Egyptian Military & Destruction of Economy – 6

(In Part 5 of this documentary file, the writer addressed: Petroleum Imbalance and Economy of Rentier State in Egypt, Dimensions of the Increasing Gap between Energy Production and Consumption in Egypt, Tax Imbalance Continuing under the Military Rule, Poor Direct Gulf Investments in Egypt, Decline of Exports and Its Impact on the Increase of Unemployment in Egypt During the Period (2011-2015), and Decline of Exports and Its Impact on the Increase of Unemployment in Egypt During the Period (2011-2015).)

XXVI- Funding For Youth Projects Implicates the Egyptian Banks

The Egyptian economic management has been witnessing false performance and undergoing weaknesses and lack of coordination between its components since the military coup in Egypt. Abdel-Fattah El-Sisi has recently issued his orders or assignment to the Central Bank of Egypt to provide through the banking system an amount of LE 200 billion for the financing of the small and medium enterprises, possessed by young people, at an interest rate of 5%, while the interest rate in Egypt is moving to touch the ceiling of 13% for depositors and 18% for borrowers.

This is not the first time that the military intervene in the economic affairs and violate the economic rules and conventions. The project of the Suez Canal expansion was undergone upon orders from the military without introducing any feasibility studies, and the Central Bank was then hired to arrange debt securities of about LE 64 billion for the Suez Canal General Authority.

The performance of the commander of the coup in Egypt, Sisi, during Sharm El-Sheikh Economic Conference, which was held in March, 2015, was an unacceptable image for the management of the economic affairs. When the holders of exposed projects and ideas estimate the cost of implementing a particular project at a certain amount of money, he interferes asking for the implementation at lower costs. When they offer certain periods of time, ten years for example, for the implementation of a project, he asks for reducing the time to only five years, as he exactly did with the Suez Canal Shunt, which was destined to have a period of time of three years, using equipment owned by domestic companies. He ordered that it should be implemented in only one year, which led to contracting with foreign drilling and dredging companies and caused the depletion of the little reserve of foreign currency.

When we consider the economic landscape in Egypt, we should not forget the Army control over the economic potentials of the country. The Army has become a competitor with the Business Sector in the food production and the construction materials. These abuses extended to the degree of allowing the Egyptian Army to establish partnerships with foreign investors. The question is, what has remained to the civil economic society of space to work in?

The recent trend of the military coup commander’s announcement to help the youth by financing their small and medium projects at an interest rate of 5% implicates the banking system in many economic problems, which will limit its economic role and load it with costs, if not losses which it cannot endure.

Below is a review of the negative effects of this decision, including the following points:

The violation of the Central Bank independence

The military language which was used in order to carry out this decision was a misuse of the Central Bank of Egypt (CBE), which by virtue of the Constitution and the law, has its own independence to carry out its entrusted task, i.e. the monetary policy-making and economic control over the banks. The project could have been introduced in a better form, through a government program, or via a project sponsored by one of the ministries, provided that it should be clearly defined, in terms of the way of fund provision, the conditions to benefit from the project and the source of affordability of the cost difference, which the banks, accepting to enter the project, will be mired in.

Actual losses to the banks

The average interest rate that banks pay to depositors is 10%, and about 2% is added to it in the case of re-lending these deposits to investors and users of these loans, as operating expense, as well as a similar proportion as dividends to the bank, so that it can carry out its activities. Thus, the normal interest rate for borrowing from banks should not be less than 14%. The question is, how will banks bear this difference, which is estimated at 10%, or about LE 20 billion? If we imagine that the banks will be able to undertake the “impossible” and implement this project, the first losses are the returns that would have gone to the state budget as a result of profits. No bank will be able to achieve profits under the project of financing the small and medium projects of the young people at an interest rate of 5%. Neither the private sector nor the foreign banks will accept to finance such project.

Deepening the lack of competition

Among the basic rules of economics is the existence of a state of real competition among the economic operators in the market. This exception that came within the framework of Al-Sisi’s orders to the Central Bank returns Egypt back to the pre-financial and monetary reform, carried out during the period of (1991/1992-1995/1996), when there were several different rates for borrowing from banks.

And so far as the issue of the lack of competition between the projects, the cost of funding will vary among the workers in the same industry or field, as one of them obtains financing with an interest of 5% while the other gets a financing with an interest of 15%. No doubt, the one who gets a lower interest rate will have a lower cost of production of goods or services than that of others, thus there will be a lack of competition and a creation of abnormal cases of competition in the Egyptian economy.

