Eastern Mediterranean Gas: Taking an Unpaved Road

A reading in dimensions of Egypt’s gas imports from Israel

Introduction

The discovery of Egyptian Zohr Field in 2015 was not the first large-scale natural gas discovery in the Eastern Mediterranean waters, as it was preceded by a series of significant discoveries including the Israeli fields of Tamar (2009) and Leviathan (2010), and the Cyprus field of Aphrodite – which once again highlighted power struggle on energy sources. The emergence of huge reserves of oil in the early 20th century in the Middle East led international powers to compete on consolidating their influence and building their political alliances in the region, making the Middle East one of the hottest and most tense arenas over the past decades. This time, huge reserves of natural gas have been discovered in the waters of the Eastern Mediterranean Sea at a time when natural gas is considered the primary fuel of the near future in light of the fact that the global consumption of natural gas tripled during the period from 1980 to 2010 and that demand on gas is expected[1] to grow by 50% by 2030 – taking into consideration that:

– The carbon dioxide (CO2) emissions from the natural gas combustion are much lower than those from coal or oil,

– Natural gas is cheaper than renewable energy sources,

– Natural gas’s significant role in power generation (as natural gas-powered fuel cells, reciprocating engines and turbines can generate electricity), and

– Natural gas can be transported either through pipelines or by shipping in tankers after liquefaction.

The huge gas reserves in the Eastern Mediterranean region, which are likely to expand in the future, have met the domestic needs of regional countries with a possibility to export the surplus to international markets. However, the growing demand on natural gas all over the world is likely to lead to major transformations in policies of the countries of the Eastern Mediterranean region – an extremely sensitive region that suffers from several political crises – and the creation of new maps of conflicts, alliances, and deals, most notably the gas deal between Egypt and Israel in early 2018. Furthermore, the natural gas resources in the Eastern Mediterranean have also pushed international powers towards engagement in competition and keenness on maintaining effective presence in the region.

This study aims at making a comprehensive assessment of the Israeli-Egyptian gas deal and addressing its political, strategic, and economic dimensions within the framework of the regional and international interactions in the Eastern Mediterranean region.

Egypt: Return to the arena of the Eastern Mediterranean

The first decade of the twenty-first century represented a huge boom in the production of natural gas in Egypt that allowed its transition from consumption to exporting – most prominently its deal to export gas to Israel in 2005 that raised controversy in Egypt at the time. Meanwhile, Egypt sought to build two plants to liquefy natural gas on the Mediterranean coast so that it could export its gas production surplus. However, this boom did not continue for long: after reaching the highest gas production rates in 2009, production started to decline gradually until gas consumption e90eeded production rates in the end; and in 2014 Egypt stopped exporting liquefied gas to foreign markets and started to rely on imports for meeting its domestic needs.

The Story of “Zohr” Field

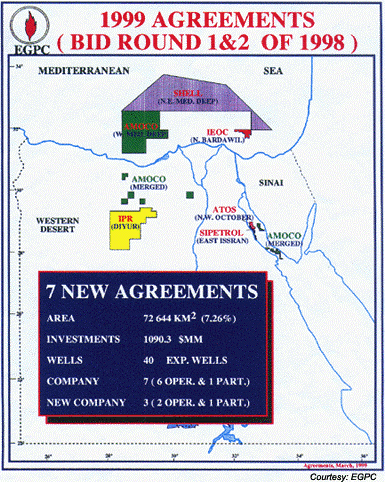

Before the huge gas reserves of Zohr Field were discovered in the “Shorouk” concession area, there had been prospection and exploration activities in the same area that had not led to major economically feasible discoveries. In 1990, Shell, a British-Dutch oil and gas company headquartered in the Netherlands and incorporated in the United Kingdom, acquired the (NEMED)[2] concession area which includes the existing Shorouk concession area and other adjacent areas located in the deep waters of the southeastern Mediterranean. (Figure 1)

[Figure 1: A map showing the NEMED concession area in the southeastern Mediterranean.]

[Figure 1: A map showing the NEMED concession area in the southeastern Mediterranean.]

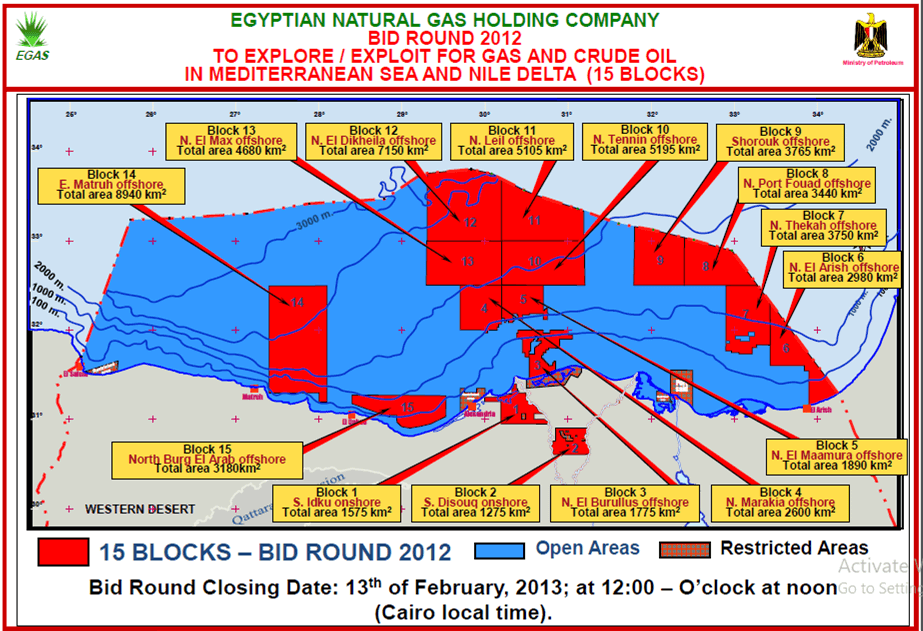

It was remarkable that “Shell” spent about 10 years trying to prove the presence of gas that could be commercially exploited, spent about one billion dollars and dug nine wells[3]. Although Shell made some gas discoveries, yet they have decided not to pursue these further due to the challenging economics of the project, as the gas reserves did not e90eed one trillion cubic feet. These disappointing results, coupled with the political uncertainty that followed the January revolution, led Shell to relinquish[4] the NEMED concession in March 2011. In January 2012, the Egyptian government through “EGAS”, a state exploration agency, divided the NEMED concession area into several blocks and announced a bid round for gas exploration[5] in these divided areas as well as several other blocks in the deep waters of the Mediterranean[6] Sea, with a total of 15 blocks (Figure 2).

[Figure 2: A map showing bid areas in 2012 (Bid Round 2012), including “Block 9” of “Shorouk”]

In April 2013, the Egyptian government announced the results[7] of the prospection and exploration bid. The offer extended by Italian Eni was accepted and it won the concession of block 9, “Shorouk”, which is in fact part of the concession area “NEMED”, which Shell had relinquished as mentioned above.

Eni’s main motive for obtaining the Shorouk concession area was to continue exploring extensions of the huge gas discoveries in Israeli fields of Tamar and Leviathan as well as Aphrodite Field of Cyprus, close to the Shorouk concession area. In April 2015, Eni[8] reached almost certain results[9] of the presence of huge gas reserves in Zohr Field which prompted it to bring the giant Saipem 10000 drilling rig to the Shorouk area and start drilling on July 3, 2015, after which the Egyptian government and Italy’s Eni announced in August 2015 the discovery[10] of the “Zohr Field” in the Shorouk concession area (Figure 3).

[Figure 3: Map showing Egyptian offshore where Eni discovered Zohr Field.]

The Zohr Field is the largest natural gas field in the Mediterranean Sea, bypassing the Tamar and Leviathan fields of Israel and the Aphrodite field of Cyprus – as the natural gas reserves in the field are up to 30 trillion cubic feet, about 850 billion cubic meters.

Interestingly, the Egyptian government on 5 July 2015, just two days after the start of drilling in the Zohr Field, had doubled[11] its gas purchase prices from Eni (under Eni’s share of extracted gas and Eni’s recovery of exploration and drilling costs), raising the price of one million British thermal unit (equivalent to 28.26 cubic meters) from $2.65 to a maximum $5.88 and a minimum of $4 – which could have been understandable compared to global gas prices[12] if the natural gas produced from the Zohr Field had been prepared for export in the future. However, this seems to be away from reality where the gas produced from Zohr will be mostly directed to domestic consumption rather than export, which is clearly visible through the Zohr Field infrastructure[13] which has been designed to pump gas produced to the local gas network and not to the liquefaction plants in Edco and Damietta to liquefy gas and export it abroad.

The coincidence between the start of Eni’s drilling activities in Zohr Field and the Egyptian government’s decision to double gas prices received from the Italian company suggests that there may have been an undeclared agreement between the Egyptian government and Eni on such move before starting drilling; as it is difficult to imagine that the Egyptian government was not aware of the presence of huge gas reserves in the Zohr Field before taking the decision to double the gas prices in favor of Eni, which opens the door to suspicions of corruption, especially that there were similar corruption cases in the past, most prominently the pricing of gas exported to Israel at very low[14] prices during the era of former President Hosni Mubarak. However, the Egyptian governments to raise gas prices in favor of Eni may have been made in the context of providing incentives to Eni in order to expedite the drilling process and development of the Zohr Field. It is noteworthy that the Egyptian government followed the same strategy[15] with other foreign companies. In its quest to attract foreign investments, the Egyptian government seems to have turned a blind eye to the fact that only local consumers will bear the price rise of natural gas.

