On 6 April 2019, the International Monetary Fund (IMF) issued its fourth review of the Egyptian economy under the extended arrangement regarding Egypt’s $12 billion loan agreement with the Fund. The IMF stated some expectations for the performance of the Egyptian economy in the coming years and announced a timetable for lifting subsidies on petroleum products as pledged by the Egyptian government. Most interestingly, the IMF report said that it had conducted a stress test for the Egyptian debt endurance and found that it is sustainable but subject to considerable risk.

This paper attempts to define the stress test, emphasizing its significance, and discuss the structure of the Egyptian debt in light of the latest monthly statistical bulletin issued by the Central Bank of Egypt in February 2019. The results of the stress test will also be reviewed in order to reach recommendations on how to address the Egyptian debt file:

Stress Tests

A stress test, in financial terminology, is an analysis or simulation designed to determine the ability of a given financial instrument or financial institution to deal with an economic crisis. We can say that it is a new technique that includes a set of scenarios aimed at identifying the ability of different institutions to face any unexpected extraordinary risks, assuming a certain crisis and then predicting the likely performance of the institution in managing it. It is worth mentioning that these tests are applied to countries, banks and financial institutions alike.

Following are the main purposes of stress tests:

1- To provide the data needed for assessing the risks of potential exposures in critical situations, and thus enable financial institutions to hedge well for such circumstances.

2- To enable boards of directors and top administration to determine whether exposure risks are in line with their expected risk assessment.

3- To strengthen statistical measures of risk used by banks in different business models.

4- To assess the ability of banks to withstand difficult situations.

One of the most prominent central banks that conduct this test is the US Federal Reserve System – the central banking system of the United States. At the level of countries, the International Monetary Fund conducts stress tests in cooperation with the World Bank in order to assess the performance of the economies of these countries and determine whether their debts may fall under risks or not.

The test mainly simulates different shocks within predetermined parameters and measures reactions. This process is done uniformly to ensure comparing different economies together. For a better understanding of the effect of these shocks, the effect of each shock should be determined separately.

In terms of test results, the debt can be described as sustainable when the initial balance – the financial balance after deducting interest payments – is capable of stabilizing the debt under basic and realistic shock scenarios, taking into account the economic and political potential. This coincides with the debt level being consistent with low and acceptable risk volume on financing, while maintaining potential growth at a satisfactory level. Conversely, the economy is seen as unsustainable if the initial balance cannot stabilize the debt.

Structure of Egyptian debt:

To examine the size, nature and structure of the Egyptian debt, we will rely on the latest monthly statistical bulletin published by the Central Bank of Egypt, the February 2019 bulletin:

1- The external debt:

The total external debt reached US$ 93.1 billion at the end of the first quarter of the current fiscal year 2018/2019. Debt service charges during the first quarter totaled US$ 2.2 billion, including US$ 1.4 billion of repaid instalments, while interest constituted US$ 868 million.

Comparing the external debt with the various macroeconomic indicators shows further significant indications: For example, the ratio of external debt to GDP was 35.4% while the average foreign debt per capita was $ 874. Due to the maturity period, 87.7% of the total external debt is long term, while 12.3% is short-term.

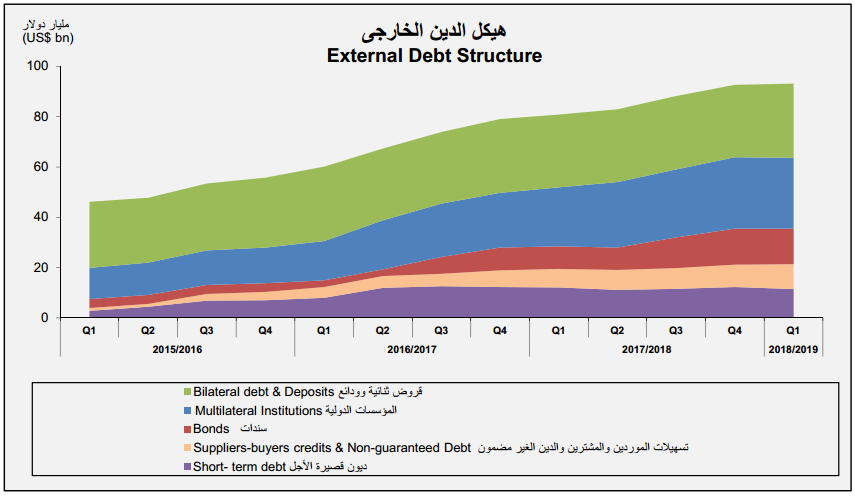

Figure 1: External debt structure from the first quarter of the fiscal year 2015/2016 to the first quarter of the fiscal year 2018/2019.