Opening a new door for corruption

In the eighties of the twentieth century, among the doors of corruption, was that many Members of Parliament (MPs), as well as other state officials used to establish fake projects and apply through feasibility studies to specialized banks to give them loans at interest rates lower than the commercial banks, about 3% or 4%. After obtaining these loans, they used to deposit them in commercial banks to get a higher interest. When the date of repayment comes, they actually repay them after benefiting from the interest rate differences. The real loser here is economy due to absence of real goods or services, in addition to the losses borne by the state general budget through supporting the interest rates of the specialized banks.

It is natural under the great state of corruption now, to exercise the same past experience, especially that the difference of the interest rates is attractive and helps drain the bank funds, or whatever source that pays the difference of the interest rate imposed by the military coup commander.

Covering up the liquidity crisis in Egypt

It is notably that there is a liquidity crisis with the Egyptian banking system which has LE 1.8 trillion as deposits, including about LE one trillion withdrawn annually by the government in the form of bills and bonds to service the burden of the state budget deficit.

In view of the reality of this problem, which crystallizes in the government’s crowding out of the private sector in borrowing from the banking system, the banks resorted to raising the interest rates up to 12.5% and sometimes to 13% with the aim of getting more deposits and the providing a new area of new deposits.

The fact, from our point of view, is that the regime wanted to reduce the mandatory reserves of banks with the Central Bank, but within an acceptable argument, which is exempting the amounts lent to small and medium projects for the young people of the proportion of the mandatory reserves, so that it would be a natural cover for the move.

According to the figures of the Central Agency for Public Mobilization and Statistics, about 98% of the establishments operating in Egypt are small and medium enterprises, and thus it would be easy to tamper with property records for projects already in place, to meet the conditions and defraud the banks to get these discount loans.

Wrong characterization

The characterization of the problem of small and medium enterprises as a funding crisis is wrong. The issue in Egypt is the high cost of production because of dependence on abroad in providing production inputs, production lines and spare parts. The problem of financing may be one of the problems but it is not the most prominent among the problems faced by these projects. It is well known that the informal savings available in the Egyptian market are approaching in amount the actual savings in the banking system. In fact, it is easy for these projects to deal actually and significantly with these informal savings.

XXVII- The Real Value of the Decline in Suez Canal Revenues in 2015

There is a general rule which the economists usually deal with in economic analysis, i.e. “Figures describe reality, but they do not reflect facts”. So, we find that many of the figures for the macro-economic indicators in Egypt are not displayed in the proper context, in addition to hiding real data and showing false ones. This introduction is to explain what has been recently circulated of a decline in the Suez Canal revenues, by about $ 290 million, at the end of 2015; the canal revenues reached $ 5.1 billion in 2015, against $ 5.4 billion in 2014, a decline rate of around 5.3%.

Lest it is to be thought that the shortfall or decline in the Suez Canal revenues was only $ 290 million, we should necessarily explain that there are many other things that show the reality of the decline in the canal revenues in 2015, including what the Suez Canal revenues will bear of interest payment to holders of the bonds of the Suez Canal expansion, through the new shunt which was opened in August, 2015. The cost of this interest only amounts annually to about LE 7.5 billion, equivalent to $ I billion at the official exchange rate in Egyptian banks.

The decline in the Suez Canal revenues at the end of 2015 amounted to $ 1.2 billion. However, the real effective yield of the canal revenues will be about $ 4 billion, or a little less than that. The seriousness in this matter is that it comes under a severe crisis plaguing Egypt since the military coup, concerning the provision of hard currency to cover the import for consumption needs and industry requirements, as well as the services sector needs.

The decline in the Suez Canal revenues will further deepen the dollar crisis in Egypt. On the other hand, the burden of repayment of the debt of the Suez Canal Authority is not restricted only to repayment of the local bonds obligations, estimated at LE 64 billion, but the local banks also provided loans in hard currency to the Suez Canal Authority during 2015, amounting to about $ 1.3 billion, as well as $ 200 million as an annual interest on these dollar loans, owed to the local banks.

The reality of decline in the Suez Canal revenues is also reflected through the fact that the state budget obtains two types of revenues from the Suez Canal; the first of them is the tax returns on the canal revenues. In the light of the decreasing revenues of the canal in 2015 and repayment of commitments of debt interest on its loans, there will undoubtedly be a significant decline in tax revenues accruing to the benefit of the state budget on the annual Suez Canal revenue.