From import to export

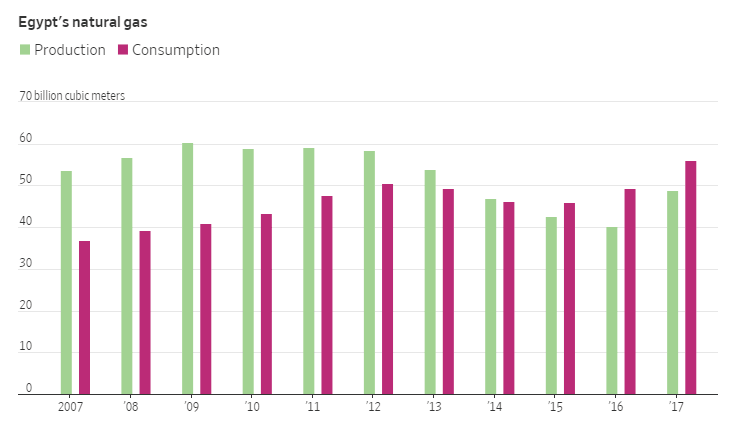

After the discovery of Zohr Field that appeared to have the largest gas reserves in the Mediterranean Sea, a key question remains about Egypt’s ability to achieve natural gas self-sufficiency and move to exporting the production surplus in the short term. This requires reviewing Egypt’s natural gas production and consumption in the last ten years (2018-2009) (Fig. 4), where Egypt reached its highest rates of natural gas production in 2009, producing about 6.1 billion cubic feet per day, which met the domestic needs and allowed the export of the production surplus abroad. However, soon after 2009 until 2015 Egypt’s gas production declined[16] by 27% to 4.4 billion cubic feet per day, turning Egypt from a natural gas exporter to a country that imports natural gas to meet domestic consumption needs. Egypt stopped natural gas exports of liquefied natural gas (LNG) in 2014 and sought to import its needs of natural gas; and the quantities imported[17] by Egypt early 2016 reached about 1.1 billion cubic feet per day. Thus, Egypt moved within a few years from exporting gas to a country that seeks meeting its domestic needs of natural gas through imports.

[Fig. 4: The diagram shows Egypt’s production and consumption of natural gas from 2007 to 2017.]

The discovery of Zohr Field has revived hope in Egypt’s return once again to exporting natural gas. In December 2017, Eni’s CEO, Claudio Deslezzi[18], said that the back field ” will completely transform Egypt’s energy landscape, allowing it to become self-sufficient and to turn from an importer of natural gas into a future exporter.” Several months after the comment of Eni’s CEO, specifically in September 2018, the Zohr Field production[19] of natural gas was about two billion cubic feet per day and Egypt’s total gas production[20] reached 6.6 billion cubic feet per day. This prompted the Egyptian Minister of Petroleum & Mineral Resources, Tarek El Molla, to announce in the same month that Egypt will halt[21] its gas imports as it was expected that Zohr Field would reach its highest rate of production[22] by 2019, reaching 2.7 bcfd. Egypt’s total gas production in 2019 is expected to reach 7.3 billion cubic feet per day, taking into consideration that Egypt’s consumption[23] of natural gas by the end of 2018 was estimated at about 6.3 bcfd, which means that in 2019, Egypt will not only achieve self-sufficiency of natural gas but also to return to the arena of natural gas exporting countries, albeit in limited quantities. We should refer here to the agreement that Egypt and Jordan signed in August 2018 to resume natural gas export to Amman in early 2019 as the first agreement[24] to export Egyptian natural gas after a period of halt since 2014.

Egypt’s return to exporting natural gas also means its return to operation of Egyptian LNG plants; as Egypt has a natural gas liquefaction infrastructure that gives it a competitive advantage[25] compared to other Eastern Mediterranean countries. It is noteworthy that the two Egyptian natural gas liquefaction plants in Damietta and Edco on the Mediterranean coast, have been stagnant over the last few years after the decline in domestic production and the halt of natural gas exports; however, in light of self-sufficiency and return to the export of Egyptian natural gas, it is expected[26] that by the end of 2019 the two plants will operate at full capacity.

An important question remains about Egypt’s ability to sustain self-sufficiency in the medium and long term, which we will discuss in detail through this study.

Israel and the search for a strategic choice

Israel from a natural gas importer to a net exporter

In 2009 and 2010, Israel announced huge discoveries of natural gas reserves in the Mediterranean Sea through the Tamar and Leviathan fields. The Tamar natural gas reserves are estimated at 11 trillion cubic feet and its production started[27] in 2013, while the natural gas reserves of Leviathan field are about 22 tcf, and its production is expected[28] to start in 2019. These huge discoveries not only gave Israel the ability to satisfy its domestic consumption, but they also allowed Tel Aviv to move from being a net importer of natural gas in the past years to a net exporter, in the near future.

The most complicated challenge for Tel Aviv was how to invest its natural gas output from the fields of Tamar and Leviathan. Despite the huge reserves of natural gas that Israel has, the biggest challenge was to find ways to access the external market, taking into consideration that Israel does not have pipelines to transport its gas surplus to consumers abroad or even gas liquefaction platforms for exporting it via tankers. Of course, the Israeli government had to look for the best options to overcome these obstacles within the framework of the political, security, and economic determinants.

Multiple options and a single strategic choice

Despite the many options available to Israel for exporting the newly discovered natural gas reserves, most of these options included a range of potential political, security, and economic risks and different relative weights. Below are some of the options available to Israel in this regard:

1- Establishment of natural gas liquefaction plants on the Israeli coasts: This option has major security concerns taking into consideration that these plants may be permanently exposed to attacks by the Palestinian resistance, in addition to their high economic costs. Another option for Tel Aviv is to establish floating platforms for the liquefaction of its natural gas output in the Mediterranean Sea, which is also extremely expensive compared to the natural gas liquefaction plants on coasts which are also very costly, with a continued potential security threat.

2- Transferring natural gas to Cyprus via pipelines and then exporting it through gas liquefaction plants on the Cypriot territory. Although this option is safer than the presence of gas liquefaction plants inside Israel, yet political obstacles are strongly present; because Israel’s reliance on Cyprus as a major route for the flow of gas from Israel will remain a constant concern for Tel Aviv amid the Turkish-Cypriot crisis and its complexity that affects the political situation in Cyprus. On the other hand, the extension of a pipeline from Israel to Cyprus and the establishment of natural gas liquefaction plants on the Cyprus territory will require considerable financial cost and more wasted time, which does not serve Israel’s interest in accelerating steps for benefiting from the surplus of its gas production

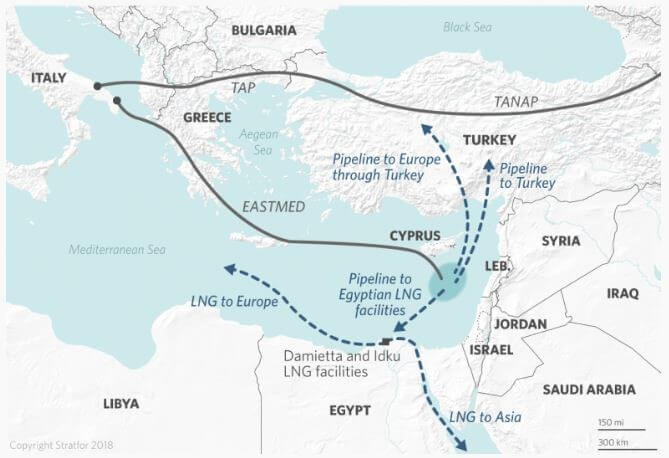

3- Construction of a pipeline to link Israel, Cyprus, Greece, and Italy, including the export of gas to the European markets: This option faces enormous challenges in terms of the high cost of the building of a pipeline of 2100 kilometers at a cost of about 7-8 billion dollars, taking into consideration the technical difficulties facing the extension of deepwater gas pipelines, as well as the expected opposing Turkish position. However, despite all these challenges, the four countries – Israel, Cyprus, Greece and Italy – signed a memorandum of understanding[29] in December 2017 for the construction of a gas pipeline to Europe, and the signing[30] of the official contract between the four countries is expected in February 2019. We will discuss in detail this likely pipeline later in this study.

4- Extending a pipeline from Israel to Turkey through Cyprus, using Turkey’s huge pipeline system and its geographical location near Europe to facilitate gas access to European markets or to Turkey itself, a major importer of natural gas. This option is considered the cheapest among all options from an economic perspective, as Israel will only need to build pipelines to Cyprus, and from Cyprus to Turkey, and it will rely on Turkey’s pipeline network and the Turkish gas transportation experience. However, there are several other considerations that may reduce the feasibility of this option for Israel and limits the chances of being chosen as a favorable route. It is difficult to imagine this option in light of the Turkish-Cypriot crisis. Meanwhile, the Turkish-Israeli relations do not seem to encourage such option, especially that Turkish-Israeli relations have deteriorated sharply in recent years (figure 5).

[Figure 5: A map showing the likely routes for the export of Israeli gas]

In view of the options available for the export of Israeli gas, it is clear that most of them have challenges and obstacles to economic, political and security considerations, but there is another option that offers Israel a better chance than the previous ones, namely to transport gas via a pipeline from Israel to Egypt – as the pipeline owned by Eastern Mediterranean Gas (extending from El Arish to Ashkelon) is already existing and can be used after carrying out some minor technical modifications. Through this option the gas flowing from Israel to Egypt can either feed the Egyptian market that has an escalating demand on natural gas or it can be exported to foreign markets as LNG after being liquefied in the gas liquefaction plants in Damietta and Edco. This option will spare Israel the cost of constructing liquefaction plants on its territory or the cost of constructing new pipelines that would extend from Israel to Cyprus, Turkey or the Greek Crete Island. Israel would only have to export gas via a pipeline that already exists, which will achieve the largest economic return of the natural gas extracted from the Tamar and Leviathan fields, in addition to achieving[31] strategic and political objectives that have not been realized through the 1979 peace treaty between Egypt and Israel. Commenting on this, Israeli Prime Minister Benjamin Netanyahu welcomed the “historic agreement” (the gas deal) between Egypt and Israel, pointing out that it was a joyous day[32] for Israel when this deal was signed. This simply sums up the size of strategic and economic dimensions that Israel has achieved through concluding the gas deal with Egypt.