Source: Central Bank of Egypt, Monthly Statistical Bulletin, No. 263 – February 2019, p: 101

Figure 1 shows the development of the external debt structure from the first quarter of the fiscal year 2015/2016 to the first quarter of the fiscal year 2018/2019. It shows the steady increase of the external debt over the past three years.

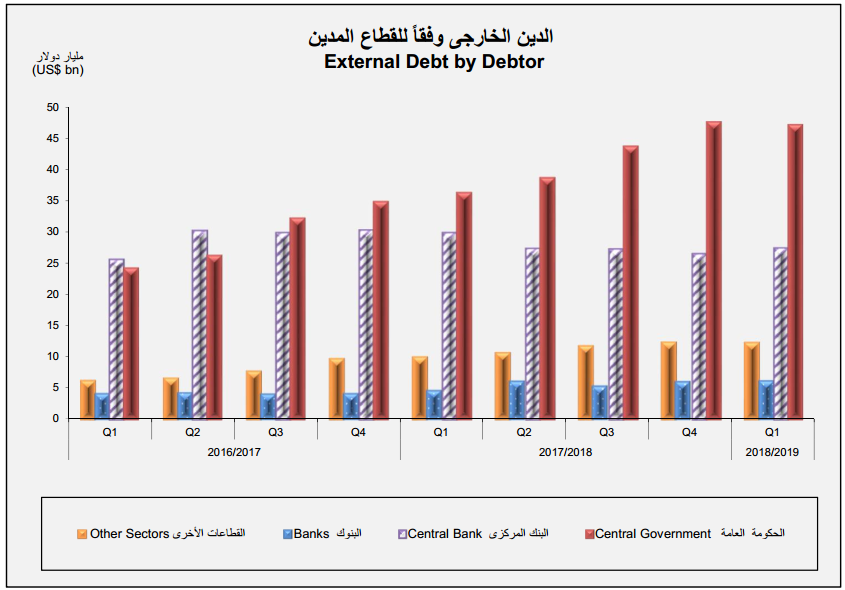

Figure 2 shows external debt according to the debtor sector.

Figure 2: External debt according to the debtor sector from the first quarter of the fiscal year 2016/2017 to the first quarter of the fiscal year 2018/2019.

Source: Central Bank of Egypt, Monthly Statistical Bulletin, No. 263 – February 2019, p: 101

Figure 2 shows an increase in the share of government debt in the total external debt over the past two years.

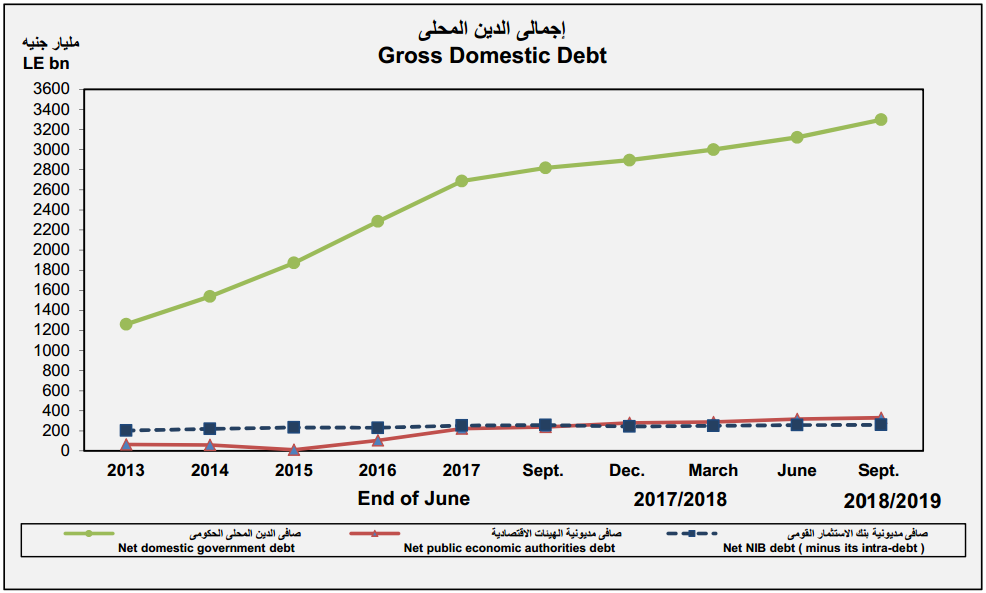

2. The domestic debt:

The total domestic debt stood at 3.89 trillion pounds at the end of the first quarter of the current fiscal year 2018/2019, by 74% of GDP, including 84.8% as government debt, representing about 3.3 trillion pounds.

The ratio of domestic government debt to GDP for the same period reached 62.8%, while the rate of indebtedness of public economic entities to GDP reached 6.3%.