The monthly report of the Ministry of Finance for November, 2015, shows that there is a noticeable decline in the tax revenues derived from the Suez Canal Authority during 2015, by about LE 1.3 billion, compared to what it was in 2014. The earned taxes on the Suez Canal revenues reached LE 14.3 billion in 2014, but dropped to LE 13 billion in 2015.

The second thing, related to the impact of the decline in the Suez Canal revenues on the state budget, is that the non- tax returns are earned on what is left of the canal revenues, representing an important revenue of the state general resources. According to the data of the same report, it is clear that the Suez Canal revenues reached LE 19.2 billion, within non-tax revenues in the general budget in 2014/2015, compared to LE 18 billion in 2013/2014.

Here, we should confirm that the data recorded on the fiscal year 2014/2015 took into account the exchange rate difference, which reduced the value of the Egyptian pound against the dollar. Thus, the canal revenues appeared with an increase of LE 1.2 billion, which is not actually a result of a real rise, but due to the drop in the Egyptian pound value, or the so-called exchange rate differences.

Giving the economic management of the military coup in Egypt a free reign to confuse the Suez Canal revenues, including the consequent escalation of the dollar crisis and the decline in Egypt’s foreign exchange earnings, is unacceptable, especially after the foreign currency resources in Egypt was negatively affected in more than one area, such as the tourism revenues, turning the surplus in the petroleum sector into a deficit for years, and recently the noticeable decline in the dollar transfers of the Egyptians working abroad, as indicated by the data of the first quarter of the fiscal year 2015/2016, by $ 417 million. This decline is also expected to escalate in light of the economic crisis of the Gulf States.

The effect on the budget’s general revenues, in general, will be devoted to the worsening of the public budget deficit crisis, which represents a challenge to the Egyptian governments under the military coup.

Under the decline in the Suez Canal revenues and the consequent decline in the budget’s public revenues, the Egyptian citizen expects that the public services will undoubtedly be affected. Actually, this is apparent in the higher inflation and the price rise of several commodities and public services.

Further decline

Economists used to classify the Egyptian economy, a period of time ago, as a rentie economy in spite of the economic diversification opportunities it has enjoyed over a period of time, whether through human, natural or financial resources. However, those who managed the Egyptian economy for decades used to depend on the rentier returns without bearing the hardship of incorporation for an Egyptian development project.

Due to the nature of the Suez Canal position in the international trade equation, and being a dependent variable as a water conduit, the canal returns remain hostage to the international trade movement, which is suffering from recession and slow growth rates, due to the fragile recovery of the development rate in the global economy.

It must be taken into account that the ships passing through the Suez Canal represent only 12% of the global trade volume. Moreover, under the Chinese crisis and its expected negative connotations on the global economy, the movement of ships passing through the canal is expected to decrease due to the decline in the demand on oil from China and the rest of the world.

The question now is: Isn’t it reasonable and correct that we should refer to trial all those who wasted about $ 8 billion dollars in the Suez Canal new shunt, which did not add anything to the Egyptian economy but affected significantly its revenues because of the annual commitments, represented in the interest rate as well as the larger commitment by the end of 2016, when the Suez Canal Authority will be required to repay the basic loan to the holders of the Suez Canal bonds?

On what basis was the project’s feasibility study made? Had the decline of the Suez Canal revenues been only $ 290 million, the impact would have been less than the financial burdens resulting from the canal expansion loan, which exceeded three times of the decline in revenues at the end of 2015.

XXVIII- The Inability of Domestic Savings and Investments in Egypt

The domestic savings are the backbone of any successful development process, a fact which has been confirmed by many of the experiences of the emerging countries, whether the South-East Asian countries or China, where the average ratio of the domestic savings to the Gross Domestic Savings (GDP) ranged between 30% and 35%. In fact, the experience in Egypt reflects a large gap between the reality of the domestic savings and development requirements. While about 850 thousand persons of the new entrants flow annually to the labor market, the potentials of the Egyptian economy are unable to provide the job opportunities required for them. According to the economic estimates, Egypt needs to achieve an annual growth rate in the GDP by at least 7.5% for a period of not less than ten consecutive years, so that it can interact positively with the new entrants to the labor market, and alleviate the current unemployment which is approaching 13% of the labor force.