Preference of the Egyptian option was not far from Israeli decision-making circles or specialized think tanks that referred to the option of transferring Israeli gas to Egypt as a strategic option for Israel. A classified report[33] by the Israeli Foreign Ministry’s Political Studies Unit stressed that Egypt is the best option for the export of Israeli natural gas compared to Turkey and Greece politically, economically, and strategically. In the same direction, the European Parliament stressed in a report[34] published in May 2017 that the best option for the export of Israeli gas is through the Egyptian LNG facilities. The report considered the Egyptian option as the most logical and realistic export scheme of Israeli natural gas compared to other options that are hampered by political crises on the one hand and the high economic cost on the other.

How the deal was made

Although the option of exporting Israeli gas via Egypt was considered the best option for Israel, it faced two main challenges during the time that followed the start of the Tamar field production in 2013. The first challenge was the occurrence of sharp political changes in the Egyptian regime after the January revolution, resulting in the emergence of an elected political leadership; and it was difficult for Israel to reach an agreement or a deal with the elected government on the transfer of natural gas from Israel to Egypt, especially that Israel had moved towards international arbitration[35] to demand substantial compensations after suspension of the export of Egyptian gas to Israel in 2012. On the other hand, this coincided with an Egyptian debate on the Mubarak regime’s deal of natural gas export to Israel after the January revolution, where senior former officials were accused of corruption for exporting Egyptian gas to Israel at prices lower than international prices[36]. Egyptian gas was then sold to Israel for $ 2 to $ 3 per 1,000 cubic feet, less than the gas prices paid by Egyptian companies at the time, $ 4 per 1,000 cubic feet, and much lower than gas prices in Europe and Asia. This issue was another challenge facing Israel’s desire of Israel to conclude any gas deals with Egypt at that critical time.

With the 3rd July coup d’etat in Egypt and the change of the political system in Egypt, the relations between Egypt and Israel have developed considerably and there was understanding between the two sides more than ever before, most notably the security cooperation and coordination in Sinai and the political consensus regarding the so-called ‘deal of the century’. This positive development revived the hopes of Israeli side in seeking to export its natural gas to Egypt and to achieve the best option for solving the crisis of exporting Israeli natural gas surplus.

The talk about a deal allowing Israel to export natural gas to Egypt was as early[37] as November 2014 when Israel sought to sell its Leviathan field output to Cairo. However, the political system that came after the coup d’état of 3 July 2013 looked concerned about gas deals with Israel, especially that the scandal of exporting gas to Israel during the Mubarak era – where prominent former officials were involved – was still fresh in mind. In addition, in such deals there is need to obtain parliamentary approvals to conclude, in anticipation of any legal claims to halt[38] import of Israeli gas, such as those that demanded suspension of exporting Egyptian gas to Israel in 2008 (In this context, a Cairo court on Dec. 1st 2008 overruled an Egyptian government’s decision to allow exports of natural gas to Israel saying that the constitution gave parliament the right to decide on sales of natural resources). These concerns led the Egyptian regime to move to make gas deals with Israel through private companies and to refrain from participating in these deals directly.

The government decided in August 2017 to pass legislation allowing private companies to import natural gas in the so-called Gas Market Law[39], as Egyptian legislation banned this in the past.

It is noteworthy that on February 19 2018, only five days after issuance of the Gas Market Law’s executive regulations[40] on February 14, 2018 – allowing private sector companies to import natural gas, a deal[41] was concluded between Egypt’s Dolphinus Holdings Ltd. (private sector) and the Israeli side – on importing Israeli gas from Tamar and Leviathan fields, which reflects clearly the preparations and arrangements made to pave the way for holding the Egyptian-Israeli gas deal. Under the deal, Israeli Delek Drilling-LP and US Noble Energy Inc., the co-partners of Tamar and Leviathan fields, 64 billion cubic meters of natural gas worth $ 15 billion will be exported to Egypt over 10 years.

The huge Egyptian-Israeli gas deal appeared to be a deal between the Israeli side and an Egyptian private sector company, as Dolphinus Holdings Ltd was the party that signed the deal with the Israeli side. However, a set of documents[42] indicate that the Egyptian General Intelligence Service is a partner with Dolphinus Holdings Ltd, which means that the company only acted as an intermediary on behalf of the Egyptian government in the gas deal with Israel. While the Egyptian government confirmed through several statements[43] that the deal belongs to the private sector according to regulations organizing gas market activities, Israeli officials[44] clearly declared that a historic deal was concluded between the Israeli and Egyptian governments.

Looking for a route

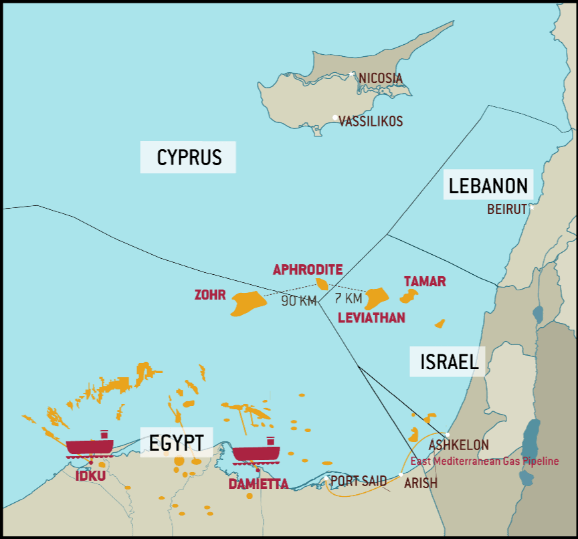

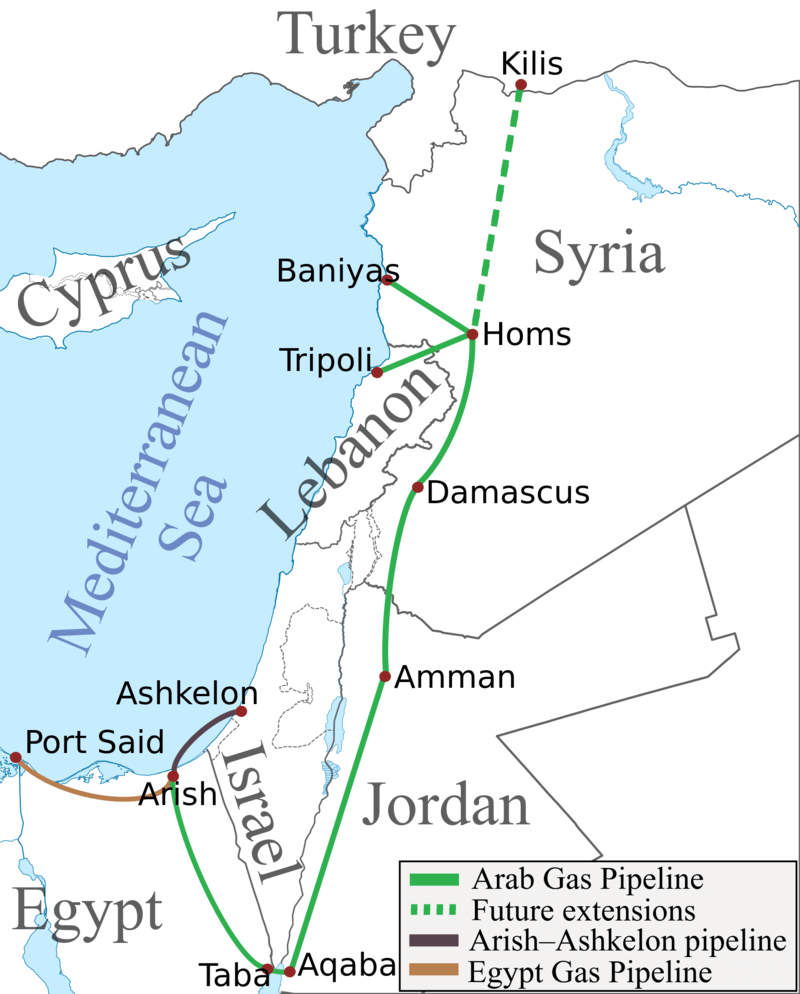

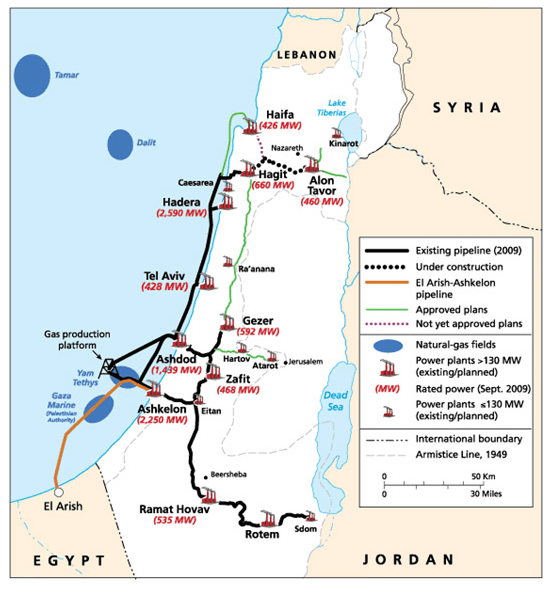

During the signing of the gas deal between Egypt and Israel, it was not announced how Israeli gas would be transferred to the Egyptian liquefaction platforms. Although there were no clear answers or assurances in this regard, it was obvious that the gas pipeline extending from the Egyptian city of El Arish to Ashdod port (Ashkelon) and owned by the East Mediterranean Gas company in the transfer of gas from Israel to El Arish and then to the Egyptian liquefaction platforms (Figure 6), especially that the Arish-Ashkelon pipeline is the same pipeline that was used in exporting natural gas from Egypt to Israel according to the agreement signed by the Egyptian government[45] in 2005. This pipeline has ceased its activity since 2011 because of the multiple blasts that hit it, up to 15 times[46] in the period following January 2011 until mid-2012, which prompted Egypt to halt natural gas supplies to Israel and then to terminate the deal completely and cancel[47] the contract in 2012. (Figure 6)

[Figure 6: A map showing the location of the Arish-Ashkelon pipeline.]