Figure 3 shows the development of the total domestic debt since 2013

Figure 3: Development of total domestic debt since 2013

Source: Central Bank of Egypt, Monthly Statistical Bulletin, No. 263 – February 2019, p.

3- Total external and domestic debt as a percentage of GDP:

According to the above data, the total external and domestic debt is 5.4 trillion pounds, while the gross domestic product is 5.3 trillion pounds; which means that the total debt exceeded 100% of the GDP, which is a harbinger of danger to the Egyptian economy if the same policies continue to expand access to loans .

Results of the stress test on the Egyptian debt

Below, we will discuss the results of the stress test conducted by IMF experts, released by the IMF in its fourth review of the Egyptian economy.

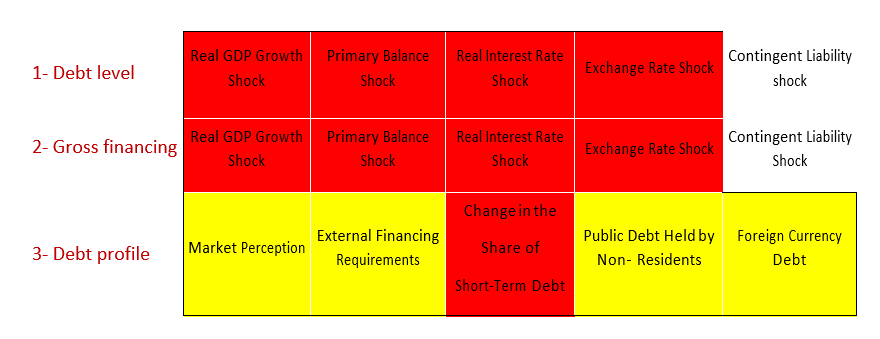

a- The heat map of the Egyptian economy:

Figure 4 shows the temperature map of the Egyptian economy, which highlights the impact of different shocks on both the debt rate and the net financing needs as well as the debt portfolio:

Figure 4: Heat map for the analysis of the sustainability of the Egyptian debt

Source: International Monetary Fund, Arab Republic of Egypt: Fourth Review Under the Extended Arrangement, p: 40

In view of the above, we can state the following:

– The Egyptian debt is extremely vulnerable to significant risks if it is exposed to any of the five shocks (excluding the contingent liability shock as the Egyptian economy is not in a position to do so), as well as the shock of external financing requirements, where the Egyptian debt is vulnerable to significant risks.

– On the contrary, the debt portfolio capacity is moderate in withstanding the five shocks except for the change in the share of short-term debt.

– The IMF concluded from this test that the Egyptian debt is subject to significant risks with emphasis that it is currently sustainable, indicating that the policy of debt expansion currently adopted by the government should change.

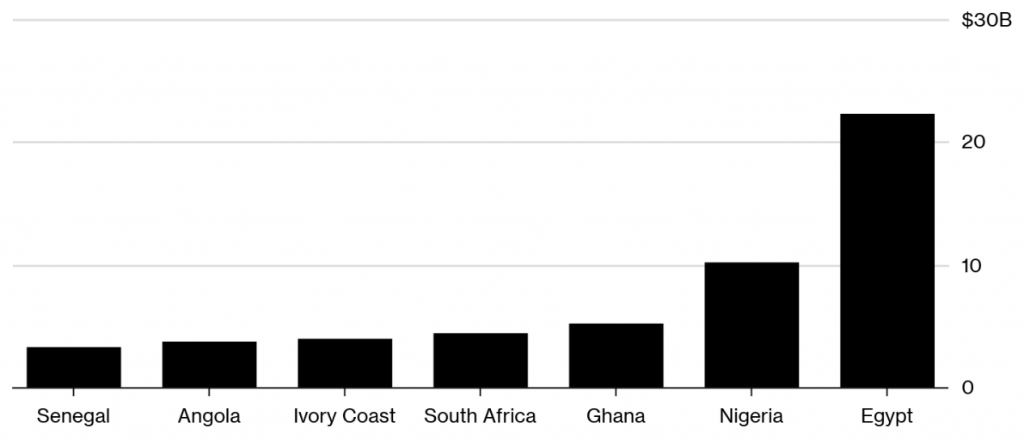

It is important that the government should announce a change in this policy. According to a recent Bloomberg report, “Egypt has been by far Africa’s most prolific issuer of Eurobonds since the start of 2017, selling more than $22 billion of securities.” Egypt’s borrowing during that period is more than the combined borrowing of Nigeria and South Africa, the continent’s biggest economies.

The following figure shows a comparison between Eurobonds issued by Egypt and 6 different African countries during the period from January 2017 – April 2019.

Source: Paul Wallace and Lyubov Pronina, A $ 22 Billion Bond Spree Sees Egypt Dominate Africa Peers: Chart, Bloomberg, 8 April 2019

This reinforces the importance of changing the current government policy of debt expansion because the fact that the debt is vulnerable to significant risks may raise the debt cost in the future, which will put more pressure on the state budget.