In order that Egypt reaches an average growth of GDP that is commensurate with the development requirements on the one hand and keeps pace with the increase in the population rate on the other, the GDP growth must be equal to three times the rate of population increase which reaches 2.5% annually. This means that the required GDP growth rate should not, in any case, be less than 7.5% per year. However, the achievement of this annual growth rate in the GDP necessitates that the domestic savings should reach 30%, so that these savings be directed to the domestic investment system, especially in the context of the productive sectors in particular, which helps in providing permanent and stable job opportunities on the one hand and reducing the pressure of dependence on imports on the other. In fact, the widening of the investment range would necessarily lead to the provision of the goods and services, especially those that are currently imported from abroad.

The Reality of Domestic Savings and Investments:

There is a big gap between the reality and the presumption (the default) in Egypt, which has been one of the performance defects of the Egyptian economy for years that intensified strongly after the military coup in July, 2013.

Following is a review of the figures of these two indicators during the period from 2010/2011 to 2014/2015 to stand on the reality of the performance of the Egyptian Economy, intensification of the unemployment problem, the increased reliance on abroad and the permanent escalation of the import bill:

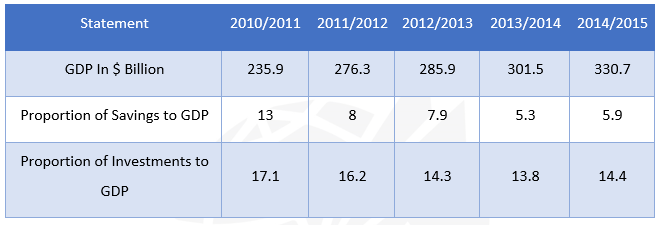

Domestic Savings and Investments as a Proportion of GDP in Egypt During the Period (2010/2011-2014/2015)

Source: The table has been prepared by the researcher from the monthly financial report of the Ministry of Finance of November, 2015 through the data published in the table on page 1

Through the data in the above table, we can notice the following:

– There is a permanent decline during the years of the period in the ratio of the domestic savings to the GDP. In 2010/2011, the rate of savings reached 13% of the GDP while in 2014/2015, this figure dropped dramatically to reach only 5.9%. This has a variety of indications, including that the incomes of citizens were no longer enough for their living requirements significantly, as evidenced by the decline of their savings to the GDP. Second, the decline in savings also reflects the financing gap that prevailed in Egypt and which made it resort to borrowing from abroad. However, the military coup government started to fill part of the financing gap through obtaining grants, aid and deposits from the Gulf States, as well as borrowing from abroad, both from the regional and international institutions or through offering bonds in the international markets.

– The decline in the ratio of savings to the GDP between 2010/2011 and 2014/2015 amounted to about 7.1%. At the same time, it is noticed that the GDP as a value increased by about $ 94.8 billion, which means that the increase was achieved through the public debt, both from inside and outside, which can be monitored through the figures of the Ministry of Finance on page 4 of the same report. The domestic debt increased during the two years from LE 808 billion to LE 1988 billion, an increase of LE 1180 billion at a rate of 146% while the external debt during the two years reached $ 39.8 billion in March, 2015, compared with $ 33.6 billion in June, 2010, i.e. the increase amounted to $ 6.2 billion by 18.4%.

It is obvious to the reader that the adoption of the financing of the gross domestic debt is one of the things that shackle development and cost the state general budget new burdens, which are also considered an extra burden on the coming generations.

– If we look at the indicator of the domestic investments in proportion to the GDP, we find that it also fell during the period of comparison, particularly after the military coup. While the domestic rate was 17.1% in the year 2010/2011, it fell to 14.4% in 2014/2015. Thus, the humility of the investment rate to the GDP reflects the reality of the humility of the Egyptian GDP in general, in a country approaching 100 million people in its population. However, there are countries, with population equal to only one-third of Egypt’s population, that achieved a larger amount in GDP than that of Egypt. For example, the GDP of Malaysia, which has a population equivalent to one-third of Egypt’s population, reached about $ 338 billion in 2014 while Egypt’s GDP only reached $ 301 billion during the same year.

– It is necessary here to stress the existence of a large gap between the domestic savings and investment in Egypt, and the importance of linking between the two indices, as the savings are the source of financing for investment. While the gap between the savings and the investments in 2010/2011 was about 3.9%, it widened in 2014/2015, reaching 8.5%, i.e. the gap between savings and investments as a share of the GDP, doubled between the two years of comparison.