Determining the route of the transfer of Israeli gas to Egypt is directly reflected in determining the real gains that Israel will get from the deal, since the different routes that the Israeli gas can take necessitate construction of new pipelines and thus affect the expected Israeli gains from the deal. Accordingly, the use of the old pipeline between Al-Arish and Ashkelon provides the faster less expensive solution despite the security challenges facing it because of passing through the city of El Arish in North Sinai, which is still witnessing military operations.

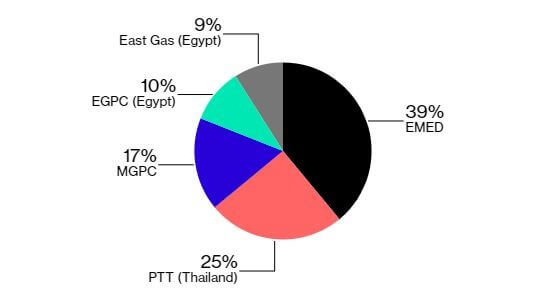

Several months after the Israeli-Egyptian gas deal, two companies, Israeli Delek Drilling-LP and US Noble Energy Inc., as well as East Gas Company [a subsidiary of the Egyptian Natural Gas Holding Company (EGAS)] announced that they have acquired[48] the largest share of the East Mediterranean Gas Company (EMG), owner and operator of the Arish–Ashkelon pipeline, by up to 39%, that allows them to dominate the pipeline compared to other partners (25% owned by Thai PTT, 17% owned by MGPC of Ali Evsen, a Turkish businessman, 10% for Egyptian General Petroleum Corporation, and 9% owned by East Gas Company). This makes transference of Israeli gas to Egypt via the Arish-Ashkelon pipeline the most likely prospect in the near future (Figure 7).

[Figure 7: showing the shares of partners in the Arish-Ashkelon pipeline.]

Where will the gas coming from Israel go?

Short-term self-sufficiency

A key question about the route of natural gas coming from Israel remains unanswered, despite the repeated talk about the Israeli-Egyptian gas deal and its details as well as Egyptian gas reserves and the possibility of achieving self-sufficiency of natural gas and becoming a platform for the export of gas abroad:

Will the Israeli gas be liquefied and re-exported abroad?

Will the Israeli gas be directed to the Egyptian domestic market to meet Egyptians’ needs? or Will it be exported directly to another destination?

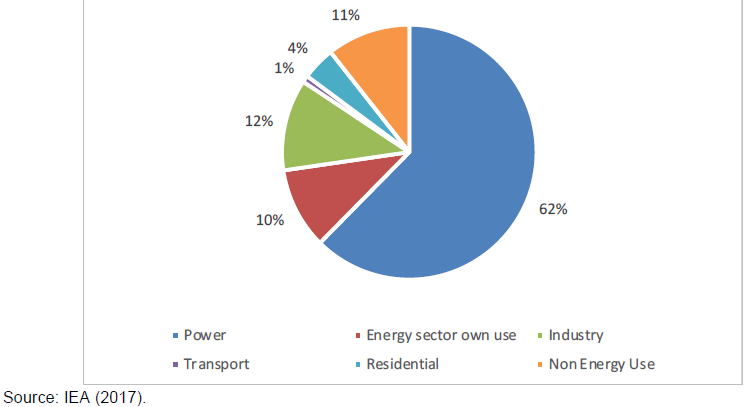

The Egyptian Petroleum Minister announced in September 2018 that Egypt had achieved self-sufficiency of gas after the rise in the Zohr Field output and added that Egypt is on the way to export the natural gas surplus in January 2019. However, despite the Egyptian Petroleum Minister’s announcement that Egypt reached self-sufficiency[49] and will export [50] the surplus, albeit in limited quantities, the possibility of filling the domestic consumption gap in the near future remains questionable. The rising energy consumption associated with the continued growth of population in the coming years does not indicate that Egypt will be able to export natural gas or even to meet its domestic consumption needs. Egypt relies mainly on natural gas in electricity production, consuming about 62% of Egypt’s total natural gas consumption rate in 2016 (Figure 8).

[Figure 8: showing natural gas consumption rates in Egypt’s different sectors.]

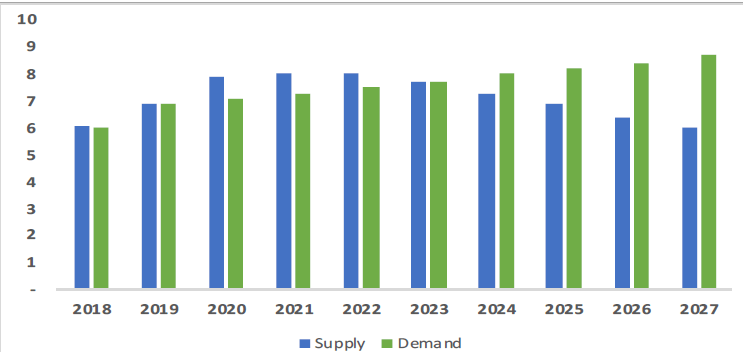

In this regard, we should refer here to a study published by the Oxford Institute[51] for Energy Studies in June 2018, which concluded that “Egypt will return to a balanced gas market but not for long”. According to the study, despite such balance could be achieved by 2020, however this will not continue for a long time since demand for natural gas in Egypt will continue to grow at a slower rate than the rates of the past two decades. Accordingly, the export window is unlikely to continue for more than a few years and then export levels will fall rapidly (Figure 9).

Scenario (1)

Scenario (2)

[Figure 9: Comparison of the forecast of natural gas production and consumption rates in Egypt over the next ten years (2018-2027).]

Scenario 1 above is based on the total gas production from the producing fields and the newly discovered fields. Scenario 2 is based on adding the expected discoveries (between 1 and 1.5 billion cubic feet per day) to the total production (Mostefa 2018).

Another study by CI Capital on the future of natural gas in Egypt also predicts that Egypt will return to importing natural gas within a few years, as the natural gas self-sufficiency will not last for long. (N.B. We have not been able to obtain a copy of the report but we have relied here on the published narrative on the Mada Masr[52] website.) However, the figures announced by the Ministry of Petroleum give the same conclusion, as the volume[53] of domestic consumption in the fiscal year 2020/2021 is expected to reach 9 billion cubic feet per day, while Egypt’s maximum production is expected to reach 7.3 billion cubic feet per day at the end of 2019 after the Zohr Field reaches its maximum production capacity. There is a clear difference between the expected consumption and production rates in the future, bearing in mind that production rates are likely to decline naturally as a result of the decline in the production of gas fields over time, unless there are new discoveries with huge natural gas reserves.

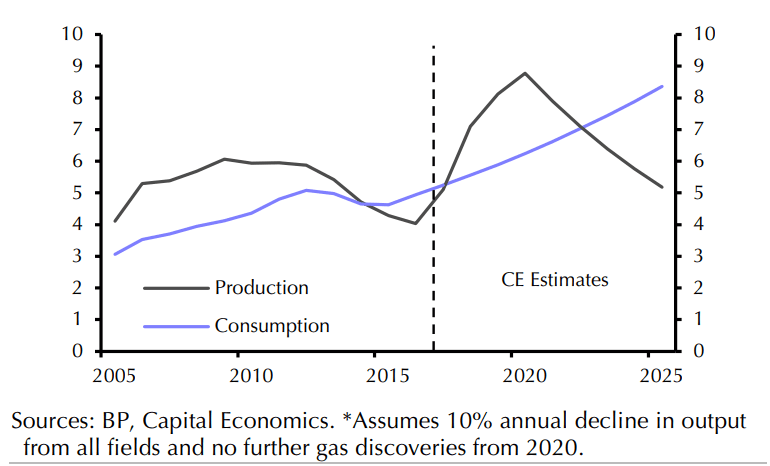

Another report by Capital Economics[54] states that Egypt[55] can return as a net importer of natural gas in five years only as a result of the rapid population growth. This means that at the beginning of the new decade, Egypt will seek meeting its natural gas needs by importing from abroad ( Figure 10), another assessment[56] of Egypt’s gas reserves conducted by Consultants McKinsey & Co. refers to the same results and states that there will be an Egyptian need for the Israeli gas to meet its natural gas needs of domestic consumption in the near future.

[Figure 10: showing the natural gas production and consumption rates in Egypt until 2025.]

So, it is not expected that Egypt will be able to achieve self-sufficiency of natural gas in the medium term. Moreover, it will need to adopt policies to develop alternative sources of energy other than the natural gas for the purposes of electricity generation. However, these are long-term solutions, as they will take a long time to achieve permanent self-sufficiency of natural gas. In the light of the reports, studies and available data, the possibility that the natural gas flowing from Israel will go to the local Egyptian market to meet its needs in the coming years seems closer to reality. However, the natural gas coming from Israel may also be exported to international markets after being liquefied besides meeting the Egyptian domestic consumption during the coming few years at best – before it will be confined to the domestic consumption only early next decade.

Export to European markets

The other possibility is that the natural gas coming from Israel will take a path to the European markets and accordingly Egypt could become a competitor to the main gas exporters to the European continent. However, there are obstacles that could make this possibility unlikely: The first obstacle is apparently the inability of the gas coming from Israel to compete with natural gas prices in European markets where it will be difficult to imagine that the gas coming from Israel through a pipeline to Egypt, liquefied in the Egyptian liquefaction plants, transported in tankers to the European coasts, and finally deliquefied again, can compete with cheap Russian gas flowing into Europe through a pipeline network that has been existing for decades.