Another global challenge, the report said, is that the current global trend of pulling-back by investors from emerging markets could hurt Egypt, as it would raise the cost of borrowing.

b- The IMF scenarios and expectations on the Egyptian debt:

The following points review scenarios developed by the IMF and their expected impacts:

1- The public debt trajectory is vulnerable to macroeconomic shocks and risks from contingent liabilities: as under a growth shock where GDP growth is 1.2 percentage points lower (one standard deviation) and inflation is 0.3 percentage point lower compared to the baseline in 2018/19 and 2019/20, debt would decline to 72 percent of GDP over the medium term compared to 69 percent in the baseline.

2- A real interest rate shock with an increase of the interest rate by about 350 basis points over the projection period, increases debt by around 3 percentage point of GDP to 72 percent of GDP over the medium term compared to the baseline.

3- A large real exchange rate shock with a hundred percent depreciation of the Egyptian pound will increase debt in the next year by 6 percentage point of GDP compared to the baseline, and by 3 percentage point of GDP over the medium term.

4- A combined macro-fiscal shock with lower growth and a looser fiscal stance could weaken favorable debt dynamics. A temporary growth shortfall of 1.2 percentage points for two years, a looser fiscal stance by about 1 percentage points over two years, and about 140 percent of nominal exchange rate depreciation increases debt to 90 percent of GDP in the following year compared to 82 percent of GDP under the baseline. Over the medium-term, debt would remain about 10 percentage point of GDP higher than under the baseline.

5- Materializing of contingent liabilities or a call on government guarantees from state-owned enterprises are another potential source of vulnerability. A customized shock scenario, in which a contingent liability of 10 percent of GDP materializes, leading to a deterioration of the primary balance, higher interest rates and temporary adverse impacts on other macro-economic variables, would increase debt-to-GDP ratio to 93 percent of GDP in 2019/20 compared to 82 percent in the baseline.

6- The most severe shock combines the macro-fiscal shock with a materialization of a contingent liability. In this case, debt-to-GDP ratio will increase in the next year to 100 percent of GDP. Over the medium-term debt would decline to around 88 percent of GDP and gross financing needs would be about 50 percent of GDP.

Recommendations on how to manage the Egyptian debt crisis:

In order to avoid Egypt’s inability to repay its debts in the future and to reduce the risks to them; the paper can make

Following are some recommendations and suggestions on how to manage the Egyptian debt crisis to avoid Egypt’s inability to repay its debts in the future:

1- To develop a clearly defined plan for dealing with the domestic public debt, which has expanded significantly in recent years, taking into account the following points:

- Setting a ceiling on domestic public debt as a percentage of the GDP.

- Finding ways to finance the government expenditure other than the high-yield bonds to ease burdens on the state budget.

- Conducting a thorough and comprehensive review of the public treasury bills, ensuring that it is reconsidered as a method of financing the budget deficit.

2- Increasing the Egyptian tax base, not by imposing new taxes, but by applying existing laws. In this context, the state needs to shift from tax collection to development.

3- Reviewing the debts of governmental bodies and companies periodically, so that the State to avoid falling under international arbitration and bearing the debts of any of these bodies.

4- To verify the feasibility of supporting economic bodies. Under Law No. 11 of 1979 that amended some provisions of Law No. 53 of 1973, the uses and resources of public economic bodies and private funds were separated from the uses and resources of the entities involved in the general budget of the state, and limiting relation between them on the surplus that goes to the budget. In fact, the main purpose of the law is to allow these bodies start their activities on their own and not to burden the state treasury with any expenses, leaving the door open for the state to provide them with grants and contributions.

The fact is that some of these bodies continue to rely on funding their expenditures through grants and contributions. According to government data, the public economic bodies received about LE 217044.5 million pounds in the fiscal year 2016/2017. This figure increased in the following year to reach LE 264584.3 million. It is noteworthy that the General Authority of Petroleum and the General Authority for Supply Commodities and the National Authority for Social Insurance accounted for 98.4% of the total grants and contributions.

5- Reviewing the budgets of special funds annually, as well as coordinating with the House of Representatives to issue a unified regulation for managing these funds, which will prevent any manipulation or waste of the public funds.

6- Modifying the Egyptian economy structure and focusing on manufacturing industries, activating the work of small and medium enterprises, reducing imports and increasing exports, thus alleviating the chronic deficit in the state budget, trade balance and balance of payments.

7- Activation of Article 4 of Law No. 53 of 1973, which provides for conducting an analysis of the enterprises funded by the Public Treasury so that the government can maintain the funding of profitable and economically feasible enterprises and abandon the losing projects that constitute a burden on the State.

To Read Text in PDF Format Click here.