Reasons for the decline in savings and investments

Undoubtedly, Egypt has been living a state of political and security instability since the January Revolution, 2011. This state intensified significantly after the military coup, and tourism was hit to killing by the incidents of violence that targeted tourists and tourist areas in the most important tourist destination in Egypt, Sinai.

With regard to savings, it is to be noted that the average GDP per capita in Egypt is still modest. In its best condition, it reached $ 3761 per capita in a year, while it was around $ 2966 in 2010/2011. This means that the increase achieved in the average per capita of the GDP after five years was around $ 795, i.e. an average of $ 159 annually. So, the domestic savings are decreasing and they are not sufficient for making the required rise for the achievement of the necessary breakthrough in the domestic investments.

With regard to investments, they suffer from many shackles in Egypt, especially in the light of the high rates of corruption and bureaucracy in the government system. The investment climate in Egypt after the military coup also witnessed a major intervention by the Army in the economic life, as well as its increased crowding out of the private sector in various economic fields.

XXIX- Egypt’s Trade Deficit with Arab Countries Increasing

There is a new twist in Egypt’s commercial relations with the Arab countries, especially the transformation of the surplus in the trade balance between the two parties from the Egyptian side to the side of the Arab states. Undoubtedly, there is a range of economic variables after the military coup which led to this negative result.

According to the data of the Egyptian Ministry of Trade and Industry’s International Trade Point, the trade surplus for the Arab States during the period from January to September, 2015 amounted to $ 989 million against around $ 264 million during the same period in 2014.

Perhaps, this is a natural consequence in the light of the decline in Egypt’s exports in general and the increasing deficit in the Egyptian trade balance after the military coup. The data of the Central Agency for Public Mobilization and Statistics indicate the existence of an increase in the Egyptian trade deficit from $ 37.1 billion in 2013 to $ 46.2 billion in 2014.

On the other hand, there are developments in the nature of the relationship between Egypt and the Arab countries, represented in the existence of preconditions by the Arab States for the economic transactions with Egypt, related to the support offered to the military coup, that it would be in kind with respect to oil and its derivatives. Moreover, the Kingdom of Saudi Arabia has recently confirmed more than once its contribution for supporting the Egyptian economy on condition that this would be only via Egypt’s import of Saudi commodities, in the light of Saudi Arabia’s support of the export program of its domestic industry.

The Arab markets have always been classified as markets that should be flooded with the Egyptian exports for considerations of geographical proximity. In addition, the Greater Arab Free Trade Agreement allowed the Egyptian exports a comparative advantage in entering the Arab markets compared to the exports of other countries. According to the data of the Egyptian Ministry of Trade and Industry’s International Trade Point, Egypt’s foreign trade with the Arab countries amounted to $ 17.1 billion in 2011, representing 18.3% of Egypt’s total foreign trade which amounted to $ 93.8 billion. The data of the year 2014 showed that Egypt’s trade with the Arab countries increased to $ 19.3 billion, representing 19.8% of Egypt’s total foreign trade, which amounted to $ 97.6 billion during the same year.

Below, we will look at data for the development of Egypt’s trade relations with the Arab countries, and a monitoring of manifestations of the decline in favor of the Arab states during the period from 2011 to 2014, as well as the first nine months of 2015.

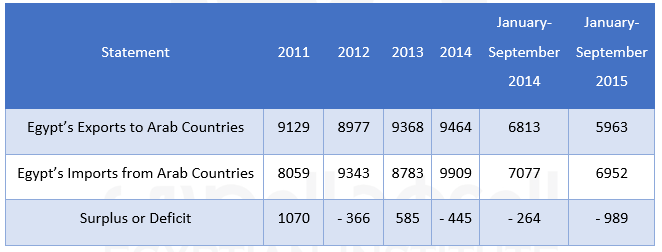

Egypt’s Exports and Imports with Arab Countries from 2011 to 2014 (The value is in $ million)

Source: The Egyptian Ministry of Trade and Industry’s International Trade Point data.