In addition to the high cost of natural gas coming from Israel to Egypt and then re-exported to the European consumer, there is another factor that further complicates the matter and makes it difficult for this gas to compete in the European market, despite the European search for an alternative for the Russian gas, namely the high price of the natural gas that Egypt contracted to import from Israel. Despite the high prices of gas in Europe, a CI Capital report[57] points to the high price of Egypt’s gas imports from Israel compared to the prices of natural gas sold in European markets, making it more difficult to compete with the countries that export cheaper gas to the old continent.

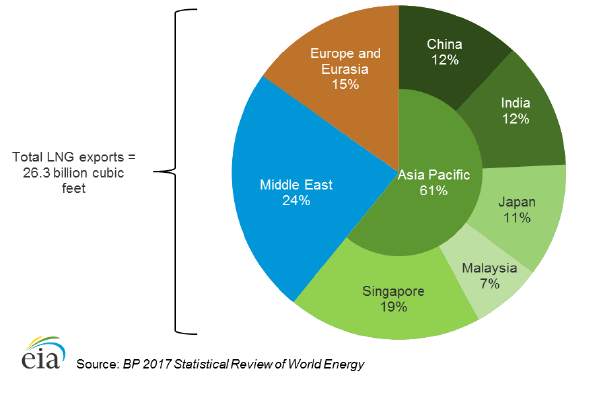

Also, the rates of Egyptian liquefied natural gas (LNG) exports[58] in 2016 indicates that it is difficult for the Egyptian LNG to compete with the gas prices in European markets. These rates indicate that there is a limited volume of Egyptian LNG exports to European markets compared to the Egyptian LNG exports to the Asian markets. While Egypt’s LNG exports to the Asia and the Middle East represent 85% its exports to European markets represent only 15% (Figure 11).

[Figure 11: showing export rates of Egyptian liquefied gas to Asia, Europe, and the Middle East in 2016.]

There is another long-term obstacle hindering the arrival of Egyptian LNG exports to European markets, namely the European strategy to replace oil and gas with renewable energy which will limit the amount of natural gas flowing into European markets in the long run, making competition among natural gas exporters more difficult at the international level. It seems clear that the obstacles and difficulties we have referred to here will make it very difficult for Egypt to re-export Israeli gas to European markets.

Will the gas coming from Israel go to Saudi Arabia?

In December 2017, less than two months before the announcement of the gas deal between Egypt and Israel, Saudi Energy Minister Khalid al-Falih told[59] reporters that Aramco was more interested in importing natural gas from areas closer to the kingdom, such as the Mediterranean Sea and East Africa. It appears from the statements of the Saudi minister that within the framework of the Kingdom’s quest to replace oil as a power generating fuel with the natural gas during the coming years and may pay more attention to the natural gas coming from the eastern Mediterranean, especially as it is geographically close to the Kingdom, which means that its cost will be limited compared to the gas coming from other parts of the world.

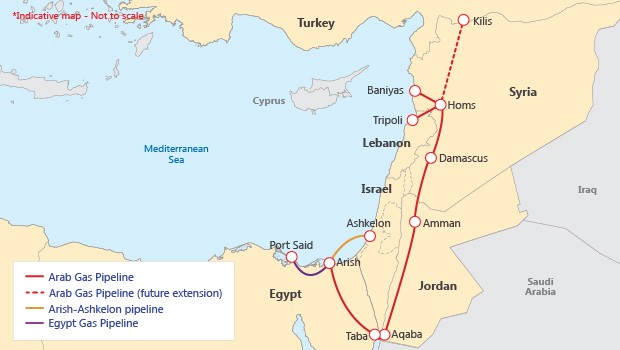

Accordingly, it is logical to conclude that natural gas coming from Israel may take another path in addition to the Egyptian domestic market and European markets by heading to Saudi Arabia. It does not seem that this possibility is far from reality where the relations between the three parties: Egypt, Saudi Arabia, and Israel appear in their best conditions and perhaps better than ever before, taking into consideration that the gas pipeline linking Egypt, Jordan, Syria and Lebanon (Fig. 12), known as the pan-Arab Gas Pipeline (AGP) that was used to transport gas from Egypt to Jordan and Israel until it was suspended after canceling[60] the contract to export natural gas from Egypt to Israel in 2012, is close to the Saudi border as it passes through southern Jordan, making it possible to use this pipeline and extend it in the future to the Kingdom of Saudi Arabia as it does not require a heavy cost .

[Figure 12: A map showing the location of the Arab Gas Pipeline]

It is important to note here that by the end of 2019, a 65 km pipeline linking Israel and Jordan will be completed[61], which can contribute to making it easier to transport gas from Israel via Jordan to Saudi Arabia (Figure 13). In this context, the comments of Israeli Delek Drilling CEO, which refer[62] to the possibility of exporting Israeli gas to Egypt through Israel’s internal network and then to the pan-Arab Gas Pipeline in the first stages of export due to technical problems in the Arish-Ashkelon pipeline. On the other hand, the possibility of liquefying Israeli gas in Egyptian liquefaction platforms and then transferring it to Saudi Arabia remains a likely option. Simon Henderson, an energy researcher at the Washington Institute for Near East Policy, clearly refers to the possibility of transferring Israeli gas to Saudi Arabia via Egypt’s liquefied natural gas platforms in a report[63] published In December 2017. “… perhaps one day Israeli gas could end up in Saudi Arabia via an Egyptian LNG plant,” Henderson suggested in his report.

[Figure 13: A map[64] showing Israel’s internal gas pipeline network]

Who will win the race for European markets?

The huge natural gas reserves of Egypt, Israel and Cyprus have stimulated their aspiration to export natural gas to the voracious European markets, which can generate major economic benefits for them. The quest for European markets has not been limited to the Eastern Mediterranean countries that produce natural gas, but it extended to other regional countries that seek to compete for the transfer of gas to Europe through pipelines passing through their territory and achieve influence within Europe as well as the economic gains. Greece and Italy entered the arena of competition on European markets in addition to Turkey, which played the biggest role in the past decades in the transfer of gas from Russia to Europe through pipelines passing through its territory (Blue Stream pipeline transfers Russian gas to Turkey, as well as the Turkish Stream pipeline, which will also contribute to the transfer of Russian gas to Turkey and then to Europe by 2019). Amid this hectic competition, the answer to the question about the ability of Israeli gas coming into Egypt to compete with other gas exporters in European markets will be an important factor in determining the real gains that could accrue to Egypt from the import of Israeli gas.

Europe and the search for an alternative to Russian gas

The European pursuit to diversify energy and natural gas sources has increased significantly after the chronic relation crisis with Russia as a result of Russian intervention in Ukraine and its occupation of the Crimea peninsula in 2014. It is noteworthy here that about one third[65] of gas imports flowing to Europe come only from Russia (Figure 14), which makes the European Union recommendations that are aimed at seeking gas exporters other than Russia understandable, especially under the European sanctions on Russia which exacerbated the crisis between the two sides. Meanwhile, the emergence of huge reserves of natural gas in the eastern Mediterranean that is geographically close to Europe represented a worthy investment opportunity for Europe and a new path that can be relied upon heavily in the future to ensure diversification of sources of gas[66] coming to Europe. Also, this may have pushed Europe to provide support for energy projects aimed at bringing gas from the Eastern Mediterranean to the old continent or to support establishment of a new energy corridor to Europe.

[Figure 14: showing the size of European reliance on Russian gas]

East Mediterranean – arena of partnerships and disputes

The massive gas reserves of Eastern Mediterranean amid the European need of this gas fed up existing regional conflicts and led to new conflicts; and at the same time acted as important drivers for ending or calming down some other regional conflicts through engagement in more partnerships and cooperation. This situation made the Mediterranean a platform for partnerships and conflicts where incentives and barriers[67] are equal. It seems clear that there is a new map alliances and conflicts in the Eastern Mediterranean, some are old and others are new.

Natural gas reserves lead to many possibilities in the relations between the Eastern Mediterranean countries. Partnerships in the field of gas may lead to further cooperation[68] in the direction of changing the strategic policies of regional countries and the pacification of existing conflicts. On the other hand, competition on the possession and export of natural may lead to creation of new regional tensions[69], and relations remain limited to cooperation with respect to the natural gas file in light of political difficulties[70], as is the case with the continued flow of Russian gas to Europe in the wake of the Ukrainian crisis.

The current tripartite alliance between Egypt, Greece, and Cyprus comes within the framework of the establishment of an “Eastern Mediterranean” alliance for coordination and cooperation with respect to the exploration of natural gas in the Mediterranean waters and achievement of economically feasible projects related to the utilization of natural gas reserves, whether through mutual deals or through the extension of gas pipelines or the use of LNG platforms. In this regard, the tripartite alliance resulted in an agreement[71] between Egypt and Cyprus that allows the latter to benefit from the LNG infrastructure in Egypt through the construction of a gas pipeline connecting Cyprus’ Aphrodite field to the liquefaction plants on the Egyptian coasts. At the same time, Israeli understandings and deals with Egypt and Cyprus indicate the volume of cooperation between the three parties regarding natural gas in the eastern Mediterranean. Israel contributed mainly to the development and discovery of gas fields in Cyprus, where Cyprus announced the discovery of the Aphrodite natural gas field in 2011 through the US Noble Energy Inc., which operates mainly in Israel. The first form of official cooperation between Cyprus and Israel started when Israeli Delek Drilling-LP became a key partner in the development of the Aphrodite gas field.

On the other hand, one of the most prominent disputes arising from the possibility of discovery of more gas reserves in the Eastern Mediterranean region in the future are those related to the delineation of e90lusive economic zones (EEZ) between more than one party, where the huge gas reserves in the region doubled the complexities of related to the EEZ agreements, especially the unilateral prospection and exploration moves by regional countries have never stopped.

