exceed 150% of the volume of public revenues by the end of the next two fiscal years only.

According to the analysis that concludes that public revenues will not be enough to pay the burden of debt service, it is logical that the state will continue to ignore spending on investment activities in its human resources in the health and education areas, and perhaps even a decline in public spending on them to exacerbate the poor quality of service provided to citizens in this direction.

Also according to this conclusion, it can be said that the state’s revenues directed to public investments will also diminish, but with the state’s keenness to complete the show-motivated megaprojects that it started during the past few years, which entrenches the need for more external and internal borrowing, and the burdens of debt service will increase, noting that the interest in these megaprojects will be accompanied by a severe neglect of ordinary public investment projects.

4- Egypt accounts for 0.6% of total global commercial debt

According to the data of the S&P report, Egypt will borrow these giant sums by issuance of bonds with large amounts, which will make it the largest demander of such debts in the Middle East, Europe and North Africa, where Egypt will account for 0.6% of the total commercial debt in the world.

Also according to the report figures, Egypt will thus exceed the total external debt of all emerging economies. However, it is significant here to note that the GDP of the countries subject to comparison should be taken into account. For example, Turkey, one of the emerging economies, accounts for 0.3% of the total global commercial debt, while its GDP is more than $800 billion, compared to the Egyptian GDP, which did not exceed $300 billion last year (supposing that the announced figures are not exaggerated), which shows the huge share of Egypt in global commercial loans compared to the size of its economy.

It is also noteworthy that in such comparisons, there should be reference to the government’s share of those debts. For example, the Turkish government’s share is less than 30% of the external debt, where the remaining percentage is owed to private sector companies, compared to a share of more than 80% of the external debt owed by the Egyptian government. The significance of this reference stems from the fact that it is easy to declare the bankruptcy of any private sector company that stops repayment of debts, based on the bankruptcy law of the country in which it operates[2], while the bankruptcy of a state has many painful repercussions[3].

[1] Sovereign Debt 2022: Borrowing Will Stay High On Pandemic And Geopolitical Tensions

[2] Egyptian Economy and the Risk of Bankruptcy: Indicators and Prospects, The Egyptian Institute for Studies, April 2022, link.

[3] The views expressed in this article are entirely those of the author’s and do not necessarily reflect the views of the Egyptian Institute for Studies

To Read Text in PDF Format Click here.