Through the above table, we notice that there was a trade imbalance with regard to Egypt’s commercial relations with the Arab countries; as the Arab market has always been a target market for the Egyptian agricultural and industrial products. This is shown clearly from the results of the trade balance in 2011, when the there was a surplus in favor of Egypt by more than a billion dollars while during the period after 2011, the result of the Egyptian trade balance changed to turn into a surplus in favor of the Arab states, with the exception of 2013, which ended with a surplus of about $ 585 million in favor of Egypt. It is to be noted that this increase was achieved during the same year of the rule of President Mohamed Morsi, the first elected civilian president of Egypt, as it was a unique year with regard to both exports and imports; the Egyptian exports increased by about one billion US dollars while the total imports decreased by about $ 3 billion.

The figures of the first nine-month period of 2015 also show that the balance of trade deficit in Egypt increased compared to the corresponding period of 2014 or even to the deficit achieved in 2014 as a whole. Moreover, the deficit reached $ 989 million during the first nine months of 2015, against $ 445 million in the entire 2014, and only about $ 264 million during the first nine months of 2014.

The Petroleum Problem

Egypt suffers from a large deficit in its energy needs. Egypt has also received, since the military coup, a Gulf support of petroleum products, whether through the free petroleum grants or through credit facilities granted by the Gulf States to Egypt over the second half of 2013, or in 2014 and 2015.

It is expected that the deficit in Egypt’s trade balance with the Arab countries as well as its imports will increase during the coming period in the light of its increasing consumption of oil and gas and the decline in its oil and natural gas production. However, if it had not been for the decline in the oil prices in the international markets, Egypt’s trade deficit with the Arab countries would have been reached very high rates.

It is also noted that the nature of the exchanged goods between Egypt and the Arab countries is “traditional” and they do not include high-tech products, tool-kits or machines because both Egypt and the Arab countries do not produce such commodities but depend on importing them from abroad. For example, Egypt exports building materials, chemicals, fertilizers, engineering and electronic goods, garments, furniture and home furnishings to the Arab countries, while it imports petroleum and its products, reinforcing steel and chemicals from the Arab countries.

There is no doubt that the Egyptian exports to the Arab countries in particular and the rest of the world countries in general will face a host of challenges during the coming period because of the economic policies which would raise the cost of the Egyptian exports, such as the high cost of energy for industry as well as the other services of water supplies and production requirements. Thus, the result of the trade balance during the coming period is expected to be in favor of the Arab countries at higher rates than what was achieved in 2014 and 2015.

XXX- Egypt’s Payments on Foreign Investment Rising

The Egyptian governments have always sung for the foreign investment and placed their hopes into it; that it is the magic solution to Egypt’s economic problems. Economic zones of various forms were created for foreign investment and legislations were enacted to open the doors widely for both direct and indirect foreign investments.

After all the years that had passed on foreign investment in Egypt, the result was negative and the “gain” that the Egyptian governments expected from these foreign investments turned into “loss”. The foreign investment did not achieve a breakthrough in the Egyptian exports or help to alleviate unemployment. It did not bring in the advanced technology or achieve stability in the stock market with regard to indirect investments, either.

The results of the balance of payments show the negative outcome of the existence of these foreign investments in Egypt. The funds that are transferred outside Egypt in the form of returns on the foreign investment, far exceeds the proceeds in favor of Egypt from its foreign investments. However, the Egyptian laws allow unconditional departure of the entire profits of foreign investors. The foreign investments did not face any problems in transferring their profits abroad except after the emergence of a problem in dollar resources, due to the decline in Egypt’s reserves of foreign currency. However, the Central Bank devoted its efforts to put an end to this problem after about six years of 2015, when the stock market foreign investors obtained their entire profits and transferred them outside Egypt.

The foreign investors did not cease to get funding for their projects from the Egyptian banks, whether during the stage of incorporation, or during operation. The Egyptian laws do not enforce foreign investors to supply the entire capitals for their projects while the complete profits exit the country under the protection of the Egyptian laws. However, this does not make a balance between gains and losses for the existence of these companies in Egypt.

Below is a review of Egypt’s proceeds and payments for investment to find out the extremely negative performance in this concern, which reflects that Egypt has turned into just a consumer market.

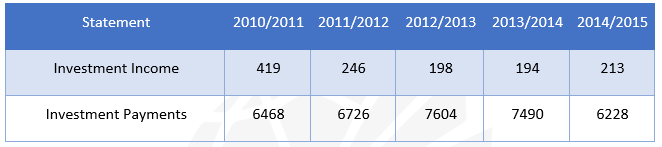

Egypt’s Income and Payments of Investment During the Period (2010/2011-2014/2015) (The value is in $ million)

Source: The Egyptian Ministry of Finance, the monthly financial report, November, 2015, Table 38, page 65.