One of the most prominent disputes over the delineation of e90lusive economic zones in the Eastern Mediterranean region is the conflict between Turkey and Cyprus, an extension of the historic conflict between the two sides. Although the emerging natural gas investments in the Eastern Mediterranean could push for a new reformulation of Turkey-Cyprus strategic relations, yet it seems that there is no expected political settlement between the two sides in the near future, where Cyprus in early 2012 tended to announce[72] a global auction (Licensing Round Offshore) for the prospection, exploration, and production of hydrocarbons in the disputed waters with the Turkish side (Figure 15), in order to support the exploration activities politically, which pushed Turkey to intervene more than once to prevent exploration vessels from searching for natural gas in the disputed area between the two sides. The last of these incidents was in February 2018 when Turkey intercepted[73] one of the exploration vessels belonging to Eni Italian destined for exploration in the disputed waters. Several months after the incident, Turkey launched in October 2018 a drilling vessel called “Fatih[74]” to start drilling in the waters near the disputed area.

[Figure 15: A map showing the disputed e90lusive disputed zones[75] between Turkey and Cyprus]

While demarcation of e90lusive economic zones in the eastern Mediterranean should depend on the creation of consensuses and understandings among the countries of the region without e90lusion of any party that can cause new conflicts or revive old ones due to the overlapping and interconnections of e90lusive economic zones between the countries of the region. The Egyptian regime tended after its ties with Turkey strained after the July 3 coup to hold talks with Cyprus and Greece to demarcate their maritime borders and identify the e90lusive economic zones. Egypt and Cyprus signed an agreement[76] in late 2013 to determine their EEZ; and the talks[77] between Egypt and Greece are still ongoing in this regard. This represented a new dimension in the strained relationship between Turkey on the one hand, and Egypt, Greece, and Cyprus on the other. The crisis between the four countries did not only reflect on mutual statements between the two parties, but with the challenges of potential conflicts it also extended to the security and military dimensions[78]. It has appeared clearly that the eastern Mediterranean countries tended to enhance their armament and training targeting the protection of their naval installations through development of their military capabilities and training to perform tasks primarily related to securing their interests in the field of naval energy.

Israel was not far from the disputes over the e90lusive economic zones, despite its understandings with Egypt and Cyprus on the determination of their EEZ, but these understandings did not include Lebanon. The Lebanese exploration contracts that were signed with international companies amid likely natural gas discoveries offshore led to the outbreak of a crisis[79] between Lebanon and Israel on the identification of e90lusive economic zones between the two sides in what is known as the crisis of “Block 9”. Despite international mediation[80] efforts between the two sides, yet there seems to be no horizon for resolving this dispute, especially that the political position of Hezbollah has been strengthened after the general elections that were held in Lebanon in May 2018, which makes access to solutions between the two sides more difficult than ever.

On the other hand, the Palestinian Authority decided in July 2017 to form a national team[81] to begin “demarcation of the maritime borders of Palestine”. The PA’s motives behind this step are not yet clear as well as the actual steps taken by the Palestinian Authority to control the maritime borders under the Israeli occupation. According to the Oslo Accords, the maritime border of the Palestinian Authority is Gaza’s maritime area off its coastline overlooking the Mediterranean Sea. However, Gaza is now under the control of Hamas; and amid the existing division between the PA and Hamas, neither Israel nor the Palestinian Authority is likely to allow[82] development of any gas discoveries off the coast of Gaza that could contribute to improving the Gaza Strip conditions as long as it is under the control of Hamas.

To sum up, the successive huge gas discoveries in the Eastern Mediterranean region indicate that energy conflicts will have a significant impact on the policies and relations of regional countries. In fact, it is difficult to reach a multilateral agreement between the Eastern Mediterranean countries for identifying the e90lusive economic zones amid the turbulent regional situation and the bilateral disputes between the Eastern Mediterranean countries, which led them to sign different bilateral agreements separately.

The long-term Israeli trap

Israel understands that it will make the most benefit of the natural gas flowing from its discovered fields by exporting it to Egypt; but at the same time it has not given up its desire to become a platform for the export of gas to Europe even in the long term. On 5 December 2017, Greece, Cyprus, Italy and Israel signed a memorandum of understanding[83] for constructing a 2100 km-long gas pipeline from the Eastern Mediterranean region to Greece and Italy at a cost of between $ 7 billion and $ 8 billion. This underwater pipeline will allow the transportation of the Cypriot and Israeli gas reserves to mainland Europe through Greece and Italy. Although the project faces technical difficulties[84] due to the difficulty of extending gas pipelines deep waters as well as other difficulties related to the high cost and economic feasibility, the persistent Israeli efforts towards the construction of the pipeline and become a platform for the export of gas to Europe has never ceased. Late November, 2018, local Israeli media reports[85] referred to “closing a deal” between the four countries for the construction of the gas pipeline to Europe, adding that the contract[86] will be officially signed in February 2019. It is noteworthy that this proposed pipeline has drawn the attention of the European Union[87] which agreed in November 2018 to invest $100 million in a feasibility study for the construction of the longest and deepest underwater gas pipeline in the world.

Israel is serious about setting up the new pipeline to achieve the most benefit of its gas reserves and become a natural gas hub in the Eastern Mediterranean, not any other country, no matter how strategic relations seem to be between them. Through construction of this pipeline, Israel does not only seek achievement of economic gains, but it seeks achievement of political goals as well, as Israeli gas flowing into Europe will contribute to reducing Arab influence in Europe resultant from the domination of Arab oil and gas exports over European markets, and increasing Israeli influence[88] at the same time. On the other hand, the Israeli gas pipeline will cause expected economic losses on Egypt due to the negative impact of the pipeline on Egypt’s positioning as a platform for the export of natural gas to Europe, taking into consideration that the new pipeline will transport natural gas directly to European markets at a lower cost than the gas coming from Egypt which needs to be liquefied before being exported in tankers to the European markets and then deliquefied again.

Israeli strategy in the export of gas

We cannot make an assessment of the gas deal between Egypt and Israel through the economic dimension and potential gains and losses only without addressing the strategic and security dimension which is basically a key dimension in the assessment and study of relations between Egypt and Israel.

Israel’s natural gas export strategy is a model that can be scrutinized to see how natural gas can be a strategic tool to impose greater influence in the region. It is important to refer in this context to the natural gas export policy approved by the Israeli government[89] in 2013 after the discovery of the Tamar and Leviathan fields. This policy obligates Israel to devote 60% of its natural gas reserves to domestic consumption, to achieve self-sufficiency of natural gas by 2040. Through this policy, Israel seeks to consolidate its strategy of the export of natural gas and at the same time target achievement of self-sufficiency in the long-term, which allows Israel to become one of the major natural gas exporters in the region, impose its influence, and possibly reach understandings and settlements of old conflicts that traditional political solutions have failed to achieve. The Israeli strategy seems very clear. Although Tel Aviv is interested in the economic returns from the export of natural gas, yet it is keen on avoiding any threats to its natural gas self-sufficiency target; Israel does not want to be in a position that makes it dependent on the natural gas flowing from the neighboring countries, which could give its neighbors an opportunity to acquire pressure cards against it in the long-term. Israel’s priority is all that concerns national its security, while the economic dimension and the gains that can be achieved always come next.

In the same context, a study[90] conducted by the Institute for National Security Studies in Israel in March 2018 concluded that the agreement to export gas to Egypt will have a great strategic value for Israel not only in granting Israel an opportunity to become one of the gas export platforms to Europe, but also to achieve its strategic ends on the long-term. “These agreements stabilize Israel’s relations with its neighbors by creating a web of mutual interests and opening up the possibility of regional cooperation beyond the subject of natural gas, such as the export and import of electricity and desalinated water,” the NSSI study stated. Israel is aware that such agreements can transcend political obstacles to establishing long-term relations with a heavy-weight country such as Egypt and imposing a reality based on common economic interests and at the same time maintaining its strategic interests.

Potential threats to national security

On the other hand, it is not unlikely that Egypt’s dependence on Israeli gas does not threaten Egyptian national security. We should refer here to several main considerations that could pose a threat to Egyptian national security as a direct result of Cairo’s gas deal with Tel Aviv, including:

First, reliance on Israeli gas gives Israel an opportunity in times of crisis, whether with Egypt or with other regional parties, as it can be used to blackmail Cairo and influence its political decision by threatening to cut off natural gas supplies and accordingly shut down major plants in Cairo and Alexandria. This issue gives Israel decisive influence in its relations with Egypt, especially as the Israeli gas will be the lifeline of Egypt where it is likely to meet the needs of the Egyptian domestic market in the coming years, taking into account that Egypt relies heavily on natural gas in generating and producing electricity.

Second, according to this deal, Egyptian security is directly linked to Israel’s security, and accordingly any security threats that could harm Israel’s ability to produce gas would also pose a direct threat to the Israeli gas supplies to Egypt. Thus, Israeli security is not only related to Israel’s interests, it has also become related to the security and interests of Egypt, which will stimulate Egypt’s foreign policy towards crises faced by Israel, whether with Gaza, with South Lebanon, or with any other regional parties, to adopt pro-Israeli positions in order to maintain the flow of Israeli gas to Egypt.

Third, the gas coming from Israel is always subject to security threats, whether it is transported through the Arish-Ashkelon pipeline or the Arab Gas Pipeline. The situation in Gaza and the prospects of the outbreak of war remain likely. On the other hand, the Arish-Ashkelon pipeline of and the Arab Gas Pipeline meet in El Arish city, North Sinai, where there are still confrontations between the Egyptian army and armed groups, which seem unlikely to end in the near term. These security conditions make Egyptian imports of Israeli natural gas unstable[91] and unreliable for a vital sector such as the energy sector in Egypt.

Controversy over economic gains

The economic dimension appeared to be the most aspect that the Egyptian government discussed during talk about the Israeli gas deal. The government has calculated the economic gains of the deal without providing a medium- or a long-term assessment of the deal. While the size of the actual gains of the Israeli gas deal is still unknown, there is still controversy about the feasibility of the deal, and its expected gains. There is real suspicions about Egypt’s ability to achieve self-sufficiency of natural gas in the coming years, which means that Egypt will return to meeting its needs of gas through importing from abroad, depending on the Israeli gas deal. Egypt’s ability to achieve natural gas self-sufficiency in the future is not the only obstacle to Egypt’s opportunities of exporting Israeli gas to Europe, where there is another obstacle that is not less difficult than self-sufficiency, namely its inability to compete with other gas exporters in European markets.