– It is to be noted from the above table that the total revenues of Egypt’s investments abroad over five years amounted to $ 1.2 billion while what Egypt paid for the foreign investments on its territories reached $ 34.5 billion during the same period, which means that the deficit in favor of the flows of foreign investment returns outside Egypt amounted to about $ 33.2 billion and that Egypt achieved only 3.6% of the total returns of the foreign investments on the Egyptian territories that actually exited the country.

– Second, Egypt’s returns on its investments abroad amounted to $ 419 million in 2010/2011 while they decreased to $ 213 million in 2014/2015, a decline value of $ 206 million, representing a decrease rate of 49%, compared to what was in 2010/2011.

– The year 2010/2011 is the best year among the years of the period in terms of the returns of about $ 419 million while the year 2013/2014 was the worst in terms of the returns of the Egyptian investments abroad, which amounted to $ 194 million. We can conclude here that the value of the Egyptian investments abroad are very modest to the point that the returns are limited to such a degree, or that the Egyptian investors abroad prefer to keep the returns of their investments outside Egypt rather than bring them inside the country.

– The year 2014/2015 is considered the least among the years of the period in terms of payments for foreign investments by about $ 6.2 billion while the year 2012/2013 was the largest among the years of the period for withdrawal of the investment returns from Egypt by about $ 7.6 billion.

– The figures of the table reflect the impact of this matter on the dollar crisis in Egypt during the years of comparison, when the dollar resources in Egypt declined dramatically. Regrettably, the foreign investor still continues the movement of transference of his profits and returns of his investments via the Egyptian banking system, which provides him dollars at official rates. Meanwhile, this investor does not want to bear any risks for management of his profits from the black market.

– The situation of the foreign investment in Egypt remains in need of reconsideration to discuss many gaps that led to economic losses to Egypt. Egypt did not earn the desired fruit from the foreign investment, while the experience was successful in other countries, such as the Southeast Asian countries, where common interests were achieved between the two parties and each party was keen on the existence of the other.

– It is strange that the foreign companies located in Egypt announced more than once after the military coup in 2013 that they would leave the Egyptian market because of the dollar crisis, and that the banks failed to provide them necessary dollars for importing the production requirements. Meanwhile, these companies are keen on transference of their entire annual profits and do not use part of them in meeting these needs to alleviate the pressure on the banking system, as well as alleviating the demand for the dollar and reducing the exchange rate in the black market.

It is to be noted that the foreign oil companies alone got their previous dues through 2015 by about $ 5 billion, as well as the stock market investors who practiced unprecedented pressures on the military coup government in Egypt, such as their rejection of the law, imposing taxes on the stock market transactions, and threatening to get out of the Egyptian market and go to the neighboring countries which do not impose taxes on their stock market transactions.

The foreign investments in Egypt have become a burden on the Egyptian economy. After crowding out the Egyptian industry and the monopoly of markets of some important goods, concerning food and detergents for instance, the issue of the exit of profits comes to represent an important figure in the performance of the balance of payments.

The results shown by the figures in the above table are supposed to make the decision maker and the economic policy maker seek to put control on the movement of these funds so as to ensure stability of the exchange market and lead to a balance in the demand for dollar, especially that Egypt is experiencing a severe funding crisis, which gives it the right to impose exceptional circumstances, such as to allow a certain percentage of the profits of foreign investors to be transferred outside Egypt, not all the funds.

However, the economic administration under the military coup finds itself in front of a general economic crisis, where the decline in the dollar resources represents only one of its aspects. So the government exerts all its efforts to maintain friendliness with the foreign investor, without caring for consequences on the Egyptian economy.

XXXI- The Government Deprives the Egyptians of Enjoying Oil and Food Lower Prices in the Global Markets

Among the statements that many Egyptian officials used to repeat for pride, is that Egypt is part of the world and should be linked and intertwined with the global markets in prices and in the foreign trade of exports and imports. Based on this hypothesis, the Egyptians should enjoy the decreases in the prices of goods and services in the global markets. However, the fact is that the Egyptians pay only the bill of cons for merger in the global economy, including flooding and global prices for the majority of goods and services, despite denial of the second half of the equation. The Egyptians do not feel any impact of the price decline of goods, in the global markets, on the domestic markets as well as the fact that their wages are not linked at all to the global system.