It is noteworthy that the Egyptian government has not mentioned whether it conducted a study of the European market to explore consumers’ demand on gas, ensure that the gas coming from Israel to Egyptian liquefaction plants and re-exported to Europe will fall within the framework of European consumer’s demand, and whether it will be able to compete with the low prices of the gas coming from Russia, Norway or Algeria to European markets. Despite the huge reserves of natural gas in the eastern Mediterranean and despite the geographical proximity with Europe, the trade difficulties[92], and the difficult restrictions of agreement between governments in the international gas markets represent further obstacles on the ability of the Eastern Mediterranean countries to compete in European gas markets.

Import in return for dropping compensations

It is clear that one of the main reasons behind Egypt’s acceptance of the Israeli gas import deal relates to Israel’s waiver of the international arbitration lawsuits against Egypt. In 2015, the ICC ordered the Egyptian government to pay $ 1.7 billion in compensation to the Israel Electric Corporation (IEC) and $ 288 million in compensation for the East Mediterranean Gas Company (EMG), owner of the Arish-Ashkelon pipeline; and the gas deal with Israel appeared to be in the context of importing gas in return for waiving compensations. Immediately after announcing the gas deal, the Egyptian government continued to confirm[93] Israel’s waiver of compensations while there was a constant denial[94] from the Israeli side. However, after Israeli Delek Drilling-LP, US Noble Energy Inc., and Egyptian East Gas Company (a subsidiary of EGAS) announced that they have acquired the largest share of the East Mediterranean Gas Company (EMG), owner and operator of the Arish–Ashkelon pipeline, by up to 39%, talk started seriously about Israel’s waiver[95] of compensations, but there is still no clear information about this issue or even about how compensations will be waived.

Transportation and liquefaction fees are limited gains

Regardless of the dispute about the economic gains Egypt can make from the Israeli gas deal and the absence of precise calculations about the size of the expected gains, there are other gains that could be made from the gas deal, albeit limited: The process of transporting and liquefying gas is one of the gains that Egypt can get from the Israeli gas deal, but they are actually of limited value, since the collection of gas charges via the Arish-Ashkelon pipeline will be obtained by a number of partners, including Egypt. On the other hand, gains acquired by Egypt through liquefaction plants remain limited because Egypt owns[96] only 24% of the Edco plant and 20% of the Damietta plant.

Conclusion

We refer here to the main conclusions of the study as follows:

First, despite the huge gas reserves of the Zohr Field, it seems that it will be directed to domestic consumption only to achieve self-sufficiency, where its infrastructure is designed to feed the local gas network only. It is also noteworthy that the Egyptian government on 5 July 2015 doubled the prices of its gas purchase prices from Eni (under Eni’s share of extracted gas and Eni’s recovery of exploration and drilling costs), raising the price of one million British thermal unit (equivalent to 28.26 cubic meters) from $2.65 to a maximum $5.88 and a minimum of $4 – making the price of gas produced from the Zohr Field directed to domestic consumption close to the prices of gas imported from the world markets.

Second, the gas self-sufficiency achieved through the discovery of Zohr Field and a number of other discoveries will not last long unless there are new discoveries and huge natural gas reserves, according to several studies on energy indicating that Egypt will return to natural gas import to meet Egyptian domestic market needs early next decade, where self-sufficiency will end between 2021 and 2025 amid the high demand on gas compared to its production.

Third, despite the many options for Israel to export its natural gas, the gas deal with Egypt has been the best strategic, political, and economic option, as it would make huge economic gains for Israel and at the same time enable it to achieve strategic superiority in energy over a pivotal regional country such as Egypt through controlling part of the power supply to the Egyptian market.

Fourth, the gas coming from Israel will go to the domestic Egyptian market to meet its needs. It may also be exported abroad alongside its domestic consumption. We should take into account that there are challenges facing gas imported by Egypt from Israel to compete within the European markets, which makes Asian markets and perhaps Saudi Arabia – which are interested in replacing oil with natural gas in power generation – the closest option for exporting the gas coming from Israel. However, gas export is not expected to continue for a long time – perhaps for only a few years – before all gas coming from Israel is devoted to domestic consumption only.

Fifth, Israel apparently strives to become the main gas export platform in the Eastern Mediterranean region through its agreement to construct a pipeline for the export of Israeli and Cypriot gas to Europe via Greece and Italy, which is a real challenge to Egypt’s quest to become a regional gas hub in the Mediterranean. The Israeli quest to build such pipeline is not limited to the expected enormous economic gains only; in fact it aims at increasing Israeli influence within Europe and competing with Arab oil and gas exporters in this regard.

Sixth, Despite Israel’s huge natural gas reserves, its gas export strategy is based on achievement of national security. It gives priority to ensuring long-term self-sufficiency, even at the expense of significant immediate economic gains from the export of gas.

Seventh, Egypt’s Israeli gas imports go in the direction of building strategic relations between the two sides, which will have a direct impact on the orientations of Egyptian foreign policy towards its regional environment, which represents potential threats to Egyptian national security.

Eighth, we cannot assess the Israeli gas deal only in terms of its uncertain economic gains that Egypt could get without giving priority to its impact on Egypt’s national security. The Israeli gas deal gives Israel a real chance to exercise greater influence over Egypt; after the deal, Israel now possesses one of the strategic cards through which it can exert pressure on Egyptian politics in the region, which is perhaps the biggest gain for Israel in the context of its conflicts and historical crises in the Middle East.

Recommendations

First, the huge natural gas reserves in the Eastern Mediterranean region lead to joint cooperation and partnerships among the countries of the region, but at the same time they can serve as a catalyst for fueling geopolitical conflicts. However, such partnerships based on natural gas resources do not appear to be an alternative path to political settlement of existing historical conflicts in the region although it may contribute to the achievement of temporary stability[97]. Therefore, Egypt should strive hard to provide other alternatives to Israeli gas in order to ensure satisfying the growing needs of the domestic market and achieve required growth rates away from linking with Israel and its continued regional crises.

Second, the Liquefied Natural Gas (LNG) from both Algeria and Qatar can be one of the options that can be relied upon to meet the Egyptian domestic market needs of gas in the future. Another option for gas imports is Turkey, through which Russian gas can flow to Egypt, especially that the Arab Gas Pipeline connecting Egypt, Jordan, Syria, and Lebanon had been planned to extend its last phase from Syria to Turkey, but stopped because of the events that accompanied the Arab Spring. In case of extending this pipeline to Turkey, it will allow the flow of Russian gas to the four Arab countries, including Egypt, via Turkey.

Third, The formulation of energy policies that ensure reducing Egypt’s heavy dependence on natural gas in the production of electric power and push towards the development of alternative[98] for the natural gas in power generation will contribute to reducing the total demand for natural gas in Egypt – which will at the same time save quantities of natural gas supplies for the benefit of gas-intensive heavy industries.

[2] Moses Aremu, Low Cost, Sweet Crude, Abundant Gas, Nearby Markets Put Saharan Africa in the Reckoning, Oil and gas online, April 6, 2000.

[3] Marco Alfieri, Nessun Dorma, eniday, October 27, 2015.

[4] Egypt gas bid round to include area abandoned by Shell, Reuters, November 15, 2011.

[5] القابضة للغازات تطرح 15 منطقة جديدة للبحث عن الغاز.. وتقدر الاحتياطي بـ«تريليون» قدم، المصري اليوم، 29 يناير 2012.

[6] Bid round 2012, Egyptian natural gas holding company, June 4, 2012.

[7] 13 شركة عالمية تفوز فى مناقصة التنقيب عن البترول والغاز بـ”المتوسط”.. و1.2 مليار دولار استثمارات متوقعة، صدى البلد، 16 ابريل 2013

[8] Block 9 Shorouk offshore, Egyptian natural gas holding company, June 4, 2012.

[9] Marco Alfieri, Nessun Dorma, eniday, October 27, 2015.

[10] مصر تعلن اكتشاف أكبر حقل غاز بالمتوسط، سكاي نيوز عربية، 30 اغسطس 2015.

[11] مصر ترفع سعر شراء الغاز من إيني وإديسون الإيطاليتين أكثر من 100%، رويترز، 5 يوليو 2015.

[12] Natural Gas Prices Forecast: Long Term 2018 to 2030, COMESA , November 2, 2018.

[13] Inauguration of Zohr Gas Field Project at Port Said, Ministry of Petroleum, January 31, 2018.

[14] عمرو عادلي، إدارة ملف الطاقة في مصر بين الفساد وعدم الكفاءة، مركز كارنيجي للشرق الأوسط، 11 مايو 2015.

[15] Jared Malsin, In Egypt’s Vision of Energy Independence, Egyptians Pay More, The Wall Street Journal, August 27, 2018

[16] Michael Ratner, Natural Gas Discoveries in the Eastern Mediterranean, Congressional Research Service , August 15, 2016

[17] Egypt to up gas production by 2019, LNG world news, May 23, 2016.

[18] Eni begins producing from Zohr, the largest ever discovery of gas in the Mediterranean Sea, Eni.com, December 20, 2017.

[19] Zohr Ramp-up: Eni reaches 2 bcfd production target, Eni.com, September 8, 2018.

[20] Egypt’s Natural Gas Output Rises to 6.6 Bcf Per Day, GAS.com, September 18, 2018.

[21] مصر تعلن وقف استيراد الغاز المسال من الخارج، رويترز، 29 سبتمبر 2018.

[22] Zohr Ramp-up: Eni reaches 2 bcfd production target, Eni.com, September 8, 2018.

[23] Egypt’s Gas Consumption to Reach 9 bcf/d in 2020/21, Egypt Oil & Gas, September 24, 2018.

[24] Jordan and Egypt sign deal to renew flow of natural gas, The Jordan times, August 9, 2018.

[25] Egypt is optimistic about new gas discoveries in the Mediterranean, The Economist, July 5, 2018.

[26] Zohr brings turnaround in Egypt’s LNG fortunes, LNG World shipping, May 16, 2018.

[27] Israel Starts Tamar Gas Production, Bloomberg, March 31, 2013.

[28] Noble Pulls Anchor in GOM as U.S. Onshore, Mediterranean Natural Gas Take Priority, Natural gas intelligence, February 15, 2018.

[29] Greece, Cyprus, Italy, Israel sign MoU for East Med gas pipeline, New Europe, December 5, 2017.

[30] Agreement reached on Israel-Europe gas pipeline, Globes, November 25, 2018.

[31] وزير الطاقة الإسرائيلي يقول صفقة الغاز ستقوي العلاقات مع مصر، رويترز، 19 فبراير 2018.

[32] PM of Israel [IsraeliPM]. (February 19, 2018). I welcome the historic agreement that was announced on the export of Israeli gas to Egypt. This will put billions into the state treasury to benefit the education, health and social welfare of Israel’s citizens. Retrieved from

<https://twitter.com/IsraeliPM/status/965593667045031936>.

[33] Classified report: It is better to export natural gas through Egypt instead of Turkey, Yedioth Ahronoth, August 14, 2018.

[34] Energy: a shaping factor for regional stability in the Eastern Mediterranean?, Policy Department, Directorate-General for External Policies, European Union, June 2017

[35] Egypt to appeal $1.76 billion award to Israel in gas dispute, freeze gas import talks, Reuters, December 6, 2015.

[36] Why Israel’s gas deal with Egypt really blew up, Foreign Policy, April 23, 2012.

[37] Delek, Noble in talks to supply gas to Egypt, Globes, November 27, 2014.

[38] Egyptian court says no to gas exports to Israel, Reuters, December 1, 2008.

[39] النص الكامل لقانون تنظيم أنشطة سوق الغاز بعد تصديق رئيس الجمهورية عليه، اليوم السابع، 7 اغسطس 2017.

[40] الجريدة الرسمية تنشر بنود اللائحة التنفيذية لقانون الغاز، الدستور، 14 فبراير 2018.

[41] Israel-Egypt $15 Billion Gas Deal Boosts Energy Hub Prospects, Bloomberg, February 19, 2018.

[42] حسام بهجت، من يشتري غاز إسرائيل؟ شركة مملوكة للمخابرات المصرية، مدى مصر، 21 أكتوبر 2018.

[43] إسرائيل تعلن عن توقيع صفقة “تاريخية” لتصدير الغاز إلى مصر، بي بي سي، 19 فبراير 2018.

[44] وزير الطاقة الإسرائيلي يقول صفقة الغاز ستقوي العلاقات مع مصر، رويترز، 19 فبراير 2018.

[45] Egypt and Israel sign 15-year natural gas deal, The New York Times, July 1, 2005.

[46] Blast hits Egypt gas pipeline, Aljazeera, July 22, 2012.

[47] Egypt cancels Israeli gas contract, The Guardian, April 23, 201

[48] Egypt to Receive First Israeli Gas as Early as March, Bloomberg, October 8, 2018.

[49] مصر تعلن وقف استيراد الغاز المسال من الخارج، رويترز، 29 سبتمبر 2018.

[50]وزير البترول: سنتوقف عن استيراد الغاز فى أكتوبر وسنصدر فى يناير 2019، الوطن، 15 اغسطس 2018.

[51] Mostefa Ouki, Egypt – a return to a balanced gas market?, Oxford Institute for Energy Studies, June 2018.

[52] حسام بهجت، من يشتري غاز إسرائيل؟ شركة مملوكة للمخابرات المصرية، مدى مصر، 21 أكتوبر 2018.

[53] Egypt’s Gas Consumption to Reach 9 bcf/d in 2020/21, Egypt Oil & Gas, September 24, 2018.

[54] Egypt’s gas sector experiencing a renaissance, Capital Economics, 6 February, 2018

[55] Increase in gas production raises Egypt’s GDP 2.8%: Capital Economics, Egypt today, February. 6, 2018.

[56] Egypt has good reasons to buy Israeli gas, Globes, 5 November, 2018.

[57] Country Analysis Brief: Egypt, EIA Beta, May 24, 2018

[58] Country Analysis Brief: Egypt, EIA Beta, May 24, 2018.

[59] Tables Turned: Saudi Arabia Hunts for Oil Assets in the U.S., The Wall Street Journal, December 20, 2017.

[60] Egypt cancels Israeli gas contract, The Guardian, April 23, 2012.

[61] Jordan Pipeline for Israeli Gas Set for Completion by End of 2019, Bloomberg, July 4, 2018.

[62] Israeli Gas Exports to Egypt Could Flow Through pan-Arab Pipeline, Haaretz, November 20, 2018.

[63] Simon Henderson, Israel’s Gas Disappointment, The Washington Institute for Near East Policy, December 21, 2017.

[64] The East Mediterranean Geopolitical Puzzle and the Risks to Regional Energy Security, IENE’s SOUTH-EAST EUROPE ENERGY BRIEF- Monthly Analysis, Issue No 103 • July-August 2013.

[65] Elena Mazneva and Anna Shiryaevskaya, Why World Worries About Russia’s Natural Gas Pipeline, Bloomberg Businessweek, August 27, 2018.

[66] Janiki Cingoli, The New Energy Resources in the Centre-East Mediterranean: Potential Current and Future Geo-Strategic Consequences, Istituto Affari Internazionali, November 23, 2016.

[67] Andrew Ward, Geopolitical rivalries cloud prospects for Mediterranean gas finds, Finicial Times, January 8, 2018.

[68] Ioannis N. Grigoriadis, Energy Discoveries in the Eastern Mediterranean: Conflict or Cooperation?, Middle East policy council, Volume XXI Fall 2014 Number 3

[69] Keith Johnson, Curb Your Enthusiasm, Foreign Policy, February 21, 2018.

[70] Tareq Baconi, A flammable peace: Why gas deals won’t end conflict in the Middle East, European Council on Foreign Relations, December 21, 2017.

[71] Cyprus, Egypt sign gas pipeline agreement (Updated), Cyprus Mail, September 19, 2018.

[72] 2nd Licensing Round, Ministry of Energy, Commerce, Industry and Tourism, Hydrocarbon Service, February 11, 2012.

[73] Standoff in high seas as Cyprus says Turkey blocks gas drill ship, Reuters, February 11, 2018.

[74] Drillship Fatih kicks off operations in Med, second vessel to enter fleet soon, Dailly Sabah, October 30, 2018.

[75] The Eastern Mediterranean’s New Great Game Over Natural Gas, Stratfor, February 22, 2018.

[76] قرار جمهورى بالموافقة على اتفاقية تنمية الخزانات الحاملة للهيدروكربون، اليوم السابع، 10 سبتمبر 2014.

[77] مصر تعتمد ترسيمًا “محتملا” للحدود البحرية مع اليونان، وكالة الاناضول، 31 يناير 2018.

[78] Gas Discoveries in the Eastern Mediterranean: Implications for Regional Maritime Security, The German Marshall Fund of the United States, March 5, 2015.

[79] Oded Eran, Could natural gas in the Mediterranean spark the third Lebanese war?, The Jerusalem Post, February 18, 2018.

[80] Keith Johnson, Curb Your Enthusiasm, Foreign Policy, February 21, 2018.

[81] قرار ترسيم حدود فلسطين البحرية: جدل بين المسؤولين والخبراء، العربي الجديد، 6 يوليو 2017.

[82] Simon Henderson, Natural Gas in the Palestinian Authority: The Potential of the Gaza Marine Offshore Field, The Washington Institute for Near East Policy, March 2014.

[83] Greece, Cyprus, Italy, Israel sign MoU for East Med gas pipeline, New Europe, December 5, 2017.

[84] The East Mediterranean Geopolitical Puzzle and the Risks to Regional Energy Security, IENE’s SOUTH-EAST EUROPE ENERGY BRIEF- Monthly Analysis, Issue No 103 • July-August 2013.

[85] srael Closes Gas Pipeline Deal with Greece, Cyprus, Italy, OpenPaper, November 25, 2018.

[86] Agreement reached on Israel-Europe gas pipeline, Globes, November 25, 2018.

[87] Israel, Cyprus, Greece and Italy agree on $7b. East Med gas pipeline to Europe, The times of Israel, November 24, 2018.

[88] Israel reportedly closes $8B gas pipeline deal with Greece, Cyprus and Italy, i24NEWS, November 25, 2018.

[89] Israeli Cabinet Votes Yea on Natural Gas Export, Haaretz, June 23, 2013.

[90] Oded Eran, Elai Rettig, Ofir Winter, The Gas Deal with Egypt: Israel Deepens its Anchor in the Eastern Mediterranean, INSS Insight No. 1033, March 12, 2018.

[91] Israel looks to new Arab allies to export gas in volatile region, Finicial Times, November 13, 2018.

[92] Andrew Ward, Geopolitical rivalries cloud prospects for Mediterranean gas finds, Finicial Times, January 8, 2018.

[93] Egypt Resolving Dispute Holding Up $15 Billion Israel Gas Deal, Bloomberg, February 22, 2018.

[94] Egypt Signals That $15 Billion Gas Deal Will Hinge on Israeli Debt Concessions, Haaretz, February 26, 2018.

[95] “البترول”: بدء إجراءات تنازل إسرائيل عن قضايا تصدير الغاز، البورصة، 30 سبتمبر 2018.

[96] وزير البترول: سنتوقف عن استيراد الغاز فى أكتوبر وسنصدر فى يناير 2019، الوطن، 15 اغسطس 2018.

[97] Tareq Baconi, A flammable peace: Why gas deals won’t end conflict in the Middle East, European Council on Foreign Relations, December 21, 2017.

[98] Mostefa Ouki, Egypt – a return to a balanced gas market?, Oxford Institute for Energy Studies, June 2018.