According to the “Economist” magazine, the prices of food and agricultural goods declined by 40% at the global level while the prices in Egypt continued to increase. Meanwhile, the Egyptian government claims that it supports the food commodities provided to citizens, in spite of the poor services provided to Egyptians in education and health, as well as deterioration of public facilities such as roads, bridges and others.

In addition, after the rise of inflation rates to about 12% according to the government figures, corruption pursues the Egyptian citizen in the most essential elements of his life, i.e. food. Between now and then, the import of carcinogenic wheat is announced, as well as the death of large quantities of fish in the Nile, with presence of fears of diverting these dead fishes into markets. Some drinking water stations in areas of Lower Egypt governorates were closed due to the high rates of contamination of the Nile water after the death of large quantities of fish there.

Another example is the “earthquake” of petroleum price collapse, which led to a decline in the prices of oil and its derivatives all over the world, except in Egypt. Why should the oil prices decrease in the whole world except for Egypt? In the United States, the fuel prices fell to quarter, the lowest price level they reached over about 13 years. Prices in most developed countries usually take the directions of ups and downs while in Egypt the prices take one direction, which is always only going up.

However, the irony is that the government always raises prices of all goods and links them to the international prices but it does not reduce the prices when they fall in the world markets. Of course, there is no link in Egypt between local and global wages.

The government suffers from a general budget deficit due to the support provided for energy, which goes mostly to the factories of businessmen. The support of energy swells every year. After it had been about LE 40 billion, equivalent of about $ 5 billion in the budget of the year 2006/2007, it increased to about LE 125 billion in the budget of 2013/2014, LE 100 billion in last year’s budget and then was reduced to become LE 61 billion in the current fiscal year, 2015/2016.

The question now is: If the oil price per barrel dropped to less than $ 30, why don’t we cancel completely the energy support, which is directed to industry and get rid of this burden on the Egyptian budget? The military coup government had a gold opportunity to leave the energy prices to the forces of demand and supply and to improve the quality of the market in distribution of resources. However, this government, which has a network of rooted corruption with the businessmen sector, cannot make decisions that could limit the deterioration of the performance of the Egyptian economy.

It is supposed that the decline in oil prices would lead to a positive improvement, represented in reduction of Egypt’s expenditure on the petroleum imports, as Egypt imports most of its needs of oil derivatives from abroad while it exports crude oil. Undoubtedly, expenditure on imports of petroleum products should inevitably decrease, leading to increased dollar supplies. But, did this actually happen in Egypt? On the contrary, we find that the dollar exchange rate continues to increase, exceeding LE 8.67 in the parallel market recently.

The decline in petroleum prices will have various negative effects, including those which are related to direct foreign or Arab investment in Egypt. Take for example a country like Saudi Arabia, which is considered a key supporter of the military coup in Egypt. Saudi Arabia produces 10 million barrels of oil per day, and after the collapse of the price of a barrel of oil from $ 110 to $ 30, there is a deterioration of one billion dollars a day in its revenues, i.e. $ 350 billion annually. Will Saudi Arabia be able to invest in Egypt in light of the successive decreases of oil prices in the global petroleum market?!

The same thing would apply to the foreign companies; the Italian company “Eni” which announced in August of last year that it discovered the largest inventory of natural gas in the world, in Egypt, will be forced to retreat from its investments in Egypt with this drop in oil prices like; as investment in the oil sector has become useless economically. Moreover, there are strong expectations that the support of the Gulf States to the government of the military coup in Egypt will decrease due to the decline in petroleum revenues, which affected the economic situation in the Gulf States. The most prominent example for this is the lifting of oil and fuel prices in Saudi Arabia by 30% recently.

The Gulf States will not be able to support this government as it was before. What emphasizes this fact, is the coup government pursuit to borrow $ one billion from China to support Egypt’s dollar reserves, as well as its announcement of entry in a privatization program, including profitable banks and companies to cover its financial deficit, and thus sacrificing the wealth of the country and losing the role of maintaining balance in the market as well as scaling down the excesses of the private sector, through giving up the state ownership of enterprises and public banks.

The question that baffles the Egyptian citizen now is: why should the blessings turn into curses in Egypt? While the decline in the prices of energy and food in the world markets should have been a boon to Egyptians, it turned into a curse at the hands of this stricken government. Isn’t it a puzzling matter that Egypt and Egyptians are a burden on the world?

(N.B. End of this documentary file: The complete text of this documentary will be published on EIS website soon.)